The US IPO Market is Rebounding. What Does This Mean for Canada?

In March 2024, the Toronto Stock Exchange (TSX), Canada’s largest platform for initial public offerings (IPOs), marked a whole year without a new corporate listing. This prolonged drought follows a 30-year low in 2023, when Canada’s top exchanges saw just one listing.

Canada’s struggles are part of a wider global slump in public offerings. In 2023, the world’s 15 leading exchanges saw a significant decline or complete pause in listings. However, entering the second quarter of 2024, the IPO markets in the United States and EMEIA are beginning to thaw, amid a series of successful, high-profile new listings.

This raises an interesting question: Is Canada also on the brink of overcoming its IPO drought, or is the market in for further hardship through the second half of 2024?

Jefferies sat down with Erik Charbonneau, Head of Canadian Equity Capital Markets, to discuss the market for Canadian IPOs. Although the pace of recovery may not match that of the United States, Charbonneau is optimistic about a resurgence in new listings and investor enthusiasm.

The following Q&A has been lightly edited for clarity and length.

After a historic drought in IPOs, are there reasons for optimism for 2024 and ‘25?

For all intents and purposes, there has been no IPO activity in Canada for the last couple of years. Now, the conditions are in place for activity to pick up again.

Equity markets are performing well, with North American indices, including the TSX, up this year. Volatility remains muted. And we’re seeing new issue activity in the US. We’re going to see rate cuts this year, and if the economy keeps trending in the right direction, I expect Canadian IPOs to see a resurgence.

The truth is: Canada’s IPO market is open today. It will just take a very high-quality company to be successful. We’re watching this in the US, where strong companies are priced well and trading well in the aftermarket. It’s going to take a while, and everyone needs to remain patient, but I think activity picks up in the back half of this year.

What does this recovery look like?

If you look at the past two decades in Canada – and you exclude the unusual pace of the COVID period – the best years saw a mid-teens number of corporate IPOs. In a less busy year, you might see mid-single digits. Between those two bookends is what I’d describe as a “normal market environment.”

Now, if we reached mid-single digit IPOs in 2024, I’d consider that a success. It would signal a rebound.

The key – though it’s almost a cliche to say it – will be high-quality, well-executed IPOs reopening the market. They need to be priced at a valuation that is attractive to issuers and investors. They need to perform well in the aftermarket. And, importantly, they need to attract the right shareholders: a broad and experienced set.

If we can achieve this with the first few IPOs out of the gate, it will prove that the time is right for issuers to go public in Canada again.

Where do you anticipate activity returning in Canadian markets? Any sectors, in particular?

In Canada’s recent history, the IPO markets have attracted a broad range of sectors – technology, healthcare, energy, industrials.

There are a handful of exciting healthcare and tech prospects that Jefferies is tracking closely, but I also know of several traditional energy companies eyeing public markets.

While IPOs always skew towards sectors with strong momentum, I expect Canadian listings to rebound with a broad range of companies.

What deals are getting done in the face of this prolonged IPO drought?

When a major asset class like IPOs isn’t performing well, it forces sponsors to look for alternatives. They are looking to monetize or partially monetize their positions so they can return money to their limited partners (LPs). How can they leverage M&A or money markets when IPOs are off the table?

Continuation vehicles are a very popular option, especially for longer assets. Sponsors can partially monetize, return capital to their LPs, and pursue future fundraising opportunities.

In other cases, sponsors are remaining patient. They have stretched out their cash reserves by recasting budgets, slowing down growth, and waiting for the right moment for a public exit or growth financing. For issuers in need of immediate growth capital, they have looked to private markets – but those have also experienced a challenging stretch.

–

Canada remains a dynamic ecosystem, abundant with strong and innovative companies. Although the past two years have been profoundly challenging for Canadian public markets, trends in the US and Europe are showing green shoots. Experts like Erik Charbonneau see a rebound on the horizon.

Erik is a Managing Director and Head of Investment Banking and Equity Capital Markets – Canada for Jefferies. He was part of the founding team for the recently opened Jefferies offices in Canada. Over the course of a 30-year career, Erik had originated and executed capital markets transactions for client across numerous industries in both Canada and the U.S. Erik has run sector ECM desks in financials, private placements and healthcare and has been responsible for equity capital markets teams in Canada (head of ECM) and the U.S. (co-head of ECM for the Americas). Erik holds a B. Comm from McGill University. You can contact Erik: [email protected] or +1 (416) 847-7395

Rapyd’s Growth and the Future of Fintech: Insights from Arik Shtilman

In September 2023, Jefferies hosted its seventh annual Tech Trek, Israel’s largest institutional investor conference. The three-day event connects leading global investors with the Israeli tech ecosystem through a series of panels, presentations, and meetings.

During the conference, Jefferies spoke with Arik Shtilman, co-founder and CEO of Rapyd, a global payments and fintech platform based in London. Rapyd offers businesses a comprehensive solution for integrating payments, commerce, and financial services into any application.

Shtilman spoke to Rapyd’s founding and its path to success, the rise of embedded finance and fintech across various sectors, the significance of cross-border sales and compliance for modern companies, and more.

The conversation followed Rapyd announcing an acquisition of a piece of PayU from Prosus, aiming to scale its fintech-as-a-service platform.

Spotting a Gap in the Market: Rapyd’s Journey to Success

Initially, Rapyd was conceptualized as a consumer e-wallet to challenge PayPal. The startup pivoted when Shtilman noticed a significant gap in the financial services space. While there were plenty of specialists, no one offered a comprehensive platform that integrated all financial capabilities — from issuance and disbursement to compliance — into a seamless, all-in-one solution.

“Every company in the sector was a one-trick pony,” Shtilman shared. “It mirrored the early cloud computing era, where there were hosting services but no infrastructure. Our vision was to create the world’s largest infrastructure for financial services, all baked into one platform.”

From there, Rapyd grew rapidly. By 2022, just seven years after its founding, it was valued at $15 billion, becoming the most valuable Israeli tech unicorn ever.

