India’s Energy Transition: 15 Insights from Jefferies’ Visit

Jefferies ESG Strategy Team has taken a close interest in India since our founding.

Most of the world’s future energy demand will come from emerging economies. The way these countries manage their resources will be key to achieving global net-zero goals – and India’s trajectory is particularly significant.

For years, India’s energy demands have been driven by coal growth, but today, the country is quickly diversifying. As the Indian equity market nudged past the $4 trillion mark, almost tripling in value since 2020, India’s position as a rising hub for low-carbon investment and innovation cannot be overlooked.

In November, the Jefferies ESG team visited India for a first-hand look at the country’s energy and social transition. We visited four cities and states: Mumbai (in Bombay), Delhi, Ahmedabad (in Gujarat), and Hazaribagh (in Jharkhand).

The trip yielded several important insights for the global investment community about this important economy and its emerging role in sustainable investment. Below are fifteen observations from our trip.

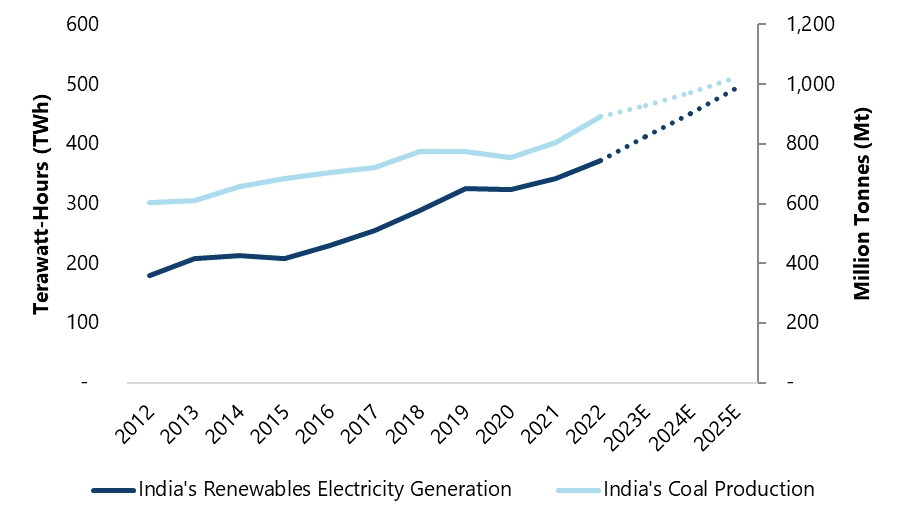

Two Competing Narratives: Both Thermal Coal & Renewable Power Generation Set to Rise

India has enough coal reserves for the next 200 years. The increasing demand for power, established technical expertise, strong state-owned enterprises (SOEs), indicate that coal consumption will continue to rise over the next two decades.

Simultaneously, the renewable energy sector will see tremendous growth in its share of the power mix. This growth will be supported by favorable policies and the country’s pursuit of energy security.

Though coal and renewables may appear to be contradictory forces, both are poised for robust growth through 2030 and beyond.

A Desire for Energy Independence

India’s aspiration for energy independence was a recurring theme during our visit. Internal coal reserves provide independence in the short term. In the medium to long term, renewables offer a path to greater energy independence, especially for sectors beyond power, such as transportation and industry.

Unwavering Policy Support for Energy Transition

Our meetings with government agencies and corporate leaders affirmed India’s unwavering policy support for the energy transition. There was no sense that current pro-renewable policies or subsidies would be scaled back, regardless of the outcome of the 2024 federal elections. This contrasts with many Western governments, where energy policy is currently dependent on the outcome of upcoming elections.

The Uniqueness of India’s Interconnected Grid

India’s Grid is one of the few in the world where new assets can be connected for transmission in 7-12 months. A singular grid, and policies which mandate the creation of high-speed networks where none exist, provide significant advantages. India’s Electricity Act should be studied by investors and policymakers around the world.

India’s Storage Options (e.g. Sodium Ion Batteries & Pumped Hydro)

Over the course of the trip, sodium ion batteries and pumped hydro were frequently highlighted as the two main alternatives to Li-Ion batteries, which remain expensive. Pumped hydro, in particular, exhibits favorable characteristics.

The Financial Health of India’s Power Distribution Companies

Entering the trip, the financial health of power distribution companies (DISCOMS) was cited as a major hurdle to renewable adoption. Their inability to competitively purchase RE power has weighed on India’s transition. We learned that policy interventions and reforms supporting DISCOMS have alleviated these concerns for generators and developers.

Self Sufficiency

Several of the companies we met are planning to expand their manufacturing capabilities down the supply chain (e.g., wafers, cells, ingots for solar panels). Driven by geopolitical concerns and external market unpredictability, both SOEs and private entities are seeking self-reliance. India aims to compete with China in green tech manufacturing – though most acknowledge it will be a decade-long journey.

National Green Hydrogen Mission

India believes that relative to China, the country was left behind on solar, batteries, and other forms of green manufacturing. India is keen to lead in green hydrogen. The National Green Hydrogen Mission, focusing on replacing significant amounts of grey hydrogen and building capacity, is central to this ambition.

The Creation of Carbon Markets

While the development of carbon markets is on the horizon for companies, it remains a medium-to-long-term consideration. The national scheme is still in early stages and is not yet significantly influencing corporate decisions. However, it is viewed as a future catalyst for making green hydrogen economically viable.

Business Strategy & India’s NDCs

Sovereign-level targets and Nationally Determined Contributions (NDCs) for India are clearly spurring action from both private companies and SOEs. As a reminder, India is planning for 500GW of installed low carbon capacity by 2030, and 50% of power gen to be from renewable sources by the same date. Those we engaged with reported strong financial positions and cash generating assets, with capital availability not an issue in allocating towards the transition. Many have and will continue to seek strategic M&A with European and US counterparts (see here and here).

