Capital Formation, Fundraising, and M&A to Accelerate the Energy Transition

In October, Jefferies and SMBC co-hosted a forum for senior executives from leading Japanese corporations and investment firms. The event, titled “How to Commercialize the Japanese Energy Transition,” examined how companies can monetize opportunities tied to the global transition and Japan’s Green Transformation (GX) Plan, a $1 trillion initiative to reduce emissions over the next decade.

During one panel, “Capital Formation, Fundraising, and M&A to Accelerate the Energy Transition,” senior leaders from KKR, TPG, Jefferies, and Twelve Inc. discussed a major shift underway in global energy-transition finance. The group focused on what is pushing the transition forward — and what is slowing it down — as unprecedented electricity demand from hyperscaler data centers and rapid AI adoption begins to reset everyone’s priorities.

The panel featured Tracy Wolstencroft, Senior Adviser with TPG Rise Climate; Emmanuel Lagarrigue, Global Co-Head of Climate for KKR; Twelve Inc. Chief Financial Officer Jimmy Chuang; and Jefferies Managing Director Jeff Tang.

Hyperscales Drive A New Wave of Energy-Infrastructure Buildout

Mr. Wolstencroft stressed that the U.S. transition story is gaining strength. Citing earlier speakers, he described a shift “from energy transition to energy addition and from clean transition ambition to practicality.”

AI’s rapid growth is forcing companies such as Google and Microsoft to secure long-term, cost-stable power supplies. That push is accelerating solar development and large-scale data-center construction.

“Hyperscalers need electrons, and they need them right now,” Mr. Wolstencroft said.

Scaling Companies — Not Capital — Is the Problem

When the conversation turned to the market’s “missing middle” challenge, Jefferies’ Mr. Tang reframed the issue.

“Many people think of the missing middle as a lack of capital for a certain type of company. And I would like to challenge that and say that it’s not, in my view, so much like capital,” he said. “It’s a lack of companies that are able to reach escape velocity and reach the type of performance that can access this type of capital.”

Capital is available, he argued, but companies need more time to develop into organizations that can use it effectively. “I don’t really think of it as missing capital, it’s more missing progress,” Mr. Tang explained.

Twelve Inc. Shows What Scale-Ready CLimate Hardware Looks Like

Panelists pointed to Twelve Inc. as a strong example of a company built for scale. “Tweleve is a great example of what is required to get these capital-heavy businesses to scale . . . the path toward competitive unit economics is front and center,” Mr. Wolstencroft said.

Twelve Inc.’s Mr. Chuang noted that Twelve is essentially sold out through 2030, adding, “we’re at a point where we can deploy our product to the world at a commercial scale.”

“This year we can start flying regularly with airlines . . . and they’ll be the world’s first CO2-to-fuel powered commercial flight,” he said. The company illustrates the level of investment required to bring next-generation decarbonization technologies to market.

Corporate Partnerships and Demand Unlock Financing

Referencing Twelve Inc.’s model, investors emphasized how corporate demand enables companies to secure low-cost project financing. Discussing airline interest, Mr. Lagarrigue noted: “British Airways, Microsoft, Alaska Airlines [are] providing that signal that enables the company to have access to very low cost of capital.”

Panelists also stressed the role financial institutions play in connecting corporate buyers with emerging suppliers. “Your ability to put both sides of the problem into a room… demand and supply … is critical to scaling these industries,” Mr. Wolstencroft said.

The panel agreed that coordinated action among corporate buyers, developers, and financiers is central to advancing the transition.

Follow along for more insights from Jefferies’ Sustainability and Transition Team on the Japan GX Plan and other important climate investing themes in the weeks ahead.

How Can Companies Commercialize the Japanese Energy Transition?

Last week, SMBC and Jefferies co-hosted a forum for senior executives from leading Japanese corporations and investment firms. The event built on Jefferies’ Sustainability and Transition team’s longstanding collaboration with Japanese leaders to unlock opportunities in the country’s climate investing and decarbonization journey.

SMBC and Jefferies explored how Japanese companies can best monetize the energy transition and Green Transformation (GX) Plan, a $1 trillion effort to reduce emissions over the next decade. The event’s themes — pragmatism, value creation, and collaboration — anchored discussion of best practices across Europe, the United States, and China.

Below are key takeaways from the event, each paired with guidance for companies.

- The View from Asset Allocators

Key Takeaway: Asset owners are now integrating the transition across strategies, not limiting it to dedicated products.

Advice for companies:

- Clearly communicate the link between your transition plans and national policy frameworks.

- Treat regulatory and investor collaboration as part of your strategy.

- Align transition goals with your core competencies.

- Focus your investments on specific segments of the transition.

- Lessons from Portfolio Managers

Key Takeaway: Investors only support transition initiatives that expand enterprise value by strengthening moats, driving growth, improving profitability, or creating strategic optionality.

Advice for companies:

- Lead with value creation, not disclosures.

- Invest in regions that have low levels of policy uncertainty.

- Navigating Governance & Investor Activism

Key Takeaway: Governance is foundational. Credible boards, long-term planning, and active debate are key to success.

Advice for companies:

- Add directors with technical and sector expertise.

- Tie incentives to long-term strategic goals for the transition.

- Engage foreign investors early with a clear, credible narrative.

- Narrow priorities to areas of focus and strength.

- Ensure robust internal debate before setting transition strategy.