How Embedded Finance and Globalization Pushed Fintech Forward

Fintech has grown rapidly, on track to become a $1.5 trillion sector by 2030. Despite a challenging 2022 and 2023, as funding and deal volume slipped, the sector’s long-term prospects remain very strong.

Shtilman identifies two trends driving the sector’s momentum: the rise of embedded finance and the increase in cross-border commerce.

“Every single company wants to become a Fintech,” Shtilman said. “Look at ApplePay, Google Pay, Samsung Pay – all these tech companies adding embedded finance. They’re realizing that the best way to monetize customer relationships is financial services.”

For most businesses, however, building fintech capabilities from scratch isn’t feasible. They just want to offer these services. That’s where Rapyd found its edge: providing an adaptable fintech platform that enables companies to offer financial solutions without developing them.

The second trend is the growth of international businesses – and the host of compliance challenges they face.

“Almost every business today operates internationally, and they need a platform that can manage varying compliance standards, currencies, and payment methods,” Shtilman explains.

Rapyd uses AI to automate these processes, bringing efficiencies to companies operating across global markets, including emerging economies.

What’s Next for Rapyd?

With a fresh rebrand and recent acquisitions under its belt, Rapyd is ready to keep expanding. How has the company maintained its momentum, as it transitioned from startup to global leader?

“One of the biggest challenges in scaling from five to 1,500 employees is preserving that startup spirit—avoiding bureaucracy and keeping everyone agile,” Shtilman shared.

To tackle this, Rapyd restructured into smaller business units that mimic the flexibility and rapid execution of startups, ensuring the company remains nimble and retains its momentum despite its size.

–

As Rapyd embarks on its next phase, the global fintech market’s trajectory remains a critical backdrop. The sector is expected to rebound in 2024, following two challenging years. The entry of more companies into this space signifies not only the sector’s growth but also the ongoing globalization of economies. Shtilman’s insights offer a roadmap for navigating the always-evolving sector, highlighting the importance of innovation and adaptability in achieving sustained growth.

The Evolution of Sports Media with Minute Media Founder Asaf Peled

In September 2023, Jefferies hosted its seventh annual Tech Trek, Israel’s largest institutional technology investor conference. The three-day event connects leading global investors with the Israeli tech ecosystem through a series of panels, meetings and curated networking events.

During the conference, Jefferies spoke with Asaf Peled, founder and CEO of Minute Media, global technology and content company specializing in sports and culture. Minute Media’s proprietary tech platform enables the creation, distribution and monetization of digital content experiences. They own and operate leading sports content brands, including Sports Illustrated, The Players’ Tribune, FanSided, and 90min, while also providing sports highlight rights through Minute Media’s most recent technology acquisition of STN Video.

Peled discussed Minute Media’s growth, acquisitions, and the potential for an upcoming public offering; the future of sports media; the Israeli tech ecosystem; and more.

Following the interview, Minute Media completed a new round of funding that valued the company at over $1 billion, and it announced the acquisition of STN Video, a sports content distributor, for $150 million. The company also struck a 10-year licensing deal with

Authentic Brands Group for the publishing rights to Sports Illustrated.

Note: Peled’s comments on Israel were made before the events of Oct. 7. The ongoing conflict may influence the region’s tech ecosystem and investment landscape.

Minute Media’s Founding: Disrupting the Sports Content Ecosystem

Over a decade ago, Peled and his co-founders spotted an opportunity to shake up sports content. They noticed the existing ecosystem lacked modern traits: short-form content accessible on a tech platform, where fans could also contribute as creators.

“We founded Minute Media on two core elements,” Peled shared. “First, developing tools for fans, creators, and athletes to participate in content creation. Second, building our own content management and distribution platform, so we weren’t over reliant on social media.”

A key growth strategy for Minute Media was forming partnerships with athletes, like Derek Jeter, Co-founder of The Players’ Tribune. These collaborations, tapping into the athletes’ global recognition, enhanced Minute Media’s credibility with both athletes and fans. This approach was particularly beneficial for The Players’ Tribune, a pioneering platform for athlete-driven content creation, which Minute Media acquired in 2019.

The Evolution of Sports Media: From Broadcast to Mobile

When Minute Media started, sports media was a mature industry with a rich legacy – but it was beginning to feel outmoded in its content creation and delivery methods. Predominantly focused on broadcast media – including TV, radio, and desktop platforms – it wasn’t meeting the evolving preferences of younger audiences.

“We noticed a paradigm shift in the user base: in the ways they create, engage with, and consume content,” Peled remarked.

As sports fans became younger and more global, their consumption patterns shifted towards mobile, favoring short-form content over traditional broadcasts. Minute Media recognized this trend early and, through their innovative platforms, played a key role in driving it forward.

What’s Next for Sports Media?

Since its founding, Minute Media has watched the sports media landscape continue to evolve. While mobile-driven, fan-generated content remains central, new areas are emerging.

Sports betting, for example, has soared to new heights. The industry posted a record $10.92 billion in revenue in 2023, up 44.5 percent year over year. The convergence of sports betting and content is also expanding, with companies like FanDuel now offering a wide array of podcasts and shows.

Minute Media is closely monitoring these developments and more, as it seeks growth both organically and through strategic acquisitions.

“We’re exploring opportunities in sports betting, next-gen video, and looking to expand our footprint in Europe and Asia,” Peled mentioned.

With its recent licensing deal to publish under Sports Illustrated, Minute Media plans to build on the iconic sports brand and expand the magazine’s publishing operations globally. Minute Media will continue Sports Illustrated’s tradition of in-depth journalism, thereby expanding the company’s digital footprint into print.

There’s speculation about Minute Media potentially going public, given its rapid expansion in recent years. Addressing this, Peled outlined the company’s approach to sustained growth.

“Our main focus is on balancing profitability with significant top-line growth. This keeps us at the forefront of sports tech globally and opens up various strategic options, whether that’s further acquisitions or an IPO. We’re keeping an open mind about our future growth avenues.”