Both the Private & Public Sector Are Actively Involved in Energy Transition

We met with Adani Green, Adani New Industries, and Adani Energy Solutions (all part of the Adani Enterprise Family), Reliance Industries, ReNew Power and HDFC Bank to name a few. All of these privately owned companies are actively investing in the transition.

We also engaged with NTPC, Power Grid Corp of India, Solar Energy Corp of India — Ministry of Renewable Energy. These organizations are either within the government apparatus or majority owned by the state. SOEs and state banks are clearly key drivers of India’s decarbonization efforts.

National Investment & Infrastructure Fund Limited (NIIFL)

The NIIFL is an innovative collaborative platform for pooling institutional capital in infrastructure. Its structure enables private capital to navigate local bureaucracy effectively and could serve as a model for both emerging and developed countries in funding transitions. Engaging with NIIFL presents attractive investment opportunities and a mechanism for de-risking investments.

And some signposts to track going forward . . .

New Coal Projects

Existing coal mines and power plants are unlikely to be retired early. Instead, investors should monitor when new coal projects stop being commissioned, as this will be a sign of accelerated progress towards net zero.”

Storage Costs

The price of Li-ion batteries has dropped 14% this year (c.$139/kWh). This is still not cost-effective enough for the country to capitalize on its mass solar potential. Monitoring the price of various storage options will be harbingers of further decarbonization in India.

Follow Experimentation in India

Panasonic and AES have recently announced an agreement to construct a 10MW energy storage facility in India. Many companies are also exploring sodium ion batteries. Developments in wind, pumped hydro, and hydrogen are all worth tracking. The country is at the epicenter of the growth versus carbonization challenge, and we expect innovative developments and solutions to continue emerging.

Prime Services C-Suite Newsletter – December 2023

Jack-of-all-Reads: A newsletter for multi-hat-wearing C-suite leaders and their key constituents.

Views from Capital Intelligence… Looking Ahead

Industry Insights:

Our newsletter, Jack-of-all-Reads, shares the latest and greatest insights in a brief read on a monthly basis. Please let us know of any comments or questions – we welcome and appreciate your continued partnership. Happy Holidays to all and we look forward to continuing our partnership in the new year.

Industry Insights:

- This month we collected insights from across our team on the industry outlook for next year. We look forward to discussing further with you in January.

- Outlook for hedge fund launches in 2024. The team is optimistic that we will see both established managers launching new products as well as an increase in specialist strategies which offer unique return streams, different factor exposures, or a combination of the two.

- Fundraising Environment. While multi-strategy and multimanager funds have been the primary group in the spotlight this year, questions remain around if demand will continue as LPs are more cognizant of fees. We expect to see:

- A continued interest and demand for uncorrelated, low beta, low net market neutral strategies with a focus on alpha generation.

- Increased appetite for healthcare and TMT strategies as rates start to decrease and indices hit rock bottom.

- More interest in tech as LPs have rotated out of the sector and are now underexposed.

- Interest for event driven strategies may increase as M&A activity rises.

- While we do see managers launching new products or a 2nd or 3rd vintage of an existing strategy, we are hearing feedback that some investors, particularly endowments and foundations, don’t have the liquidity to invest in the next iteration of a product given existing commitments to other drawdown/capital call types of investments they have made.

- As we are continue to see managers launching new products, managers need to be mindful around continuing to spend enough time on the flagship funds.

- Terms and Fees Outlook. Founders share classes have been becoming more illiquid. Nearly all groups have a lock and gate. See below for findings from a recent analysis our team conducted on the evolution of terms for newer managers; we always find it interesting to study the new launch environment as many of these managers set the stage for the innovation of terms for established managers launching new products.

- Management Fees. In 2023, the average founders share class management fee rose to 1.35%, up from 1.25% in 2022, which marks a return to 2021 levels when the average founders class management fee charged was 1.35%. Interestingly, in 2023, main share class management fees increased 40 bps from their 2021 levels (charging 1.60%), continuing their trend upward.

- Incentive Fees. The average inventive fees for founders share classes declined over 15% in 2023, down 230 bps from their 2021 levels. Conversely, the average incentive fee for main share classes rose to nearly 19.50%, up from 2022 when the average fee was 18.80% and in line with 2021 when the average fee was 19.50%

- Liquidity and Lock Ups. 87% of new launches imposed a lock-up in the founders share class, 2/3 of which were soft lock ups. The most common liquidity offered continues to be quarterly with a redemption notice of 60 days.

- Biggest Challenges to Launching in 2024. Heading into 2024, many firms are navigating the costs of keeping up with legal and compliance requirements given increased SEC activity, as well as grappling with how to attract and retain top talent.

- Multi-Manager Platforms. Will continue to actively hire and create competition for talent amongst emerging and established managers.

- Importance of Backing and Seed Capital. The barrier of entry to launching a fund is much higher now – from it being more expensive to run/operate a fund in this inflationary environment to there being less day one capital providers who are able to invest. Additionally, many provide deeper support and partnership that enable managers to scale.

- Thoughts from ODD. This year has been increasingly important from the operational due diligence perspective. The geopolitical environment and banking crises have prompted many to reevaluate how they view risks.

- The Latest on the ODD Landscapes. Questions from some ODD groups are becoming more complicated. Previously, managers seemed to have less of a grasp on what they needed to do, that information is now more readily available.

- AI in ODD: The Wave Of The Future. As managers are exploring different ways that they can leverage AI, ODD professionals are getting quickly educated on how to better understand and diligence it.

- Counterparty Risk. Diversification and vendor due diligence has been top of mind throughout our conversations with the community. The banking crises this year prompted a resurgence of putting processes in place to combat these risks however, most funds still only have one management company bank account in place.

- ODD Exam Format: Remains Hybrid. In a post-COVID world, the industry has been able to strike a balance of creating efficiencies through completing some components of ODD virtually and leveraging tools such as data rooms. The important exercise of visiting managers and participating in face to face meetings continues.