- US, European & Chinese Companies

Key Takeaway: Innovation that drives energy cost deflation is the unlock. Energy security and transition goals need to be managed together.

Advice for companies:

- Balance decarbonization with competitiveness and energy security.

- Prioritize innovation and drive down costs of new technologies.

- Compete where you have structural advantages (e.g., nuclear).

- Insights from Japanese Companies

Key Takeaway: Domestic and international collaboration is essential for scaling transition technologies.

Advice for companies:

- Pursue joint ventures and side-car structures.

- Avoid hype cycles; maintain long-term orientation.

- Tailor strategies for Asian markets and demand patterns.

- Capital Formation, Fundraising and M&A

Key Takeaway: Capital markets for the transition remain active, supported by load growth and energy security priorities.

Advice for companies:

- The missing middle is not capital, but clarity on risk allocation and de-risking.

- Build solutions that reduce execution risk and improve unit economics.

- Engage capital partners early and structure for scale and bankability.

Japan’s GX spans all areas of climate finance: carbon levies, emissions trading, transition bonds, and more. And given that it represents nearly three times the annual GDP investment percentage of the U.S. Inflation Reduction Act (relative to the sizes of their economies), it is sure to be one of the defining climate investment themes of the next decade.

For Japanese and global companies alike, that scale of opportunity comes with meaningful strategic considerations. The insights from Japanese executives and climate investors here offer a practical guide for navigating this moment in the global transition.

Follow along for more insights from Jefferies’ Sustainability and Transition Team on the Japan GX Plan and other important climate investing themes in the weeks ahead.

Paul Singer on Exercising Caution in an Era of Extremes

Views on the trajectory of equity markets vary widely, but most agree that today’s conditions are truly unprecedented.

Artificial intelligence is driving record levels of investment and capital expenditure, tariff policies are reshaping global trade, and a prolonged era of near-zero rates — followed by the sharpest inflation surge in decades — has left investors divided on the future course of monetary policy.

Few are better positioned to weigh in than Paul Singer, Founder and co-CEO of Elliott Management, recognized as one of the world’s most prominent hedge fund managers for decades. Drawing on that experience, Singer shared his views on today’s conditions and how investors might navigate them with the Jefferies team at TechTrek, the firm’s annual tech investor conference in Tel Aviv.

The following remarks have been edited lightly for clarity.

How High Valuations and Political Intervention are Shaping Equity Markets

Singer, who launched his first investment firm in 1977, views markets through decades of experience. Having lived through several major bear and bull markets, even he says today’s conditions are extraordinary.

“Right now, the near-term risks are unusual. Valuations may or may not trigger a melt-up or a meltdown, but history tells us today’s valuations point to low forward returns,” he explained. Singer noted that U.S. equity valuations — especially in the tech sector — are among the most drastic on record.1

Singer cautioned that many investors believe President Trump will do whatever it takes to prevent a bear market, pointing to the post-Liberation Day tariff rollback as an example. “That belief allows valuations to stretch to even greater extremes,” he said.2

This push and pull — between the president’s efforts to support markets and investors’ belief that such support makes them indestructible — creates a uniquely difficult market to predict.

Singer Urges Caution Amid Ongoing Uncertainty

Looking ahead, Singer pointed to three themes he sees shaping global equity markets: artificial intelligence, inflation, and tariffs.

“It’s true that artificial intelligence is an immediate and powerful transforming force. But in some businesses, there are still kinks to be ironed out,” Singer said. Investors are in an “I believe” mode when it comes to the technology, and he argues that a healthy dose of skepticism is warranted.

On inflation, Singer warned it may be too soon to assume the worst is over. “Another burst of inflation is a significant possibility,” he said. “The 2021 surge was comparable to the bursts — plural — of the 1970s. Back then, we learned that inflation is rarely one and done.”

Finally, on tariffs, Singer noted that current policies are likely to raise prices and squeeze margins, even if they address trade imbalances. “The president believes these imbalances are important to correct,” he said. Reflecting concerns with a range of political uncertainties and economic risks, Singer warned, “I do think conditions for a possible bear market are now in place.”

“Our debt, fiscal policy, and monetary policy are unusual, so my firm is operating with the highest degree of prudence,” Singer said. “I think investors of my generation — those who’ve lived through multiple bear markets — know to be cautious right now.”

Singer has built his career challenging prevailing market sentiment. His message today is that no condition is permanently sustainable — whether it’s the rise of AI, stretched equity valuations, or the current mix of monetary and trade policies. For investors, he argues, caution is a wiser path than overconfidence.

For more from TechTrek — including interviews with top founders, executives, and investors like Paul Singer — visit Jefferies Insights.

Lessons from Portfolio Managers: A Guide for Japanese Corporates to Attract Public Equity Capital

In October, Jefferies and SMBC co-hosted a forum for senior executives from leading Japanese corporations and investment firms. The event, titled “How to Commercialize the Japanese Energy Transition,” examined how companies can monetize opportunities tied to the global transition and Japan’s Green Transformation (GX) Plan, a $1 trillion initiative to reduce emissions over the next decade.

One session, “Lessons from Portfolio Managers: A Guide for Japanese Corporates to Attract Public Equity Capital,” gathered four public-markets investors: Thomas Kamei, Executive Director at Morgan Stanley’s Counterpoint Global, leading the Tailwinds Fund; Rolando Morillo, Portfolio Manager for Rockefeller Asset Management’s Thematic Equity Offerings; Will Pomroy, Director of Impact Engagement & Sustainability at Federated Hermes; and Masanori Mizuno, Principal, Responsible Investment Section, Sumitomo Mitsui DS Asset Management.