Israel’s Entrepreneurial Ecosystem

Peled closed by highlighting the importance of Minute Media’s Israeli roots and how the nation’s dynamic ecosystem remains a driving force behind the company, even as it ventures into increasingly global markets.

“Our Israeli roots are really, really key,” Peled shared. “It’s our number one differentiator. You’ll find our offices in New York, LA, São Paulo, Tokyo, London, and more – but our Israeli DNA, and the flexibility and creativity it brings, will always come first.”

Prime Services C-Suite Newsletter – March 2024

Jack-of-all-Reads: A newsletter for multi-hat-wearing C-suite leaders and their key constituents.

Areas of Focus: Regulatory Environment, Marketing, and ODD

Industry Insights:

Our newsletter, Jack-of-all-Reads, shares the latest and greatest insights in a brief read on a monthly basis. Please let us know of any comments or questions – we welcome and appreciate your continued partnership.

Industry Insights:

- Top of Mind: Regulatory Line Items. Funds continue to try and keep track of the ever-changing regulatory landscape. We are fielding concerns regarding continued updates from the SEC around the new private funds rule, as well as increased cyber security safeguards being put in place in the US and across the pond.

- Private Funds Rule. The rule has different effective dates for funds managing more than $1.5bn AUM (as of Sept 2024) and for those managing less than $1.5bn AUM (as of March 2025). Advice to managers is to start working with counsel to adapt their policies and procedures as soon as possible given there is a long road to compliance. Annual disclosures will have to be made to all investors in the same private fund. Although the SEC has not defined the methods of disclosure, we are seeing an increase in the importance of data room capabilities to centralize important documents.

- Cyber Security. Regarding the SEC’s cyber security rule, managers will have a timeline to file within 48 hours and report any accidents within 72 hours. Although the rule was put into effect for many managers in December of 2023, smaller reporting companies will have until June 2024, at the latest, to comply.

- Cyber In the EU. Managers are working to comply with the EU’s Digital Operational Resilience Act (DORA). DORA entered into force in January 2023 and the terms will apply as of January 2025. March 2024 was the EU’s deadline for public consultation on the policy products aimed to standardize the regulation’s requirements. As it stands, DORA requires AIFMs and ManCo’s to classify or report all IT and cyber security related incidents and contract an external firm to conduct comprehensive resilience testing on their IT and cyber security systems. DORA also requires these financial entities to manage their Information and Communications Technology (ICT) service provider risk, with the provisions placing an emphasis on contractual relationships. AIFMs are encouraged to compile a register of their existing ICT service provider contracts to ensure compliance with DORA.

- Marketing Focus: An Era of Digital Transformation in Marketing & Regulatory Updates. Some groups are starting to explore creative new ways to market and improve workflows. On top of that, the evolution of the regulatory environment has many focused on continued guidance towards the new marketing rule and staying compliant.

- AI & Data Analysis Technologies in Marketing. The team has been fielding questions from managers who are searching for ways to integrate AI tools to enhance, refine, and speed up their marketing efforts. While AI tools cannot replace the human creativity and connection involved in a fund’s marketing process, they can be used in the beginning stages as a starting point for drafting materials, and they can also speed up research processes by succinctly aggregating information. In addition, many marketers are also focused on using other data analysis technologies to gain better insights into their target audience’s needs. A new study published by EXT. Marketing found that almost half of marketer’s plan to focus on implementing new data analysis technology in their processes this year. Video-based marketing is also gaining in popularity, with the EXT. Marketing report finding that people have a preference towards visual aids, including easy to digest scannable content and short videos that can be consumed quickly.

- Additional Guidance: New Marketing Rule Updates. Last month, the SEC released updates to the new marketing rule, which gave managers additional guidance on requirements for calculating net and gross performance. Managers are encouraged to reach out to their legal counsel with any questions to ensure they will be in compliance . Although the law itself has not changed, there was an increase in requests on methodology for performance calculations prior to this FAQ.

- Trends in ODD. Throughout conversations with various ODD teams on their current areas of focus across the industry, many have emphasized challenges around talent retention and acquisition, the increased importance of having efficient IT systems, and the need to more closely scrutinize vendor relationships.

- Talent. As the biggest funds continue to grow in size, the war for talent across both the investment and non-investment teams continues. This has been forcing managers to think differently about how they aim to retain and attract key workers. Many funds are reporting particular difficulty in hiring for junior controller roles and, similarly, many accounting firms are having trouble retaining junior accountants. To cope, some groups are heavily investing in technologies that can help solve for this industry-wide shortage.

- Technology. ODD teams are placing emphasis on how their managers are utilizing technology and are seeing more clients engage with software data analysis programs. The days of having all analysis on excel seems to be diminishing.

- Vendor Due Diligence. Ensuring new vendors go through rigorous compliance is a focus, specifically as it pertains to expert networks and alternative data sources. With potential risks arising from managers’ use of AI technologies and the longstanding risks associated with utilizing third-party vendors, it is increasingly important that funds vet their technology systems and put safeguards and policies in place to respond compliantly to any breaches. There is also concern around Expert Networks and heightened diligence on transcripts received from expert networks to ensure there is not MNPI embedded.

Please reach out to your Jefferies contact for more information on any of the topics above.

Client Corner:

Women’s History Month: Numbers in Alternatives: The industry has seen an increased focus around DEI initiatives and many have been reflecting on the pivotal role diversity plays in the alternatives space. Preqin released a report this month on the status of female representation in the industry, finding that only 17% of those in senior roles at hedge funds are women. Although this is 6% higher than the proportion in 2020 and is higher than the rate across the entire alternatives industry, which sits at 15%, there are still discrepancies when compared to the broader workforce. Preqin’s report found that the proportion of female employees across all levels – junior, middle, and senior – appears lower in the alternatives industry overall. As Women’s History Month comes to an end, it is important to continue to create a workplace culture that allows for diversity of thought and ideologies.