- Regulatory Changes. The SEC recently came out with their 2024 exam priorities which includes focus the new marketing rule, fiduciary duty rule,, and off channel communications. The SEC is currently aggressive in rule making and enforcement actions. There are new, existing, and upcoming disclosures, which groups will quickly need to adopt.

- Top of Mind in 2024: Private Fund Rule. This rule has been highly scrutinized as the advisor may no longer able to provide side letters or negotiations. It has brought on more comment letters than any period of time.

- Spotlight on Preferential Treatment. This will grant information and redemption rights as well as prohibit advisors from offering preferential redemption terms unless offered to all current or future investors. Potential solutions include creating customized reports sent via email or portal, or hosting regularly scheduled calls open to investors.

- The Latest on the ODD Landscapes. Questions from some ODD groups are becoming more complicated. Previously, managers seemed to have less of a grasp on what they needed to do, that information is now more readily available.

Please reach out to your Jefferies contact for more information on any of the topics above.

Spotlight on Content and Events:

Jefferies Launch 2025: Many of the trends we highlighted in last year’s Annual State of Our Union remained top of mind through 2023. Decision makers were revisiting their assumptions, and redefining their organizations in efforts to sustain themselves through challenging periods, or fuel growth amidst dislocation. Stay tuned for the Jefferies Launch 2025 series which will be released with both written and video components. In this series, we leverage expert views on what potential founders need to know now before launch including costs, the challenges, and potential upsides.

Interesting Service Provider Reads: Highlighting Topical Content from Industry Leaders

Lowenstein Sandler – The SEC’s Private Fund Adviser Rules Explained — Part 4: The Quarterly Statement Rule

Vigilant Compliance – 8 Important Considerations for Dual-Hatted CCOs

Waystone Compliance – SEC 2024 Exam Priorities for Private Fund Advisers

Jefferies Prime Services Contacts:

Mark Aldoroty

Head of Jefferies Prime Services

[email protected]

Erin Shea

Head of Business Consulting

[email protected]

Barsam Lakani

Head of Sales for Prime Services

[email protected]

Leor Shapiro

Head of Capital Intelligence

[email protected]

Shannon Murphy

Head of Strategic Content

[email protected]

Paul Covello

Global Head of Outsourced Trading

[email protected]

DISCLAIMER

THIS MESSAGE CONTAINS INSUFFICIENT INFORMATION TO MAKE AN INVESTMENT DECISION.

This is not a product of Jefferies’ Research Department, and it should not be regarded as research or a research report. This material is a product of Jefferies Equity Sales and Trading department. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the individual author and may differ from the views and opinions expressed by the Firm’s Research Department or other departments or divisions of the Firm and its affiliates. Jefferies may trade or make markets for its own account on a principal basis in the securities referenced in this communication. Jefferies may engage in securities transactions that are inconsistent with this communication and may have long or short positions in such securities.

The information and any opinions contained herein are as of the date of this material and the Firm does not undertake any obligation to update them. All market prices, data and other information are not warranted as to the completeness or accuracy and are subject to change without notice. In preparing this material, the Firm has relied on information provided by third parties and has not independently verified such information. Past performance is not indicative of future results, and no representation or warranty, express or implied, is made regarding future performance. The Firm is not a registered investment adviser and is not providing investment advice through this material. This material does not take into account individual client circumstances, objectives, or needs and is not intended as a recommendation to particular clients. Securities, financial instruments, products or strategies mentioned in this material may not be suitable for all investors. Jefferies is not acting as a representative, agent, promoter, marketer, endorser, underwriter or placement agent for any investment adviser or offering discussed in this material. Jefferies does not in any way endorse, approve, support or recommend any investment discussed or presented in this material and through these materials is not acting as an agent, promoter, marketer, solicitor or underwriter for any such product or investment. Jefferies does not provide tax advice. As such, any information contained in Equity Sales and Trading department communications relating to tax matters were neither written nor intended by Jefferies to be used for tax reporting purposes. Recipients should seek tax advice based on their particular circumstances from an independent tax advisor. In reaching a determination as to the appropriateness of any proposed transaction or strategy, clients should undertake a thorough independent review of the legal, regulatory, credit, accounting and economic consequences of such transaction in relation to their particular circumstances and make their own independent decisions.

© 2023 Jefferies LLC

Clients First-Always SM Jefferies.com

Jefferies Head of UK Banking on the Road Ahead for Investors

Jefferies recently sat down with Philip Noblet, Head of UK and Ireland Investment Banking at Jefferies. They discussed new inflation data and its potential impact on dealmaking. They also touched on next steps for private equity firms sitting on dry powder, and how investment banks can support corporate and sponsor partners through challenging times.

Their conversation came on the heels of October inflation data, where UK headline inflation fell sharply from 6.7% to 4.6%, the lowest in two years. This follows the Bank of England leaving its benchmark interest rate unchanged at 5.25% in early November. The central bank ended a run of 14 straight hikes in September, as policymakers keep their eye on a 2% target.

We just saw positive news on inflation in the UK. What do you think this means for interest rates and deal flow in 2024?

Whether you are a corporation or a private equity sponsor, you crave stability. And we’ve been through a period without stability, especially due to interest rate hikes. It’s made everyone very data dependent, and it’s hard to deal under these circumstances.

When stability returns – even at rates no one likes – everything level sets. Folks can make a plan.

On the private equity side, we have seen a quantum of funds raised over the last five years, and that capital hasn’t yet been deployed. All these players are coming back to the market, looking for opportunities. Many of these opportunities, albeit on the smaller side, have been in the UK public market.

On the corporate side, it’s all about CEO confidence. Whether you’re in the US or the UK, you need to feel confident in your own business, share price, and prospects.

We’re trying to provide folks with that confidence, supporting them with insightful ideas, bringing them thoughts from our equity division. We’re helping them understand what investors are thinking, and how investors will support public companies’ growth journeys, be it through acquisitions, disposals, or private equity sponsors.

