How Data Centers Are Shaping the Future of Energy Consumption

The following article is an overview of “Powering Data Centers,” a report from Jefferies’ Equity Research Team. For the full report, visit this link.

If it feels like GPUs (Graphics Processing Units) are suddenly everywhere, it’s because they are. GPUs drive computation across a wide range of industries and applications, from big data analytics to machine learning.

Soaring GPU demand is rippling across the global economy, but no area has been more affected than data centers. They house the infrastructure to power, cool, and manage GPUs. Over the past two years, data center demand has skyrocketed, surging to over 30% annual growth in some key markets.

The pressing question is: Can supply keep up? Market constraints — including scarce raw materials, limited land, labor shortages, and construction bottlenecks — pose serious challenges. Most critically, power generation and grid capacity are lagging.

With demand outstripping supply, rents for wholesale data centers have jumped over 80% since late 2021, reversing years of decline. Rising build costs further strain the market.

This explosive growth in data centers, coupled with infrastructure and power constraints, presents both challenges and opportunities for a myriad of sectors, including utilities, energy, capital goods, infrastructure/construction, and more.

A new report led by Jefferies Utilities and Clean Energy team, with input from more than 20 Jefferies analysts around the world, explores the implications of this growth, the economic dynamics, and the strategic moves needed to sustain the sector’s expansion.

This article previews the following areas of the report:

- Data Center Power Consumption

- Renewable Energy and Power Purchase Agreements

- Regional Dynamics and Opportunities

Data Center Power Consumption

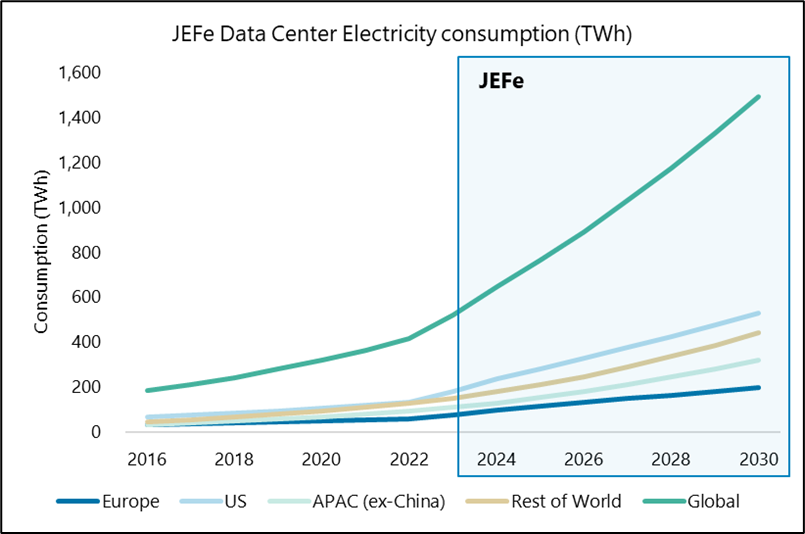

AI Data centers are large, energy intensive operations that often run 24 hours a day. Since 2016, their global power consumption has grown at an estimated 16% compound annual growth rate (CAGR). Jefferies projects this growth will continue through 2030, with US data center electricity consumption outpacing that of Europe and APAC (excluding China).

In the US, many regulated utilities, grid planning organizations, and industry consultants are forecasting resurgent energy demand growth over the decade. This growth could strain power generation and grid capacity. Ten years ago, 15% demand growth in the data center market meant about 250 megawatts. Today, the same growth equates to 2 gigawatts — eight times the demand — and growth was double that in 2022 and ‘23.

In Europe, electricity demand has been flat for two decades, remaining at 2000 levels through 2023. It’s now poised for a rebound, expected to grow at 2-3% annually. Data centers will be a major driver, potentially accounting for 20% of this future growth.

Source: Jefferies Estimates, DC Hawk

Renewable Energy and Power Purchase Agreements

One beneficiary of the data center boom may be the global energy transition.

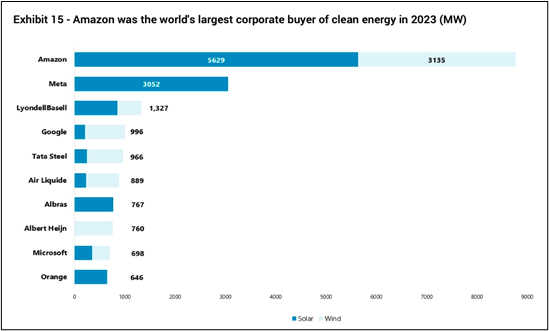

The growth in data centers is expected to help renewable power developers reduce risk by allowing them to form longer-term contracts at higher prices. Big tech companies are now major buyers of Power Purchase Agreements (PPAs) for renewable energy, with contracts spanning 10-15 years at fixed or variable prices. These firm revenue commitments enable developers to finance new renewable energy projects. As data center demand grows, so will these agreements. In 2023, the corporate PPA market hit a record high for the seventh consecutive year, with an increasing share going toward solar, wind, and other renewable sources.