Spotlight on Content and Events:

Launch 2025. This series of video, audio, and written content explores critical questions that should be top of mind for alternative fund founders and some answers that can help build a successful launch. It includes six episodes that explore the critical questions that need to be top of mind for every alternative fund founder in the mid-2020s and some answers that can help build a more successful launch such as: “Who do you hire first?” and “What is this going to cost you?”. VIEW HERE

AI FAQ’s: As the industry makes strides in understanding how AI tools may be able to work for them we are fielding questions from managers and investors. This piece answers some of the most frequently asked questions around AI. It also discusses recent trends and themes across the hedge fund industry regarding AI and its use cases. Reach out to the Jefferies consulting team to discuss the below:

- What is AI?

- How are manager using AI?

- How are investors thinking about AI?

- What compliance considerations should AI users keep in mind?

Interesting Service Provider Reads: Highlighting Topical Content from Industry Leaders

EisnerAmper – A Comprehensive Outlook on Hedge Funds in 2024

EXT. Marketing – Top Trends in Financial Marketing in 2024

Schulte Roth & Zabel – Marketing Rule FAQ – Impact of Subscription Lines of Credit on Presentation of Net IRRs

Sidley – Enforcement is on the Rise Against Non-Compete Agreements. Is Your Business Ready?

SS&C – Preparing for Form PF Changes as SEC & CFTC Adopt Amendments

Jefferies Prime Services Contacts:

Mark Aldoroty

Head of Jefferies Prime Services

[email protected]

Barsam Lakani

Head of Sales for Prime Services

[email protected]

Ariel Deljanin

Business Consulting Services

[email protected]

Leor Shapiro

Head of Capital Intelligence

[email protected]

Paul Covello

Global Head of Outsourced Trading

[email protected]

Eileen Cooney

Capital Introductions

[email protected]

DISCLAIMER

THIS MESSAGE CONTAINS INSUFFICIENT INFORMATION TO MAKE AN INVESTMENT DECISION.

This is not a product of Jefferies’ Research Department, and it should not be regarded as research or a research report. This material is a product of Jefferies Equity Sales and Trading department. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the individual author and may differ from the views and opinions expressed by the Firm’s Research Department or other departments or divisions of the Firm and its affiliates. Jefferies may trade or make markets for its own account on a principal basis in the securities referenced in this communication. Jefferies may engage in securities transactions that are inconsistent with this communication and may have long or short positions in such securities.

The information and any opinions contained herein are as of the date of this material and the Firm does not undertake any obligation to update them. All market prices, data and other information are not warranted as to the completeness or accuracy and are subject to change without notice. In preparing this material, the Firm has relied on information provided by third parties and has not independently verified such information. Past performance is not indicative of future results, and no representation or warranty, express or implied, is made regarding future performance. The Firm is not a registered investment adviser and is not providing investment advice through this material. This material does not take into account individual client circumstances, objectives, or needs and is not intended as a recommendation to particular clients. Securities, financial instruments, products or strategies mentioned in this material may not be suitable for all investors. Jefferies is not acting as a representative, agent, promoter, marketer, endorser, underwriter or placement agent for any investment adviser or offering discussed in this material. Jefferies does not in any way endorse, approve, support or recommend any investment discussed or presented in this material and through these materials is not acting as an agent, promoter, marketer, solicitor or underwriter for any such product or investment. Jefferies does not provide tax advice. As such, any information contained in Equity Sales and Trading department communications relating to tax matters were neither written nor intended by Jefferies to be used for tax reporting purposes. Recipients should seek tax advice based on their particular circumstances from an independent tax advisor. In reaching a determination as to the appropriateness of any proposed transaction or strategy, clients should undertake a thorough independent review of the legal, regulatory, credit, accounting and economic consequences of such transaction in relation to their particular circumstances and make their own independent decisions.

© 2024 Jefferies LLC

Clients First-Always SM Jefferies.com

A View of ESG Performance During the Trump and Biden Presidencies

On November 5, 2024, millions of Americans will head to the ballots, where the presidency, 468 congressional seats (33 in the Senate and all 435 in the House), and 11 governorships will be contested. These outcomes may shape the future of the energy transition, with climate policies front of mind for voters and candidates alike.

Last month, Jefferies’ Sustainability and Transition team explored six key questions around the 2024 elections’ impact on the US energy landscape. This analysis was part of a broader series examining the interplay between politics and the global energy transition.

Continuing this series, the team’s latest report analyzes ESG performance during the presidencies of Donald Trump (R) and Joe Biden (D). Specifically, it explores how ESG heuristics performed against traditional counterparts and broader market benchmarks during each administration.

This analysis covers two distinct periods: (1) from President Donald Trump’s election to President Joe Biden’s election and (2) from President Biden’s election to the present. It’s important to note that these findings do not establish causality, as ESG performance is influenced by a multitude of factors beyond just politics and policy.

Jefferies analyzed seven heuristics focused on ESG and the energy transition:

- Four ESG and energy transition indices outperformed their broad market benchmark during President Trump’s tenure, while three underperformed.

- All seven ESG and energy transition indices underperformed vs their broad market index during the current Biden era.

—

Invesco WilderHill Clean Energy ETF (PBW) vs. Invesco S&P 500 Equal Weight Energy ETF (RSPG) vs. S&P 500 (SP50)

- PBW tracks a modified equal-weighted index of US-listed companies involved in clean energy sources or energy conservation.

- RSPG tracks an equal-weighted index of US energy companies listed in the S&P 500.

- SP50 includes 500 leading companies in leading industries of the US economy.

Findings: During the Trump Administration, PBW saw the strongest performance and RSPG saw the weakest, with a delta in total return of 350.5 percent. During the Biden Administration, performance flipped: RSPG performed strongest and PBW weakest in a reversal of 309.8 percent.

iShares STOXX Europe 600 Oil & Gas UCITS ETF (SXEPEX) vs. SPDR S&P Oil & Gas Exploration & Production ETF (XOP) vs. STOXX Europe 600 (183660)

- SXEPEX tracks the performance of companies from the European oil and gas sector.

- XOP tracks an equal-weighted index of companies in the US oil and gas exploration and production space.

- 183660 includes 600 European companies representing all market caps.