I think we’re seeing stability return, albeit at higher rates, and that’s bringing signs of life to our pipeline for 2024.

When stability returns, but rates remain high, is private equity open to dealmaking?

I believe private equity will still do deals.

A partner said to me the other day, “if I’m borrowing money at 10 or 11 percent, what’s my rate of return?” The answer is 25 percent. Everything just goes up. It just makes the job more difficult. You have to incent management teams. You have to spend more time with the businesses. Private equity firms are really digging in, and they’re looking to acquire companies that can do the same.

Also, there is increased pressure to deploy capital. Investors aren’t paid to sit and twiddle their thumbs; they need to deploy their powder. There are a lot of bright folks in private equity, looking for opportunities, and we’re starting to see the industry gain momentum.

Do you think the return of deals will be driven by any sectors, in particular?

I think healthcare and tech is where it starts. These sectors have really held up through a really difficult 2022 and ‘23. I think deals in these sectors will continue to accelerate and become bigger – but we also need to question what ‘big’ means.

We were doing deals in 2021 for $10 billion. That’s a difficult deal to pull together today. But can we get to single-digit billion-dollar deals? Yes, and I think that primarily takes place through mergers.

Folks will use their shares, which they feel are undervalued, to buy other shares that appear undervalued. Taken together, these new valuations will be worth more than the sum of their parts. I think these single-digit billion-dollar deals will come back in the private equity world, as financing returns.

Our leveraged finance team is very confident about where the market’s going. We’ve seen some real positivity in the American and European leveraged finance markets, the private credit markets, and when you pair that with growing stability and confidence, it should inevitably lead to better deal flow and deals of larger size.

Investors are struggling to deploy capital. They’re struggling with liquidity events. How can investment banks like Jefferies be more creative? What are the strategies for helping sponsors unlock capital in the current environment?

One of the things we do well as a firm is put ourselves in the client’s shoes. We think, ‘what do the clients really want here?’

Sometimes, that means pushing them to explore. Sometimes they need to be brave, and that’s a lot easier when you have a thoughtful, insightful partner. Someone sitting across the table that has done it dozens of times before.

Jefferies made a wise decision in hiring one of the best continuation vehicle teams. You see many sponsors with high-quality portfolio companies that aren’t just willing to sell at a good price but put them into continuation vehicles. We’re at the forefront of that movement.

Fundamentally, though, it’s all about how you provide ideas to clients. In the end, a senior team bringing thoughtful ideas instills confidence in the client. And when the client knows advice is in their best interest, they’ll respond to it and take action.

Finally, IPOs have faced challenges in the US, even as activity returns. What do you see for the IPO market in the UK?

The reticence to invest in existing public companies is very high in the UK. To bring a public company to the UK, especially one in their growth stage, is challenging. We’ve seen share prices collapse, through no fault of the company. There just hasn’t been support and confidence from investors in public markets.

So, I suspect very little IPO activity in the UK. But that doesn’t mean we won’t go after them, when the opportunity is right.

When we connect with potential IPO candidates, we look at everything. How has private capital helped them? When is the right time to come to the public market? We give them real-time feedback, encouraging them to look at all their options, and ensuring they are in the best position.

Balancing Act: Navigating Conflicting ESG Challenges in Healthcare

In November, Jefferies hosted its annual Global Healthcare Conference in London. The event gathers leading healthcare, pharmaceutical, and medical technology executives from around the globe, joined by institutional, private equity, and venture capital investors, to discuss near- and long-term investment opportunities and key themes in global healthcare.

The following article is adapted from “ESG and Healthcare: Governing in an Era of Diverging Viewpoints”, a panel discussion hosted by Luke Sussams, Head of Sustainability and Transition Strategy, EMEA.

Panelists included Jos Lamers, Chairman, Bergman Clinics Group; Natalia Kozmina, Former Executive Vice President, CHRO & ESG Stewardship, Convatec; and Patrick Vink, Chairman, Essential Pharma.

As in other industries, there is a growing consensus that Healthcare companies with better Environmental, Social, and Governance (ESG) risk profiles tend to outperform their competitors.

- E: Energy efficiency and reduction of emissions remain critical to the industry’s longer term sustainability goals.

- S: Social priorities include access and affordability (particularly drug pricing concerns) as well as reliability of supply.

- G: Business ethics, product quality and safety remain top of mind when considering improved governance.

However, the umbrella acronym of ESG can fail to account for the challenge of reconciling the often-conflicting demands of ESG concerns. This complex interplay is particularly evident when balancing the need for an affordable and reliable supply of medicine against the imperative of environmental sustainability.

A panel discussion at the recent Jefferies 2023 Healthcare Conference called for a nuanced approach, blending innovation, collaboration, and carefully orchestrated funding strategies.

Environmental Sustainability vs. Access to Medicine

The healthcare industry, historically characterized by high energy consumption and significant waste generation, faces increasing pressure to reduce its environmental footprint. Initiatives like reducing greenhouse gas emissions and managing pharmaceutical waste are essential in combating climate change and environmental degradation. However, these initiatives often come with higher costs and operational complexities, which can inadvertently impact the affordability and accessibility of healthcare.

The Cautionary Tale of the Weight-Loss Miracle Drug

Amid the noise and excitement around the GLP-1 market, attendees of the November conference struck a note of caution. In our annual research report, the Jefferies Healthcare Temperature Check, 33 percent of the 600 senior leaders and investors expressed the view that substantial risks remain in the GLP-1 market. And they were proven right.

On the first day of the conference, November 14, Belgium banned the use of Ozempic for weight loss purposes, a decision set to last until the summer of 2024. The drastic action was taken in response to a global shortage of the diabetes drug, driven largely by its off-label use for weight loss. This shortage – affecting pharmacies not just in Belgium but also in the US, Canada, and other parts of Europe – necessitated the consideration of alternative medications to meet the needs of patients relying on Ozempic for its intended purpose: the treatment of diabetes. This action highlighted that national and supranational regulators are not afraid to take drastic action to protect reliability of supply.