The key question: how do international equity managers evaluate and allocate to transition strategies globally.

The Allocation Lens: Value First, Not Labels

Mr. Kamei opened with a clear framework for how his team evaluates transition strategy. Any initiative, he said, has to connect to one of four enterprise value drivers: extending a company’s durable competitive advantage, driving growth, improving profitability, or creating thematic optionality for the future. If it doesn’t, “we don’t think it has business value.”

The goal isn’t simply to “own fewer bad companies,” but to identify where a transition strategy directly contributes to alpha.

Rockefeller’s Approach: Mitigation, Adaptation, Security

Mr. Morillo framed climate change as a present, not distant, force shaping markets. Rockefeller’s approach starts with identifying durable business models with this is mind, linked to either climate adaptation or mitigation — and recognizing that the two increasingly overlap.

“It’s not just about decarbonization,” he explained. “It’s also about energy security. It’s about food security.” As global temperatures rise beyond the 1.5°C threshold, he sees a growing, often overlooked opportunity in adaptation: companies enabling greater resilience across supply chains, infrastructure, and agriculture.

Rockefeller focuses on companies with resilient balance sheets and strong management teams. These businesses, Mr. Morillo said, are positioned to navigate policy change, scale new technologies, and capture demand as the transition accelerates.

Engagement as a Core Mechanism

At Federated Hermes, Mr. Pomroy described engagement as the core of the investment process. “Engagement is central, foundational to how we go about pursuing investments for our clients,” he said. The firm’s active, long-term funds focus on governance quality and a company’s openness to dialogue. He called this “receptiveness to engagement.”

That responsiveness is often the best signal of readiness for transition, which he described as “a journey” requiring patient, purposeful conversation between investors and management.

Momentum Over Static Scores

Mr. Mizuno drew a distinction between ESG, impact, and transition investing, emphasizing rate of change over static ratings. “We pay more attention to the changes, the momentum,” he said, “not the raw level of ESG score.”

Beyond screening, his team seeks to “proactively contribute to the positive change of the corporate… through engagement,” including through initiatives like Japan Hydrogen that aim to make a “hydrogen society” bankable with true “risk money.”

Why Japan (Now)

Across the panel, Japan’s appeal is rising. Mr. Kamei pointed to world-leading industrial niches — “60% market share of global precision gears used in industrial robots” — and the importance of retruns that clearly links strategy to secular growth.

Mr. Morillo cited visible shifts in governance and capital allocation discipline, plus attractive valuations. Mr. Pomroy noted that eight years of governance and capital-efficiency reforms have made conversations “much richer,” with a stronger “convergence in interest” between societal needs and investor returns.

Where the Opportunities Are

Mr. Morillo highlighted three near-term buckets: low-carbon power (including nuclear restarts toward a “20 to 22%” mix target), grid “infrastructure” and “resilience,” and an impending wave of energy-efficiency retrofits across aging building stock. He also called out industrial decarbonization (electrification and advanced materials). One example: carbon fiber in aerospace delivering “about 20% fuel efficiency,” a real cost and emissions win.

Mr. Kamei underscored grid build-out as an investable pull (citing Quanta Services’ multiple expansion tied to “incremental free cash flow” from grid spend), and offered a caution on box-ticking: “… [a] focus on disclosure has been counterproductive,” especially when metrics can be gamed without real-world abatement.

What Corporates Should Do Now

The panel closed with practical guidance for companies seeking to attract capital.

Mr. Pomroy urged firms to translate transition targets into clear financial terms, connecting plans directly to the top line, bottom line, and capex context. Mr. Mizuno stressed the importance of showing outcomes rather than slogans, calling for “commitment to action” and tangible metrics that demonstrate progress.

Mr. Morillo highlighted a more immediate constraint: execution capacity. “We may not have the labor resources necessary,” he said, urging companies to plan for skilled-labor gaps as they scale new projects. And Mr. Kamei returned to the investor lens: “We need to change the mindset,” he said. “It is not about owning fewer bad companies; it’s about alpha.”

Follow along for more insights from Jefferies’ Sustainability and Transition Team on the Japan GX Plan and other important climate investing themes in the weeks ahead.

Energy Transition Allocation – The View from Asset Allocators

In October, Jefferies and SMBC co-hosted a forum for senior executives from leading Japanese corporations and investment firms. The event, titled “How to Commercialize the Japanese Energy Transition,” examined how companies can monetize opportunities tied to the global transition and Japan’s Green Transformation (GX) Plan, a $1 trillion initiative to reduce emissions over the next decade.

One session brought together global investment leaders to discuss how asset allocators (pensions, insurers, and sovereign wealth funds) are deploying capital into Japan’s transition. The panel featured Helga Birgden, Global Chair of Sustainable Investing at Mercer; Glenn Yelton, Global Head of Investment Stewardship & ESG at Invesco; and Debanik Basu, Head of Sustainable Investing (APAC) at APG.

Their prompt: explain how the ultimate owners of capital think about risk, return, and policy in the context of the transition.

Allocation Is Now Broad, Not Niche

The transition has moved from specialist strategies to market-wide allocation.