Findings: During the Trump Administration, STOXX Europe 600 saw the strongest performance and XOP the weakest, with a delta in total return of 81.7 percent. Again, during the Biden Administration, performance flipped: XOP performed strongest and STOXX Europe 600 weakest in a reversal of 208.9 percent.

iShares MSCI ACWI Low Carbon Target ETF (CRBN) vs. iShares MSCI World ETF (URTH) vs. MSCI AC World (892400)

- CRBN tracks an index of stocks from global firms selected for a bias toward lower carbon emissions.

- URTH tracks a market-cap-weighted index of stocks that cover 85 percent of the developed world’s market cap.

- 892400 captures large- and mid-cap companies across developed markets.

Findings: During the Trump Administration, performance was essentially the same across all indices. Under the Biden Administration, URTH has seen the strongest performance and CRBN the weakest, with a delta of 8.3 percent.

MSCI Global Alternative Energy (MS700750) vs. iShares Global Energy ETF (IXC) vs. MSCI AC World (892400)

- MS700750 includes developed and emerging market companies that derive 50 percent or more of their revenues from alternative energy products and services.

- IXC tracks a market cap-weighted index of global energy companies.

- 892400 captures large- and mid-cap companies across developed markets.

Findings: During the Trump Administration, alternative energy saw the strongest performance and IXC the weakest, with a delta in total return of 146.2 percent. Under the Biden Administration, performance flipped: IXC saw the strongest performance and alternative energy the weakest, with a delta of 202.6 percent.

Invesco Solar ETF (TAN) vs. iShares Global Energy ETF (IXC) vs. MSCI AC World (892400)

- TAN tracks an index of global solar energy companies selected based on the revenue generated from solar-related businesses.

- IXC tracks a market cap-weighted index of global energy companies.

- 892400 captures large- and mid-cap companies across developed markets.

Findings: During the Trump Administration, TAN saw the strongest performance and IXC the weakest, with a delta of 337.5 percent. During the Biden Administration, IXC saw the strongest performance and TAN the weakest, with a delta of 207.2 percent.

SPDR MSCI USA Gender Diversity ETF (SHE) vs. S&P 500 (SP50) vs. MSCI USA (984000)

- SHE tracks a market cap-weighted index of US companies promoting gender diversity while exhibiting a high proportion of women across all levels of their organization.

- SP50 includes 500 leading companies in leading industries of the US economy.

- 984000 measures the performance of the large- and mid-cap segments of the US market.

Findings: MSCI USA saw the strongest performance under the Trump Administration and SHE the weakest, with a delta of 21.3 percent. During the Biden Administration, the S&P 500 saw the strongest performance and SHE the weakest by 19.7 percent.

iShares MSCI USA ESG Select ETF (SUSA) vs. S&P 500 (SP50) vs. MSCI USA (984000)

- SUSA tracks an index of US companies with high ESG factor scores, as calculated by MSCI.

- SP50 includes 500 leading companies in leading industries of the US economy.

- 984000 measures the performance of the large- and mid-cap segments of the US market.

Findings: During the Trump Administration, SUSA saw the strongest performance and S&P 500 the weakest, with a delta in total return of 6.7 percent. Under Biden, performance flipped: the S&P 500 saw the strongest performance and SUSA the weakest, with a delta of 9.1 percent.

—

Again, these findings do not establish causality, as the factors impacting ESG performance during any given period are multifarious. That said, today’s political parties diverge significantly in their approach to the energy transition and related policies. With so many elections slated for this November, there is no question that 2024 will be a critical year for ESG.

For the full report, and more coverage of ESG performance, follow Jefferies’ Sustainability and Transition team.

The Climate Tech Investment Landscape — A Deep Dive

With over 7,000 companies – of which 100 are valued at over $1 billion – climate tech has emerged as a pillar of ESG and sustainability investing. As the energy transition unfolds, these technologies are only poised to capture more market share.

The novelty of many climate tech solutions makes it difficult for investors to assess their progress, market penetration, and impact on existing players – especially since most operate in private markets.

Jefferies’ Sustainability & Transition team set out to examine the landscape of climate tech investing; analyzing its current state, trajectory over the next year; key developments and innovations; and more.

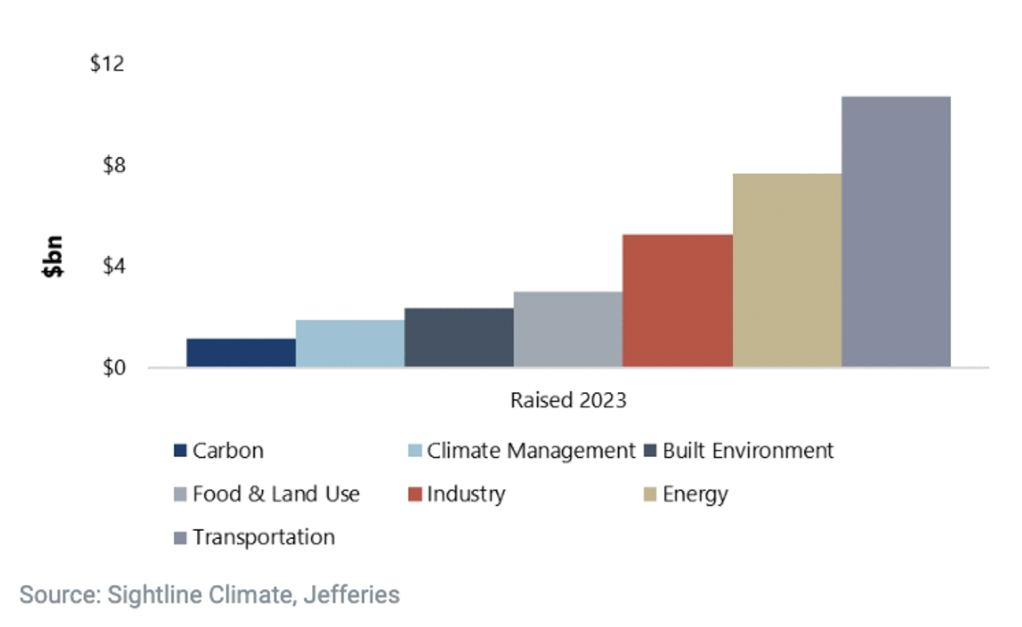

First, it’s crucial to understand the evolution of climate tech since 2020. This period marked a significant leap forward for the sector, with over 2,500 companies raising around $150 billion through more than 4,000 deals. Acquisitions have been the primary exit strategy, accounting for 65 percent of exits since 2020. Despite macro challenges, the sector maintained its momentum in 2023, with the average deal size growing by 28 percent and investments increasing at an annual rate of 23 percent.