Innovative Solutions for Sustainable Production

Innovation in manufacturing processes and supply chain management presents a viable solution. The adoption of renewable energy sources in production, coupled with efficient waste management systems, can significantly reduce environmental impact. Pharmaceutical companies are exploring ways to minimize their carbon footprint without compromising the efficacy and availability of medicines. We expect that technology will play a pivotal role in streamlining supply chains, making them more sustainable and efficient. With firm expectations of higher M&A levels, after two years of muted activity, identifying and executing strategic acquisitions and partnerships can also play a role in bolstering firms’ ESG credentials.

Bridging Financial Gaps for ESG Goals

The evolving landscape of ESG concerns in the healthcare industry presents both challenges and opportunities. Availability of capital has been a critical theme over the last 18 months and, once again, it is high on the agenda.

Over two thirds of conference attendees surveyed believe that the economic environment and outlook is having a ‘major adverse impact’ on the ability of healthcare companies to raise capital. Healthcare companies, both private and public, often face significant financial constraints when attempting to navigate the complexities of integrating ESG principles into their operations. However, with most predicting the slow resurrection of Debt and Equity Capital Markets in 2024, companies that continue to make the effort to integrate ESG will find capital most accessible.

How AI is Democratizing Access to Alternative Data

Today, professional and institutional investors have access to at least 100 times more consumer transaction data than they did just a decade ago.

That nets out to at least one trillion rows worth of consumer transaction data that can be parsed to gain insights into where a company, the economy, or markets are headed.

And this only represents a drop in a global ocean of alternative data that includes email receipts, social media posts, mobile phone location and other data that exists outside the realm of most corporate filings and official government reports. The $4.5 billion alternative data market has grown 50% annually for the past four years and it shows no signs of slowing down.

This data has become an increasing source of competitive advantage, especially for the quant-focused hedge funds that together manage well over $1 trillion, representing 29% of all hedge fund assets. Other fund managers we have spoken to have expressed concern they can’t keep up with this alternative data arms race, but recent advances in artificial intelligence are suddenly leveling the playing field by:

- Closing the Data Scientist Gap: As the amount of data has grown, so too has the number of data scientists investment firms need to hire to keep up with it. Imagine if you had two data scientists to extract value out of U.S. consumer data and then you got access to reams of consumer data from France. Well now you need a third data scientist, and ideally they need to speak French. Some firms have the resources to keep hiring. Most don’t. Fortunately, the advent of tools like Open AI’s Code Interpreter are making it easier for any investor to glean data insights. Some are already using Interpreter to upload and analyze data and to create tables and charts. You don’t even need to know exactly what you’re looking for. You could, for example, upload information on a retailer’s foot traffic, the weather in the region and social media data and prompt Interpreter by asking it, “Tell me what’s unusual or interesting about this data set.” A few years ago, only a trained data scientist could have done this exercise. Now, almost anyone can do it.

- Finding a Needle in a Research Haystack: If you are a buy side analyst who covers 100 energy companies, you could be getting reports on them from 20 sell side analysts publishing twice a quarter. That’s 4,000 reports, which collectively could exceed 40,000 pages. You will never read it all, but you don’t have to if you are using AI summarization tools, which can distill reams of research reports down into concise summaries.

- Cleaning up the Messy Work: Alternative data can be messy. Even if the data is structured, it may have inconsistent merchant names or product descriptions. Within a single dataset, there can be multiple data sources (for example, data from different point-of-sale systems) that is differently labeled. Making sense of unstructured data can be even more challenging, as there may be a significant amount of language processing required to extract insights. All of these tasks are time-consuming, require precision, and are more monotonous than higher-level insight generation. Thankfully, many of these tasks represent perfect applications for large language models. For example, performing entity resolution (mapping merchant descriptions to tickers in consumer transaction data) can be largely automated with AI tools. This allows analysts to focus on higher-level analysis of the data, instead of menial data cleansing.

In recent years, investors have been both wowed and overwhelmed by the amount and type of alternative data that’s available. But AI is democratizing alternative data access, making it easier to find, to make sense of it, and most importantly to deliver actionable investing insights.

Spenser Marshall is the Chief Data Officer of Sundial Data, a direct data sales subsidiary of M Science, a portfolio company of Leucadia Investments, a division of Jefferies Financial Group.

Lance Uggla’s Roadmap: Insights for Today’s Entrepreneurs

In September 2023, Jefferies hosted its seventh annual Tech Trek, Israel’s largest institutional investor conference. The three-day event connects leading global investors with the Israeli tech ecosystem through a series of panels, presentations, and meetings.

Jefferies CEO Rich Handler sat down with Lance Uggla, co-founder of Markit and current CEO of BeyondNetZero, to glean insights for emerging entrepreneurs. Their discussions covered traits and priorities that lay the groundwork for success, the pros and cons of going public, climate-focused investing, and more.

Lessons from a Seasoned Entrepreneur

In 2003, Uggla founded Markit, a financial information and services company. The company grew to more than 4,000 employees and 21 global offices before merging with Information Handling Services (IHS) to form IHS Markit. The combined entity later joined S&P Global in a deal valued at approximately $44 billion.

In his conversation with Handler, Uggla retraced his evolution from budding entrepreneur to seasoned executive. The most important ability he honed along the way? Focus.

“Focus on two or three things and do them exceptionally well,” Uggla advised. “When you’re thirty, you’re filled with ideas, but it’s where you really focus that you achieve great results.”

Reflecting on the traits he values in modern entrepreneurs, Uggla underscored the importance of great character. “I love to meet an entrepreneur who shows integrity,” he said. “Enthusiasm, personal manners, and grace are a great foundation for success.”