As Mr. Yelton of Invesco explained, clients now expect energy-transition exposure “across every strategy that we manage… fixed income, our equity strategies, our private market strategies,” and if managers are not doing that, “we are in fact not allocating alongside the market.”

He noted that almost half of Invesco’s ESG-characterized AUM is now climate-focused and growing, and that in 2024 the firm launched two climate-transition ETFs for a single U.S. client totaling “over $4 billion.”

What’s Working, What Isn’t

Ms. Birgden described where capital is flowing today: “core investments in renewables, efficiency… batteries and electrification.”

Ms. Birgden cited survey work showing transition readiness is a high priority for asset owners (Morningstar’s read of 500 owners across 11 countries) and that a majority of investors KPMG surveyed have already invested in energy-transition companies, with “a big drive towards electrification.”

Private Markets Lead, But Public Markets Still Matter

The panel agreed that most transition investment activity today is happening in private markets. Mr. Basu noted that private allocations offer clearer attribution — “we can select real assets rather than companies” — and give investors greater ability to shape strategy through ownership and engagement.

Public markets, however, remain essential

Ms. Birgden added that asset owners are also reshaping public exposures by “choosing transition-aligned benchmarks” and applying climate considerations across global equity and credit portfolios.

Policy as a Valuation Input

Policy support matters because it changes the economics of projects, but only if it’s durable.

Mr. Yelton called it “the off-balance-sheet component” that can make a marginal deal attractive “if you believe that the government is going to be committed… for an extended period of time.” He contrasted Japan’s policy cohesion with U.S. volatility, which forces “a discount factor on those supplemental components,” while noting state-level building codes and programs can still drive activity.

Mr. Basu underlined why policy fills a practical gap: many customers “are not willing yet to pay a green premium,” investors are “not willing to put in concessionary finance,” and key technologies in hard-to-abate sectors “do not yet exist or are not yet fully scalable.”

He offered two examples: a steelmaker with credible decarbonization roadmaps in Europe but uncertainty in India due to feedstock and technology constraints; and a Mexican cement company limited by U.S. building codes that restrict lower-clinker cement despite its lower carbon profile.

The Backlash and the Reset

The panel characterized recent pushback as a move toward pragmatism, not a retreat. Mr. Yelton said, “The biggest pushback we get is when performance goes down,” which is true of any strategy. He argued that early net-zero pledges moved from “ideation to implementation” too fast” Economics must track decarbonization for fiduciaries.

Ms. Birgden described a “pendulum swing”: fewer public green claims due to tighter rules on greenwashing, alongside continued, quieter work on decarbonization. She also noted investors working directly with governments, citing Australia, where institutional investors helped shape national targets.

Follow along for more insights from Jefferies’ Sustainability and Transition Team on the Japan GX Plan and other important climate investing themes in the weeks ahead.

Capital Markets and the Rise of AI

It is difficult to overstate the significance of the rise of artificial intelligence for capital markets. The massive scale of current AI investments and the rapid pace of technological progress raise questions and increase stakes for nearly all investors, companies, and countries as they try to anticipate what the future holds. According to Brent Thill, the Tech Sector Leader of Software and Internet Research at Jefferies, the story of AI is just beginning, although certain long-term trends are becoming apparent.

On November 11, Brent and his team host several hundred senior leaders at the Jefferies AI and Capital Market Summit. There, they will discuss the most significant trends shaping AI development and their implications for various industries and markets. Ahead of the event, we spoke with Brent to get his perspective on a few key questions likely on attendees’ minds.

Q: Some recent media coverage has suggested that a lot of major corporate AI investments have yet to turn a significant profit. What’s your take on this narrative?

Contrary to what you hear in some quarters, AI is making money today on multiple fronts. The backlog of contract signings is $700 billion across the tech vendors we watch in the hyperscale market. That’s over 200% greater than the Capex increase. So, revenue exceeds the investment. Over the last two years, Microsoft has shown that it has expanded operating margins while investing in AI. So, when you look at both revenue-to-costs and margin, we continue to believe there’s pricing power and that the economic output of AI will exceed its costs.

The long-term ROI case study for AI is yet to be seen. We don’t believe you’re seeing significant jobs reduced or eliminated at this point. AI is effectively augmenting rather than replacing today. Long-term, there will no doubt be job loss. The question is, what’s the magnitude of that loss?

What are the most notable trends you have seen unfold in the last six months to a year?

The number one trend is investment in infrastructure for AI. The other things, like applications, are not selling as robustly as energy, land, data centers, power, water cooling and all the other things that go into enabling AI to run. That’s what’s booming right now. The applications and the number of people inside using AI are yet to come, which helps explain why many application stocks have lagged materially.

Where is the lion’s share of the investments going?

For AI to work, you must have three things: users, data, and capital. You can count on two hands the number of companies that have those things: Microsoft, Amazon, Oracle, Google, Nvidia are the big ones of course. That is why we believe, as an investment thesis, that you want to stay long with the biggest companies that are leading investment in this space. The number one constraint is energy. So, energy is a big winner. Some energy stocks are up 50% to 500%. No one would have seen that coming five years ago. There will also be specialized vendors that benefit, such as CoreWeave and Nebius, which handle data center infrastructure, along with chip companies like Avago and Broadcom. However, for now, this remains a very narrow trade.

What are the risks and concerns we should have about the AI story today?