In 2024, as macro conditions improve, climate tech investors have dry powder. Once the domain of VC funds, the sector’s cap table now includes private equity, governments, corporates, and infrastructure funds, all ready to invest substantial capital.

Here are some of the key questions for climate investors in 2024.

What’s in store for the sector’s investment landscape?

Corporate involvement in the climate tech space is expected to grow in 2024. Established corporates are likely to integrate innovative companies with limited capabilities and balance sheets, aiming to expand their market share or adjust their existing business lines.

The sector is set to mature even further, continuing the trend from 2023, with the bulk of funding flowing towards established players that offer proven solutions in specific sectors. Data indicate that Energy and Industry will be the main areas of focus for investors in 2024.

What are the size and scale of key players in the climate tech ecosystem?

Climate tech has undergone significant evolution in recent years, shifting from primarily funding innovative and immature technologies to also embracing infrastructure, growth, and bankable projects. Several factors need to be considered as investors evaluate the sector’s key opportunities in 2024:

Funding Levels: Where is capital flowing?

- In 2023, late-stage and growth funding experienced continued declines (around 30 percent), whereas seed-stage funding showed resilience, increasing by 12 percent year over year.

- The transportation and energy verticals remained highly attractive to investors.

- Industry was the only subsector to gain positive momentum amid a challenging macroeconomic environment.

Transportation and Energy remained in favor in 2023.

IPOs, SPACs, Acquisitions: What’s the state of dealmaking?

- Overall, IPOs, SPACs, and M&A transactions decreased by 50 percent in 2023. SPACs, in particular, saw an 89 percent downturn, signaling a potential collapse in that market for climate tech companies.

- Transportation and Energy saw the largest number of companies go public or get acquired, representing 64 percent of the sector’s total exits in 2023.

- More than 80 percent of M&A deals in the climate tech space were for undisclosed amounts.

- On average, the median exit time for companies is just north of 8 years.

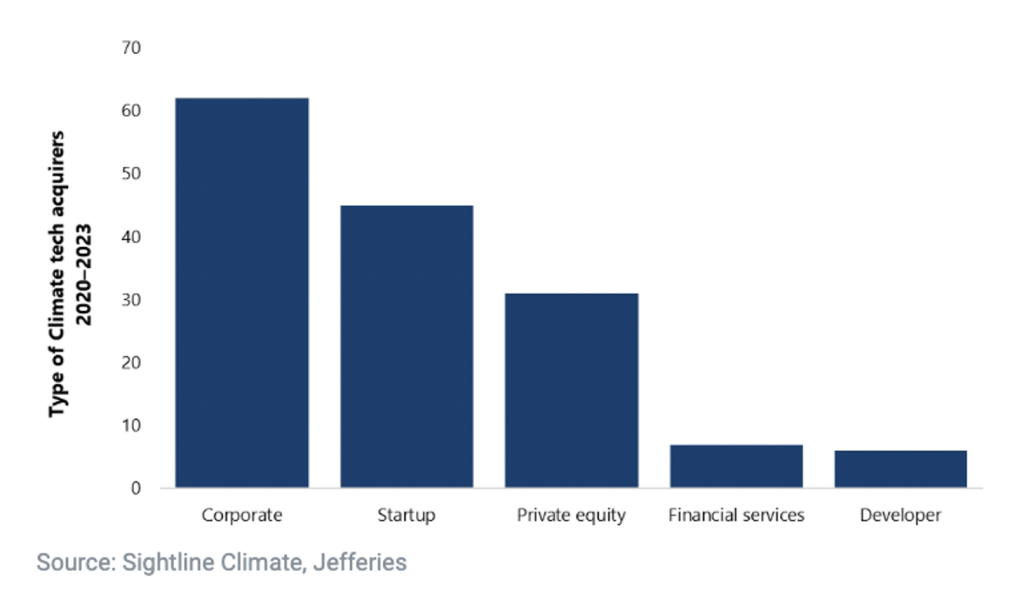

Corporates & Climate Tech: How has their role evolved?

- Since 2020, corporates have emerged as the most active acquirers of companies, responsible for 41 percent of all acquisitions.

- Notably, BP, Shell, and Schneider Electric have been particularly significant players.

- Corporate venture capital has been distributed relatively evenly across Series A and growth-stage funding rounds.

Corporates have been the most active acquirers of climate tech companies over the last 3 years.

How can investors identify winners and losers in emerging climate tech sectors?

Identifying potential success stories in climate tech involves considering returns relative to the level of risk, a familiar approach for investors. Three key risks need to be assessed:

- Technology Risk: Assessing technology risk is often the single biggest issue investors face. Technology risk exists at each step through from concept to early and late prototypes, all the way to first-of-a-kind and commercial operation stages. Earlier-stage innovations naturally command higher risk premiums.

- Execution or Project Risk: With a database of over 16,000 projects globally, Bent Flyvbjerg estimates that over 90 percent of projects (construction) aren’t completed on time, overrunning by an average of 60 percent. Assessing execution risk for first-of-a-kind and one-of-a-kind projects will be a key determinant of success at both the sector level and the company level.

- Geographic Risk: The success of specific solutions will greatly depend on the local context. Some innovations may be more applicable or relevant in certain geographies than in others.

It is now widely accepted that the energy transition is a technological revolution which will play out over the next two decades — and potentially longer. It will harness the power of many new technologies, many of which are not the incumbent options in their respective sectors.