Beyond personal traits, Uggla values entrepreneurs with a clear vision for profitability. A compelling product is key, but a solid financial model differentiates the best founders.

The Double-Edged Sword of IPOs

A decade after its founding, Markit filed for an initial public offering, making its debut in June 2014 at $24 a share.

The move to public markets can be challenging, especially in the current IPO climate. Drawing on his own experience, Uggla offers important advice: find the right partners.

“Choose someone who wants to be with you for the journey, not just the event,” Uggla said. “It’s tempting to choose from the league tables, but you need a partner who really understands you and speaks your language.”

Whether in search of legal counsel or investment bankers, aligning with trustworthy, long-term partners was key to Uggla’s success.

On the experience of being publicly traded, Uggla recognizes the benefits and drawbacks.

“When you go public, you create a currency. You have a real valuation,” Uggla shared. “This opens up a lot of opportunities that aren’t available in private markets.”

He cautioned founders, however, that this advantage brings the challenges of quarterly reporting, increased expenses, and regulatory scrutiny. These obligations can limit your agility, sometimes impeding the pace of business.

Building Ties with Investors, Public and Private

Uggla reiterated the importance of building ties with investors, be it in the private or public domain. He also emphasized the distinctive nature of these relationships.

Private equity investors, Uggla said, feel like partners. They understand your business deeply and participate actively in major decisions. Public investors still expect exceptional results, but they’re less connected to your strategy.

“When you go public, you become a grown up, and the way you communicate has to change,” Uggla advised. “It’s professional investors versus nonprofessional investors. Both deserve respect, but you have to learn how to bridge the gap.”

Uggla’s Journey to Climate Investing

Uggla finished by highlighting his passion for climate investment, which originated with IHS Markit. Uggla had envisioned a specialized division named ‘Beyond Net Zero’ within IHS Markit, which would produce unique energy transition solutions, but the opportunity was shelved during the company’s sale.

The concept evolved into a fund with the same name, in collaboration with General Atlantic.

With new partners, including Lord John Browne, an energy industry veteran, Uggla raised a $3.5 billion fund. Today, BeyondNetZero is at the forefront of growth equity for climate-based investing.

From founding Markit to spearheading innovative climate investment strategies, Lance Uggla’s career is a testament to adaptability, focus, and strong partnerships. His insights offer valuable guidance to young entrepreneurs, underscoring the importance of character, collaboration, and adept communication in building successful ventures.

Jefferies’ Economist Mohit Kumar Sees Bull Market Potential in 2024

Jefferies sat down with Mohit Kumar, Chief Economist and Strategist for Europe, at the firm’s 14th annual Global Healthcare Conference in London. They discussed central bank policy, the potential for recession, the latest inflation and employment figures, the best asset classes for 2024, and more.

Their conversation comes on the heels of October inflation data, where US headline inflation fell from 3.7% to 3.2%. The drop reduces the likelihood of an interest rate hike at the Federal Reserve’s year-end meeting. The United Kingdom also saw a sharp drop in annual inflation, from 6.7% to 4.6%.

We recently received October inflation data from the United States and United Kingdom. Where are we in the global battle against inflation?

I think we are still some distance from the central bank target of two percent, but we’re trending in the right direction. Inflation is moving lower. I think we will be below two percent by the end of next year in the US. For Europe and the UK, it might take slightly longer, but by the end of 2025 or early 2026, we could be below two percent as well.

What is important from markets and central banks’ point of view is that, in the medium term, inflation expectations are below two percent.

Should we expect a recession in 2024 in Europe?

Recession is a strong word. It means two quarters of negative GDP growth. In Europe, my best case is we see flat or zero growth over the next two quarters. Maybe we avoid recession; it’ll be very close. Even if we get a recession, I suspect it’ll be a mild one. A slow down rather than a proper recession.

Growth is slowing down. Inflation is slowing down. What does this mean for interest rates – have we seen the end of hikes?

I definitely think so. Thinking about the three main central banks – the Federal Reserve, European Central Bank (ECB), and the Bank of England – I believe all three are done with rate hikes.

Now, of course, these decisions are data dependent. If the data surprises, we could see more hikes, but the bar for another hike will be high. My view is that we see a slowdown going forward, which means there’s no need from the Fed, ECB, or Bank of England.

The next question is: when will they cut?

For the Fed, we have a presidential election cycle coming. The Fed wants to be neutral during an election cycle, so they will be very reluctant to cut rates unless we see a material slowdown. For ECB, you see the unwinding of quantitative easing (QE) policy and interest rates. My best guess is they will announce the end of Pandemic Emergency Purchase Programme (PEPP) investments next June and cut rates in the third quarter. For the Bank of England, again, it’s a summer or post-summer story.

All said, the direction of central banks is clear: rate hikes are done. Rate cuts are the next step.

Employment has shown resilience globally. What do you expect for jobs in the coming year?

The job picture has been very resilient overall, but if you look at the details, it’s sector specific. There’s been resilience in small and medium enterprises (SMEs), or companies with fewer than 100 employees. In the US, from pre-COVID to today, there’s been a 120% increase in SME new hires. In the UK, it’s close to 140%.

The obvious question, then, is why is the SME sector so strong? I’d offer three reasons.

First, the pandemic – during COVID, the government paid us money to stay home, and people formed new companies. New company formation and SME new hires went through the roof.

The second reason is excess cash. The SME sector is flush with cash. That means the Fed or ECB can hike rates, and the impact on companies’ balance sheets will be limited. The central banks’ transmission mechanism is not flowing through.

The third reason is end consumers, who also have excess cash. Our level of excess savings remains very high. Our expectation was that by Q3 2023, the lower-income cohort would run out of excess savings. Three weeks ago, we saw revisions to the national account data which showed excess savings as double our initial predictions.