The risk is the ROI. We’re putting such a big investment into infrastructure. It’s the biggest investment we will see in our lives. The big question is, can AI do what everyone says it can do? And when are we going to see the adoption path inside the enterprise? Today, that process is early and the path to revenue is uncertain. Nonetheless, we expect substantial returns from AI investments, and we will see them in the near future. There are so many AI tools available to us, but many users aren’t trained. Enterprise still must go through the crawling and walking stages before this thing really takes off. Then, data governance and security are critical issues for AI. One of the biggest challenges we hear about is that the adoption of these technologies can’t succeed if you’re using poor data, because that leads to bad results. However, these are solvable problems. They also present great opportunities for companies that can provide effective data security solutions.

What are the major things you see happening with AI in the next two years?

What we will see in the next couple of years is an AI shakeout. We will go from the tryout phase to the implementation phase. I think many of the systems we are just seeing now will be used in a big way in 2026 and 2027.And that’s when we start to see bigger ROI. That’s when we see more capital allocated. Another thing you should keep in mind is that during past major technological shifts – such as the arrival of the internet or the shift from PCs to mobile devices – entire boards of directors did not rush to demand the adoption of these new technologies. Today, however, boards are frenetically pushing for the adoption of AI because of its potential future impact. There has really been nothing like this in the last 30 years.

Geopolitics, AI, and Israel: Bill Ackman on the Forces Shaping Global Markets

For investors, the key questions are how today’s instability may ripple through the world economy — and whether the opportunities are strong enough to outweigh the risks.

Today, geopolitics may be shaping global markets more than at any point in decades. Wars in Ukraine and the Middle East have fueled inflation, while shifting monetary and trade policies are reshaping economic activity across borders.[1][2]

Bill Ackman, Founder of Pershing Square Management, is uniquely well-positioned to weigh in. A widely recognized voice in investing and global affairs, he sat down with Jefferies to share his perspective on world markets, U.S. growth drivers, Israel, and more.

The following remarks have been edited lightly for clarity.

How Defense Spending Could Bolster the Global Economy

A seasoned international investor, Ackman brings a sharp view of the opportunities and risks shaping global markets. He told Jefferies that while conflict is a near-term risk, today’s investments in deterrence could position the global economy to thrive in the long run.

“The biggest concern today is geopolitical risk. But the actors who’ve launched wars — Russia in Ukraine, Hamas and Hezbollah in Israel — are not in a better place,” Ackman said. These outcomes, he suggested, may discourage others from provoking future conflicts.

“The best outcome of today’s geopolitical environment is the investment in deterrence and defense. I think we’ll see more of that globally,” he said.

Global defense spending reached a record in 2024 as countries responded to a deteriorating security environment. This spending may carry a two-fold benefit for the global economy: improving geopolitical stability over time while supporting infrastructure and R&D investment today.

The Intersection of the AI Boom & Pro-Business Policy Agenda

Beyond geopolitical risk, Ackman sees powerful growth engines in the US economy, which in turn drives global advancement. He points to two in particular: the AI boom and a pro-business policy environment.

“The biggest driver of global markets is the AI revolution,” he said. “I’ve never seen capex numbers like this. Trillions of dollars are pouring into our economy.”

On policy, Ackman highlighted several tailwinds: “We have the infrastructure bill, which is only starting to be spent. We have a new tax regime that’s creating economic incentives. And we have a deregulation agenda.”

The 2021 Infrastructure Investment and Jobs Act provides $1.2 trillion in spending, an effort widely expected to spur economic opportunity in the years ahead. As Ackman notes, this investment is rolling out alongside an ambitious deregulatory push from the current administration.

“These forces are going to lift confidence, and they make me bullish on America,” he said.

Why Ackman Eyes Enduring Value in the Tel Aviv Stock Exchange

The conversation closed on Israel, where Ackman has invested a nearly 5% stake in the Tel Aviv Stock Exchange (TASE). Owning an exchange, he explained, is a way to invest in the success of a country as a whole. His stake in the TASE reflects his broader confidence in Israel’s trajectory.

“An exchange is basically a royalty on a country’s success. It thrives as more companies list, market cap grows, and economic activity increases,” he said. “It’s the perfect way to make a long-term bet on a country.”

Ackman noted that the Israel of his parents’ generation is very different from the country today. What once was considered a destination for philanthropy, as opposed to strategic investment, has grown into one of the world’s strongest startup and venture capital ecosystems, with the highest number of unicorns per capita worldwide.

“When I invested in the exchange, the whole thing was valued at $500 million. It just felt like the wrong number,” he said. “My only regret is that I didn’t buy more.”

For more from TechTrek — including interviews with top founders, executives, and investors like Bill Ackman — visit Jefferies Insights.

[1] https://www.bcg.com/capabilities/international-business/navigating-international-trade/what-is-a-tariff?utm_source=search&utm_medium=cpc&utm_campaign=geopolitics&utm_description=paid&utm_topic=tariffs&utm_geo=global&utm_content=dsa_explainer&gclsrc=aw.ds&gad_source=1&gad_campaignid=22423918029&gbraid=0AAAAACKyBhqyT_pBJ4oJv2aeGWqQPF6nI&gclid=Cj0KCQjwl5jHBhDHARIsAB0Yqjw8ZhHVWT4fFOmL6zEKKggnBG1c6fYs-BNqVKvIgYzTJuGk_A2_iZUaAhf1EALw_wcB

[2] https://www.sciencedirect.com/science/article/abs/pii/S0140988323005972

Lessons on Entrepreneurship and Investing from Jeffrey Katzenberg

Crafting a narrative is a medium that transcends the entertainment industry. While the shift from media executive to entrepreneur and investor is one with many parallels across roles, few have succeeded in leveraging both lenses as aptly as Jeffrey Katzenberg.