Adoption of new technologies will be both uncertain and nonlinear. Investors who are able to develop an understanding of how innovations play out at various stages will be able to develop strategies to capitalize on new markets.

For a more detailed analysis of the state of climate tech in 2024, see Jefferies’ Sustainability and Transition team’s full report on the state of the market.

Leucadia Asset Management Announces Strategic Relationship with GREYKITE

Cato Networks’ Head of Strategy on Product Differentiation and the IPO Roadmap

In September 2023, Jefferies hosted its seventh annual Tech Trek, Israel’s largest institutional investor conference. The three-day event connects leading global investors with the Israeli tech ecosystem through a series of panels, presentations, and meetings.

At the conference, Jefferies spoke with Yishay Yovel, Chief Strategy Officer at Cato Networks. Cato, an Israeli-based SASE platform company with converged networking, security, and mobility capabilities, is one of the tech ecosystem’s most anticipated IPOs. In September 2023, Cato announced a $238 million equity investment, valuing the company at over $3 billion.

Yovel shared insights on Cato’s strategy for building a differentiated product in an already developed sector; Cato’s “rip-and-replace” approach; achieving resilience in turbulent markets; and the company’s path to going public.

Note: The following interview preceded the events of October 7th and does not take into account the effects of the ongoing conflict.

Achieving Growth in Mature Markets: Cato’s Strategy

Founded in 2015, Cato Networks reached $100 million in annual recurring revenue (ARR) in 2022, growing its ARR from $1 million to $100 million in just five years. Serial entrepreneur Shlomo Kramer, founder and CEO of Cato, previously led cybersecurity startups Check Point and Imperva to multi-billion-dollar IPOs. Cato’s cloud-native architecture combines enterprise networking and network security within a secure access service edge (SASE) framework. Today, more than 2,100 enterprises across 150 countries have adopted the Cato SASE Cloud.

Yovel spoke to the company’s unprecedented growth in the network security sector, which, at the time of Cato’s founding, was already dense with cloud solutions from major providers.

“Most companies grow by building a point solution for a point problem. Our approach was different,” Yovel explained. “Enterprises have a difficult time managing multiple products with separate capabilities. We took a step back and asked, ‘Why is there so much complexity in networking and security infrastructure, and can we simplify it with a single-product architecture?’”

That became the vision for Cato: a turnkey networking and security infrastructure that is scalable and addresses multiple needs.

This “rip-and-replace” strategy became the backbone of Cato’s growth. It involves not just substituting one legacy solution with a cloud alternative, but migrating multiple point products, appliances and cloud services, into a single, cloud-native software stack. Cato’s framework has gained significant traction in the industry, with leaders like Gartner and Forrester now recommending a SASE solution for their network security clients.

Developing Durable Products in Uncertain Markets

Cato’s growth overlapped a challenging period for global markets; in the wake of the COVID-19 pandemic, cost reduction became a priority for many businesses. Though enterprise security is typically viewed as a resilient operating expense, cost centers like the SASE Cloud remained vulnerable to budget cuts. Yovel, addressing this challenge, explained Cato’s approach to building resilient products by prioritizing total cost of ownership (TCO) from the start.

Yovel detailed Cato’s unique sales approach, sharing that “Cato’s projects are essentially funded by existing budgets. We approach companies with separate allocations for firewalls, remote access, and networking infrastructure, and we demonstrate how these budgets can be consolidated into Cato’s solution. Even in challenging economic times, our value proposition is resilient, because we help businesses invest less and get more.”

The Path to Going Public: What’s Next for Cato?

Discussing Cato’s future, Yovel addressed the question on many investors’ minds: when is the company planning to go public?

Shlomo Kramer is on track to be the first founder to lead three cybersecurity companies from seed stage to multi-billion-dollar IPOs. He has discussed a potential IPO in the fourth quarter of 2024, depending on market conditions.

“We want to go public, if market conditions allow it, in the next 12 to 18 months,” Yovel stated. “We have the growth rate and numbers to support this. We just need to find the right opportunity in public markets.”

While predicting the exact timing and specifics of a potential IPO is difficult, the company’s trajectory, product resilience, and focus on growth position it for longtime leadership in network security.

Shifting Tides in the Sleep Apnea Treatment Market: From Philips’ Re-Entry to Ozempic

The sleep apnea treatment landscape experienced a major reshuffling in 2021, as Philips Respironics, a longtime market leader, recalled several CPAP and BiPAP devices due to potential health risks. Now, three years later, Philips is preparing to re-enter the market. What does this mean for companies like ResMed, who stepped in to fill the gap Philips left behind?

This is just the tip of the iceberg in what’s expected to be a critical year for the sleep apnea sector. The advent of GLP-1 drugs brings further uncertainty. These novel treatments have the potential to alleviate sleep apnea symptoms, but their impact on the market is yet to be seen.

In a recent survey of 50 US-based sleep doctors and durable medical equipment (DME) providers, Jefferies’ Global Research and Strategy Team explored these developments and more. Respondents shed light on the current and future market for sleep therapies, from the resilience of established methods like CPAP (Continuous Positive Airway Pressure) to the emerging potential of GLP-1 Agonists.

Here, we unpack the latest trends in pricing, product quality, and novel therapeutic approaches that are shaping an eventful 2024 for the sleep apnea treatment market.

The Competitive Landscape: How Will Philips’ Re-Entry Impact the SDB Treatment Market?