The expectation that a slowdown would start in Q3, and that’s when the labor market would crack – I think this has all shifted forward by 3 to 6 months. I think the labor market will slow down, but it’s a late Q4 or early Q1 story. Jobs will remain strong for a bit longer.

When we see cracks in the labor market, I don’t expect a deep recession, meaning 8% unemployment. I expect unemployment to peak around five percent. This would be a mild recession or slowdown in the US and Europe, not a deep one.

Is there any market where you expect especially strong growth? A star of 2024?

A few markets. I’d first highlight the US tech market, which I think can continue to perform strongly – with the exception of maybe Q1, where we may see short-term growth concerns. Credit is another strong market. Clearly the investment grade market should do very well next year, compared to equities. Of course, you have to focus on total yield rather than just a spread basis, but I’m confident credit can continue to perform.

Emerging markets (EM) is another area that should perform. If the dollar weakens and the Fed starts talking about rate cuts, EM can do quite well. With EM, you always have to pick your countries, but as an overall asset class, it should perform quite well next year.

Broadly speaking, we’re going to see a fixed income market over the next year. Whether you’re looking at credit or sovereign, these are the asset classes you want to own next year.

Prime Services C-Suite Newsletter – November 2023

Jack-of-all-Reads: A newsletter for multi-hat-wearing C-suite leaders and their key constituents.

Preparing for Year-End with SEC Updates, Trade Agreements, and Insurance Trends

Our monthly newsletter for multi-hat-wearing C-suite leaders covers the latest and greatest insights across the hedge fund industry.

Industry Insights:

- Increased Activity: SEC Stats and Priorities. The SEC has released their 2024 exam priorities and figures around enforcements in 2023 showing an uptick in overall activity. Clients are engaging their compliance and legal teams to assist in navigating various key line items, performing gap analyses, and thinking about which processes will need to change to be compliant with the new rules.

- Exam Priorities. The SEC released their priorities which are primarily focused on new and recent rulings from the commission. Many new regulations have been finalized this year such as the Private Funds Advisory, Cyber Security, and Short Selling rules. Notably, ESG is no longer on the exam priority list despite the finalized Fund Naming rule.

- Yearly Increase. Over the past three years, there has been a 20% increase in enforcement actions by the SEC. In contrast, the amount of fines generated has been less linear with $1.4 billion fewer fines generated in 2023 compared to the previous year and $1.2 billion more in fines this year than in 2021.

- Trade Agreement Best Practices. Going into year-end, trade agreements may be top of mind for some COO and CFOs. Some key considerations may include:

- Maintain levels of uniformity. When building trade agreements, infrastructure and operational considerations should be taken into account. This is especially important in the world of SMAs to maintain certain sets of uniformity from the trading standpoint.

- Have a short and long term view. COO and CFOs should aim for an overall picture of what the business may need as it evolves across asset classes. Be prepared for any sudden changes in plans, and ability to diversify where it makes sense.

- Build relationships across the firm and across asset classes. There is an importance in having these connections and viewing these relationship with the ability to shift and change.

- Ask the right questions. There is a need to understand what’s in your documents, where items may be lacking and what is the rational around what you’re doing. Additionally, groups should ensure their legal counsel is also involved in the process.

- Thanks to Lowenstein Sandler for providing their latest insights on the above.

- Alternative Data: As funds continue to be consumers of alternative data, due diligence on vendors, keeping track of progress of the data, and understanding risks associated with these providers is top of mind. Groups are spending more time understanding needs around oversight and governance of these services as well as keeping inventories of who’s using it and how it is being used.

- Building Projects and Gaining Support. Many groups are starting to think about how to remain competitive in terms of data and are beginning to implement new processes. It can be critical to the implementation of these projects that users can understand the complexity of data and have the ability to achieve standardization around the data.

Please reach out to your Jefferies contact for more information on any of the topics above.

Client Corner:

Insurance Trends. Given the increase in enforcement actions by the SEC and higher legal fees, many fund managers are opting for increased D&O and E&O insurance coverage. Despite this, Fieldstone insurance Group noted a decrease in pricing overall per million dollars of coverage in the hedge fund market. Interestingly, this is not seen in other parts of the alternatives industry such as insurance coverage for PE or VC funds. Additionally, cyber insurance coverage is still growing across the client base and service providers in the space with close to half of funds purchasing coverage.

Spotlight on Content and Events:

Israel’s Economy and Financial Markets: Navigating Wartime.

Wednesday, November 29th, 10:00–11:30am ET / 15:00–16:30 GMT / 17:00-18:30 IST

Join us as for a webinar hosted by the Israel Hedge Funds Association (IHFA) and Tel Aviv Stock Exchange (TASE) to highlight Israel’s Economy and Financials during Wartime.

Bank of Israel Governor will discuss the economy and role of the central bank, TASE CEO on the importance of the stock exchange and then Natti Ginor (JEF Head of Israel IB) will interview the CIO of Migdal (+$90 billion insurance and pension fund) and Co-Founder & Managing Partner of Sphera Funds (one of Israeli’s largest hedge fund managers).

Interesting Service Provider Reads: Highlighting Topical Content from Industry Leaders

Apex – Regulatory and compliance updates for Cayman Islands Q3 2023

BlueFlame – Client Debrief: A Chaotic Weekend for OpenAI and What it Means for Announcements from DevDay 2023

Seward & Kissel – FTC Imposes New Data Breach Notification Requirements

Jefferies Prime Services Contacts:

Mark Aldoroty

Head of Jefferies Prime Services

[email protected]

Erin Shea

Head of Business Consulting

[email protected]

Barsam Lakani

Head of Sales for Prime Services

[email protected]

Leor Shapiro

Head of Capital Intelligence

[email protected]

Shannon Murphy

Head of Strategic Content

[email protected]

Paul Covello

Global Head of Outsourced Trading

[email protected]

DISCLAIMER

THIS MESSAGE CONTAINS INSUFFICIENT INFORMATION TO MAKE AN INVESTMENT DECISION.