Katzenberg spent a decade as chairman of Walt Disney Studios before co-founding and leading DreamWorks. Today, he invests in technology and digital media companies through his venture firm, WndrCo.

At a time when the overlap between entertainment and technology is top of mind for investors, the Jefferies team caught up with Katzenberg at TechTrek, the firm’s annual conference in Tel Aviv. The three-day event brought together leading global institutional and private capital investors to discuss the latest trends in technology and capital markets.

In conversation, Katzenberg shared his perspective on what he looks for in entrepreneurs in 2025, the role of storytelling, the revolution in AI, and more.

The following remarks have been edited lightly for clarity.

The Makings of a Strong Founder

As both an entrepreneur and a backer of entrepreneurs, Katzenberg has built a sharp sense of what makes a great founder — and what it takes to turn big ideas into real businesses.

“Every entrepreneur is a dreamer,” he shared. “What sets successful founders apart is perseverance. It’s a bumpy road, and you need determination and resilience to go along with ambition.”

From there, entrepreneurs must channel those traits into a story the market understands. Whether it’s attracting talent, raising capital, or winning customers, a clear and compelling narrative is what brings people together around an idea.

“In order to get people to believe in your dream, you have to be able to tell it,” he emphasized. “Whether you’re B2B or direct-to-consumer, storytelling is essential. Communication has to sit at the center of everything.”

With this, Katzenberg notes one of the tech industry’s unique strengths is its tolerance for failure. There’s an understanding that it may take two or three tries to make an idea work. This openness gives entrepreneurs the freedom to chase big ideas without fearing their career is over if one attempt falls short.

Balancing Optimism and Skepticism in Investing

In his storied career, Katzenberg has sat on both sides of the table, as an entrepreneur and as an investor. He said successful investing requires sharing some of a founder’s dreamer qualities but balancing them with a healthy dose of skepticism.

“As an investor, you need to be a dreamer yourself — while knowing not all dreams come true,” he said. “You have to balance those contradictory instincts: optimism and skepticism. Where you see opportunity, you also have to see risk.”

As co-founder of WndrCo, Katzenberg invests across three stages of a company’s life cycle: seed, venture, and growth. The firm’s portfolio has included Figma, Databricks, Robinhood, and other household names.

AI Holds Center Stage for Investors

One of the most dominant themes at this year’s Tech Trek — just as in recent years — was artificial intelligence. Katzenberg discussed what makes this moment in investing unique, and how the market is working to separate hype from impact.

“When we think about the agricultural revolution, the industrial revolution, or early computing, it took decades for those technologies to spread,” Katzenberg shared. “AI has changed everything in just two or three years. That has everyone excited, but investors are understandably nervous about a bubble. They don’t want to get ahead of themselves.”

Global private investment in AI — especially from corporations — has surged in recent years. In Q2 2025, funding for AI companies reached $47.3 billion[1] worldwide, even as research shows that enterprise investments have yet to deliver meaningful returns in most cases.[2] Still, the flow of capital shows no sign of slowing, particularly from U.S. investors, who put in nearly 12 times more than China, the next-largest backer.[3]

“The opportunities in AI touch every part of our lives, both professional and personal. Its impact is ubiquitous,” Katzenberg said. “Ultimately, I’m very optimistic.”

For more from Tech Trek — including interviews with top founders, executives, and investors like Jeffrey Katzenberg — visit Jefferies Insights.

[1] https://www.freewritings.law/2025/09/ai-investment-reaches-all-time-highs-the-state-of-ai-fundraising/

[2] https://www.axios.com/2025/08/21/ai-wall-street-big-tech

[3] https://hai.stanford.edu/ai-index/2025-ai-index-report/economy

In Direct Lending, Cash Flow (Coverage) is King

This will be the first publication in a series of articles by Jefferies Credit Partners designed to bring investors under the hood of underwriting private credit.

Private credit has rapidly evolved from a niche asset class into a significant force in the global lending landscape. It has grown at a rate of 15.6% per year between 2018 – 2024 and is projected to grow from a $2.1 trillion sector at 2024-end to an estimated $4.5 trillion by 20301.

Private credit may offer superior yields, bespoke deal structures, and a favorable risk-return profile, having delivered an annualized return of 9-10% with low standard deviation over the last two decades as measured by Cliffwater Direct Lending Index 2. Across several different credit cycles, sponsor-backed loans have maintained lower default rates than non-sponsor-backed loans3.

As investor interest in private credits grows, so too does the imperative of selecting the right manager, with the right process, to evaluate a potential borrower’s strengths and weaknesses.

One common way that many direct lenders run unnecessary risk is when they are overly reliant on EBITDA measures that don’t provide a clear view into a business’s cash flow or creditworthiness. In the process, they are exposing credit investors to more risk than they bargained for, especially amid rising global geopolitical and economic risks.

At issue is the Interest Coverage Ratio (ICR), which, like a P/E ratio, has the virtue of simplicity, and is commonly referenced as a predictor of a company’s creditworthiness.