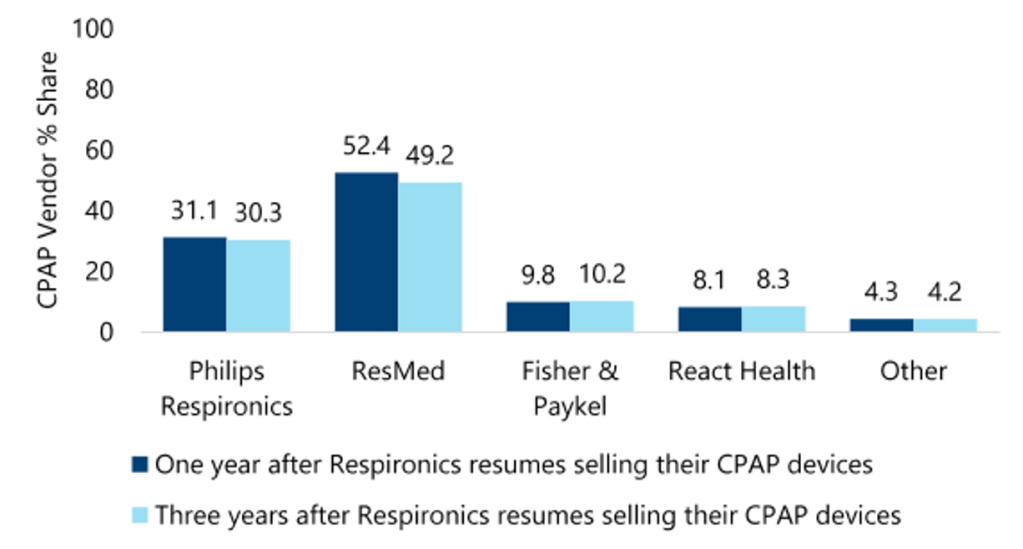

ResMed, the market leader, scored highest in providers’ CPAP and mask rankings. RMD currently holds 62 percent market share, a position strengthened by Philips Respironics’ exit from the market in 2021. This shift came after issues were discovered in Philips’ CPAP and BiPAP devices, leading to a market gap that RMD effectively filled. Despite its strong position, respondents expect RMD’s market share to decrease with Philips’ re-entry, potentially falling to between 49 and 52 percent in the next 1-3 years.

Exhibit 1 – What percentage of your CPAPS do you expect to write scripts for or recommend patients use from the following providers?

Source: Jefferies 4Q23 Sleep Survey

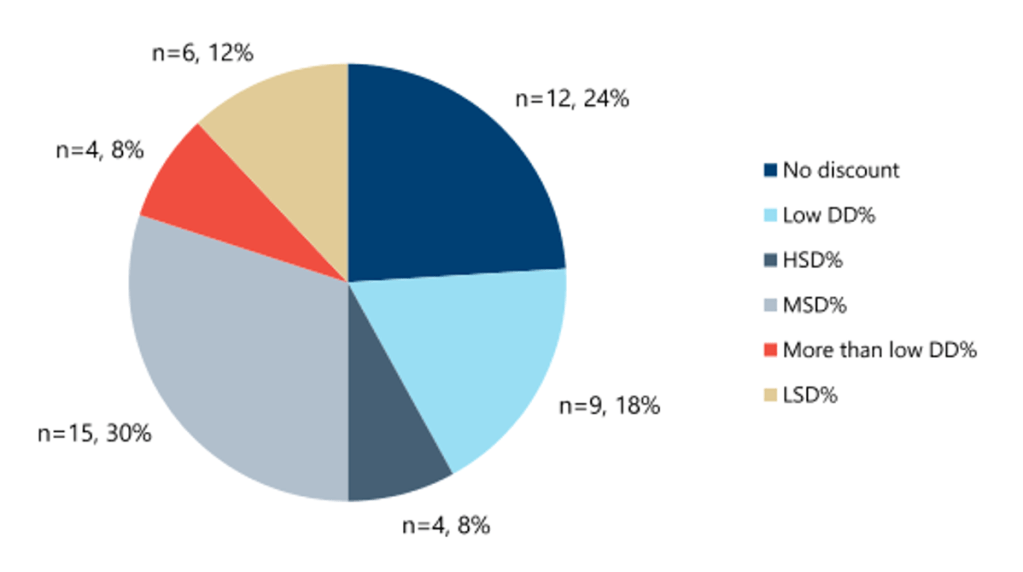

The exact timing of Philips’ return to market is still pending, dependent on the outcome of a consent decree. However, respondents expect PHIA’s re-entry to include competitive pricing strategies, with moderate discounts aimed at RMD. While PHIA is expected to regain market share, the process is likely to be gradual, buffeted by the company’s reputational challenges and an increasingly tough competitive landscape.

Exhibit 2 – Assuming Respironics can prove the safety of their machines, what level of pricing discount would you insist on from Respironics (expressed as average % discount vs ResMed)?

Source: Jefferies 4Q23 Sleep Survey

Looking ahead, respondents also expect scripts for Fisher & Paykel and React Health to increase in the coming years, by 4.1 and 3.0 percent, respectively. Both companies benefited from the initial PHIA recall, with their market share rising by several percentage points.

The Birth of GLP-1s: Do Weight-Loss Therapies Threaten the Industry’s Gold Standard?

Though respondents expect continued growth in the CPAP market, this growth faces potential slowing due to the rise of GLP-1 treatments. GLP-1 Agonists, primarily used for obesity management and diabetes, show promise in reducing sleep apnea symptoms by promoting weight loss, a known factor in improving sleep apnea severity.

Survey participants predict a 12 percent increase in CPAP volume for 2024, with GLP-1 treatments having a limited impact initially. However, over the next five years, they expect the CPAP market could shrink by approximately 15 percent as a result of these treatments. To date, there hasn’t been a noticeable decline in adherence to or sales of traditional sleep apnea treatments among patients using GLP-1 treatments, but changes are expected as the market adjusts to these new therapies. Leading CPAP providers like RMD are yet to feel a significant impact but are preparing for future shifts in the market influenced by these novel therapeutic options.

Jefferies’ Sleep Survey offers important insight into shifts in the sleep apnea treatment landscape, as key players like ResMed and Philips navigate periods of transition. The coming years may see changes in market share, competitive pricing dynamics, and the integration of novel therapies like GLP-1 agonists, presenting unique opportunities and challenges for investors, healthcare providers, and patients. Jefferies Global Research and Strategy team will monitor these developments closely; the full summary of the sleep doctor and DME provider summary is available here.