This is not a product of Jefferies’ Research Department, and it should not be regarded as research or a research report. This material is a product of Jefferies Equity Sales and Trading department. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the individual author and may differ from the views and opinions expressed by the Firm’s Research Department or other departments or divisions of the Firm and its affiliates. Jefferies may trade or make markets for its own account on a principal basis in the securities referenced in this communication. Jefferies may engage in securities transactions that are inconsistent with this communication and may have long or short positions in such securities.

The information and any opinions contained herein are as of the date of this material and the Firm does not undertake any obligation to update them. All market prices, data and other information are not warranted as to the completeness or accuracy and are subject to change without notice. In preparing this material, the Firm has relied on information provided by third parties and has not independently verified such information. Past performance is not indicative of future results, and no representation or warranty, express or implied, is made regarding future performance. The Firm is not a registered investment adviser and is not providing investment advice through this material. This material does not take into account individual client circumstances, objectives, or needs and is not intended as a recommendation to particular clients. Securities, financial instruments, products or strategies mentioned in this material may not be suitable for all investors. Jefferies is not acting as a representative, agent, promoter, marketer, endorser, underwriter or placement agent for any investment adviser or offering discussed in this material. Jefferies does not in any way endorse, approve, support or recommend any investment discussed or presented in this material and through these materials is not acting as an agent, promoter, marketer, solicitor or underwriter for any such product or investment. Jefferies does not provide tax advice. As such, any information contained in Equity Sales and Trading department communications relating to tax matters were neither written nor intended by Jefferies to be used for tax reporting purposes. Recipients should seek tax advice based on their particular circumstances from an independent tax advisor. In reaching a determination as to the appropriateness of any proposed transaction or strategy, clients should undertake a thorough independent review of the legal, regulatory, credit, accounting and economic consequences of such transaction in relation to their particular circumstances and make their own independent decisions.

© 2023 Jefferies LLC

Clients First-Always SM Jefferies.com

The Global Tech Landscape: Uncovering New Investment Opportunities

In September 2023, Jefferies hosted its seventh annual Tech Trek, Israel’s largest institutional investor conference. The three-day event connects leading global investors with the Israeli tech ecosystem through a series of panels, presentations, and meetings.

Jefferies sat down with Bernard De Backer, Partner in StepStone Group’s private equity division, to hear his perspective on tech sector performance, regional disparities in the global economic recovery, untapped investment opportunities in Europe, and more.

Tech Exposure: Is Concern Warranted?

Investors have worried about their tech exposure amid nearly two years of sector volatility. Tech shares fell over 30% in 2022, outpacing the broader market’s decline, and these challenges bled into private markets. By Q2 2023, year-over-year tech valuations were down 14% in Series A rounds, 9% in Series C rounds, and 33% in Series D rounds and above.

Today, a strong earnings quarter and resilient economy may suggest a tech sector rebound. As we approach 2024, should investors still be concerned about their exposure?

De Backer, advising clients from sovereign wealth funds to foundations, is cautiously optimistic. Tech forms nearly a third of his clients’ exposure, a proportion he believes may grow.

“Medium to long-term, I expect our clients to remain supportive of tech investing. Their exposure may rise even further,” De Backer shared. “Tech and software investments remain very compelling.”

Acknowledging valuation challenges, he underscored the resilience of private markets, highlighting companies with solid financial models like software as a service (SaaS). These businesses fared much better than their growth-oriented and public market counterparts. As markets rebound, De Backer expects private tech companies with reliable models to lead the charge.

The Global Recovery: Europe’s Untapped Potential

De Backer discussed regional disparities in the global recovery, with the U.S. leading the way. The U.S. reported 4.9% GDP growth in Q3 2023, more than double the second quarter’s pace. The country’s GDP recovery and labor markets continue to outpace other advanced economies.

“I think the U.S. is five or six months ahead of Europe in their tightening cycle,” De Backer said. “The U.S. was coming off a very robust market, and it created enduring tailwinds and financing. It remains the world’s most active market.”

October inflation data boosted the United States’ economic momentum, as headline inflation fell from 3.7% to 3.2%. The drop reduces the likelihood of an interest rate hike at the Fed’s year-end meeting. Similarly, in the United Kingdom, a sharp drop in annual inflation from 6.7% to 4.6% reduced pressure on the Bank of England to continue aggressive measures.

Despite its tepid recovery, De Backer still sees untapped opportunities in broader Europe. StepStone aims to capitalize on several key advantages in the region:

- Europe boasts a larger pool of software engineers than the U.S. With lower median salaries, they represent a cost-effective talent base for tech entrepreneurs. This is a driving factor in Europe’s growth as a hub for new startups. The region is now home to over 150 ‘unicorns’.

- Europe has fewer specialized tech investors than the U.S., leading to lower overall market capitalization. This creates opportunities for valuation arbitrage that seasoned investors like StepStone Group can seize.

- There’s room for consolidation in Europe’s tech market. Unlike the U.S., many European tech niches and platforms are still independent. There’s great potential for strategic M&A to drive growth and returns.

Secondary Markets and GP-Led Transactions

The conversation closed on the topic of secondary markets. As IPOs and dealmaking remain subdued, secondary markets have stayed active, especially for GP-led transactions.

“Secondary markets are attractive. If you look at the ratio of money raised to opportunities, it’s a very strong ratio,” De Backer said. “A big opportunity set for investors.

De Backer emphasized the appeal of diversified LP positions, rather than investing too much in concentrated GP vehicles. Still, under the right circumstances, transactions with general partners remain attractive.

“We look for strong assets combined with a very strong GP. That combination is critical.”

Bernard De Backer’s insights offer tempered optimism, undergirded by resilient private markets and unrealized growth in Europe. As developed economies rebound, challenges are expected, but investors focused on sustainable business models and under-penetrated markets will find exciting new avenues for growth.