Interest Coverage Ratio = Adjusted EBITDA / Interest Expense

Interest Coverage Ratio is a widely marketed metric in presentations, loan tapes, and diligence files for investors. However, the real standard that most lenders focus on, and investors should direct their attention to, is the Fixed Charge Coverage Ratio (FCCR). While being a useful proxy, we note that ICR can obscure more than it illuminates, by relying on an Adjusted EBITDA figure that does not answer the most critical question for every credit investor: Is this company generating enough free cash flow to service its debt?

EBITDA is increasingly subject to manipulation with companies adjusting it higher by, among other factors:

- Including pro forma cost savings or synergies

- Making run-rate or ramp adjustments – for example, including new stores or products that are not yet operational or profitable, or pulling forward revenue from contracts

- Classifying expenses such as recruiting, growth marketing spends, restructuring, and other employee costs (e.g., severance, legal, etc.) as ‘one-time costs’

Many leveraged loan credit agreements have an EBITDA definition that includes several pages of addbacks and adjustments, resulting in a materially higher “Adjusted EBITDA.” Interest coverage also does not account for capital expenditures, cash taxes, sponsor management fees, and other “below the line” cash costs that do not hit EBITDA, the sum of which can be material.

This is why lenders like Jefferies Credit Partners (“JCP”) rely on a measure called the Fixed Charge Coverage Ratio (FCCR), which they believe makes it more difficult for a company to engineer its way to creditworthiness.

Before delving into the details of FCCR, it’s worth reminding ourselves that credit has an asymmetric return profile, where a good outcome features capped upside (earning your coupon and recovering your principal) and a bad outcome is losing 100% of your principal. Unlike equity investments, credit does not offer winners with outsized returns to offset mistakes. Therefore, our view is that a good credit partner should focus on downside protection, with a disciplined and repeatable underwriting process.

Unpacking the Fixed Charge Coverage Ratio

FCCR is a key tool that is used to judge a company’s free cash flow. Here is how it is measured:

FCCR =

(Adjusted EBITDA – Cash Addbacks – Capex – Cash Taxes – Sponsor Fees – Other Below the Line Cash Costs) / (Interest Expense + Required Principal Amortization)

Note that the denominator in this equation also includes principal payments for the simple reason that this is cash a company does not have available to operate or invest in the business.

Fixed Charge Coverage Ratio (FCCR) vs. Interest Coverage Ratio (ICR)

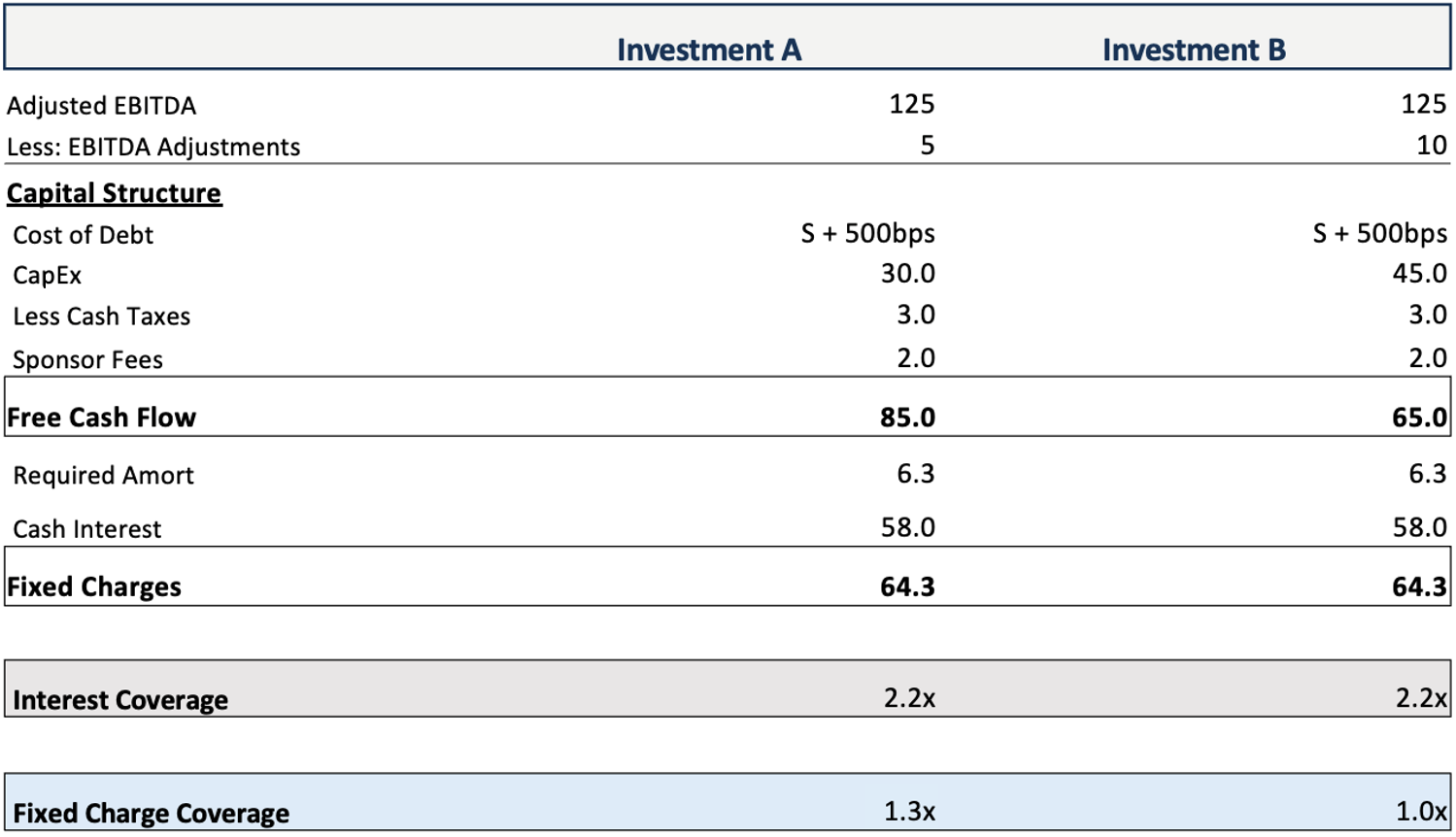

FCCR often paints a different picture of a company’s creditworthiness than ICR. Consider the following illustrative example of two similarly situated companies, both generating $ 125M of adjusted EBITDA, levered at 5x debt-to-EBITDA with the same interest rate and required amortization schedule. Both have the same Interest Coverage Ratio of 2.2x, while Investment A has a 0.3x higher FCCR due to lower capex requirements and fewer EBITDA adjustments.

If an investor were presented with these two credit opportunities, it would make sense, all things considered, for them to pursue Investment A over Investment B.

A Metric Credit Investors Need to Know

In recent years, the private credit market has become deeper and more diverse as investors have embraced a growing array of creative debt instruments.

Amid this growing complexity, straightforward and dependable measures of whether a company has the cash to cover its debt are essential. FCCR meets this test and remains a key tool for investors when assessing creditworthiness.

Endnotes:

- Source: Preqin – Private Credit Forecast 2030; Total AuM values relate to year-end figures and are referenced as calculated by Preqin for Global Private Credit (including Direct Lending, Distressed Debt, Other and BDCs, excluding all other semi-liquid funds). AuM figures exclude funds denominated in yuan renminbi.

- Source: Cliffwater 2025 Asset Allocation Report – referencing the Cliffwater Direct Lending Index which represents the actual historical asset class return for the 20 years ending September 30, 2024; gross of fees, on an unlevered basis.

- Source: LCD – US Leveraged Loan Default Rates (Period reviewed: Jan 2020 to Jul 2025)

Jefferies Credit Partners is a brand name for the asset management business conducted by the following SEC-registered investment advisers: Jefferies Finance, LLC, Jefferies Credit Partners LLC (“JCP”) and Jefferies Credit Management LLC (“JCM”), and together the Jefferies Credit Partners Platform (the “Platform”). Registration of an investment adviser with the SEC does not imply a certain level of skill or training. Jefferies Credit Partners is the investment management division of Jefferies Finance LLC (“Jefferies Finance”), a ~20-year-old joint venture founded in 2004 between Massachusetts Mutual Life Insurance Company (“MassMutual”) and Jefferies Financial Group Inc. (NYSE: JEF) (“Jefferies”). References to Jefferies are intended as Jefferies Financial Group Inc. global investment bank.

Past performance is no guarantee of future results. There is no guarantee that all of these opportunities will be available in the future. This document is furnished on a confidential basis for informational purposes only. The information contained herein must be kept strictly confidential and may not be reproduced or redistributed in any format without the express written consent of Jefferies Credit Partners LLC. These materials do not constitute an offer to sell or a solicitation of an offer to buy shares or limited partnership interests in any fund.

JCP is a division of JFIN. References herein to JCP refer collectively to JFIN, its relying advisers and affiliates. All information provided herein is for informational purposes only to illustrate the background and experience of the JCP investment team, which should not be relied upon to make an investment decision. This information is being furnished by or on behalf of JFIN and JCP on a confidential basis to the Recipient, which, other than on a need to know basis to the Recipient’s professional advisors, cannot be redistributed without the prior written consent of JCP. It is neither an offer to sell nor a solicitation of any offer to buy any securities, investment products or investment advisory services.

Certain statements herein constitute forward looking statements. When used herein, the words “project,” “anticipate,” “believe,” “estimate,” “expect,” “intend,” “target,” and similar expressions are generally intended to identify forward looking statements. Such forward looking statements, including the intended actions and performance objectives referenced herein, involve known and unknown risks, uncertainties, and other important factors that could cause the actual results, performance, or achievements to differ materially from any future results, performance, or achievements expressed or implied by such forward looking statements. Even if presented with numerical specificity, forward-looking financial projections are only predictions based on information currently available to JCP and JCP’s assumptions based on such information. Actual results may differ materially from any forward-looking financial projections contained herein. You are cautioned not to place undue reliance on any forward-looking statements or financial projections. No assurances can be given that the future results as projected will be achieved. All forward looking statements or financial projections in this document speak only as to the date hereof. JFIN expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements or financial projections contained herein to reflect any change in its assumptions or expectations with regard thereto or any change in events, conditions, or circumstances on which any such statement or projection is based. Furthermore, nothing contained herein is, or should be relied upon as, a promise or representation as to the future performance of any investment, vehicle or account managed or owned by JFIN.

Additional information about JCP and the information contained herein is available upon request.