Source: BNEF, Jefferies Analysis

Regional Dynamics and Opportunities

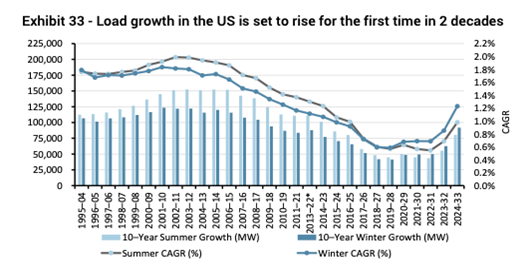

In the United States, resurgent electricity demand from data centers will require additional transmission and generation infrastructure investments in the US. Companies in these spaces are expected to benefit more than those focused on distribution. Independent power producers and nuclear plants will also profit from increased power demand, with nuclear power particularly valued for its stable, carbon-free electricity. Broadly, US utility capital expenditure can be split into three buckets: (1) Grid Hardening, or investments in grid reliability and resistance against adverse weather conditions; (2) Generation, including solar, nuclear, and peaker gas; and (3) Transmission & Distribution, or enhancing and expanding the system around power delivery.

Source: Long-Term Reliability Assessment 2023, FERC, Jefferies

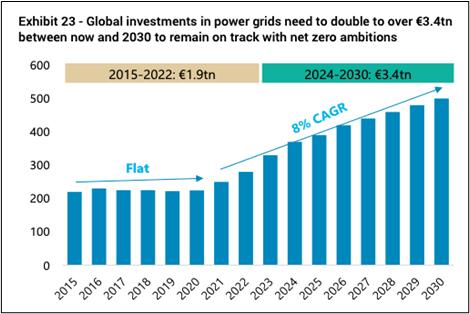

In Europe, the highest data center capacity growth is expected in Germany, Ireland, Spain, Italy, and Norway, with projections exceeding 15% CAGR over the next decade. Norway and Spain, with their cheap baseload power, are attractive markets for incremental data center demand. Germany, Ireland, the Netherlands, and the UK, with their strong financial services, tech companies, and advanced internet and wiring infrastructure, are also prime candidates for this growth. The challenge is the age of European grid infrastructure: 40% of EU grids are over 40 years old. To address these vulnerabilities, European grid companies are significantly increasing their capital expenditure. This increase is driven by new power plant connections, grid resilience improvements, reinforcements, and maintenance. However, developing the necessary infrastructure could take years due to regulatory and permitting processes.

Source: Rystad Energy, Jefferies Cap Goods Team Estimates

In India, the data center market is rapidly expanding, spurred by the Reserve Bank of India’s directives to localize payment data. The country’s data center capacity is projected to grow at over 50% CAGR. This growth necessitates a significant rise in power generation and T&D investments, expected to increase 2.2 times to $280 billion by 2030. This expansion positions India as a major hub for data centers, driving both economic growth and substantial capital expenditure in the sector.

In China, data center power consumption is projected to reach nearly 8% of total power usage by 2030. AI development – particularly generative AI and large language models – are driving rapid growth. Concurrently, China’s grid infrastructure is set to expand significantly. The country is investing in digitalization and distribution to support renewable energy growth.

As the AI era roars on, GPUs and data centers will remain key drivers of global economies. The demand growth brings significant challenges but also vast opportunities. For a more in-depth look at how data center and electricity demand growth will impact global markets, sectors, and governments, read the full report from Jefferies’ Equity Research Team here.

Why Differentiation Is Defining the U.S. Consumer Sector

Consumer spending—and the psychology behind it—is a perpetual puzzle for investors. Before the Jefferies Consumer Conference, we spoke with Jim Walsh, Vice Chairman and Global Head of Consumer, Retail & REGAL Investment Banking, who has over 30 years of experience in the consumer sector. He shared his thoughts on how U.S. consumers are doing and companies’ opportunities and challenges in the current environment.

Q: What is the most important trend in today’s U.S. consumer market?

JW: In the U.S. consumer market, a critical factor that can set a business apart is a truly unique, high-growth, high-volume offering with an attractive value proposition for consumers. If you can effectively communicate this distinctiveness, you will likely attract a diverse range of buyers.

For others, deals will be harder.

Q: A key economic storyline of the last couple of years in the United States has been consumer resilience in the face of inflation. Is that still the case

JW: The consumer probably isn’t feeling as good as you’d think. Marginal consumer spending on luxury items such as restaurants has seen a pullback. Government dollars flowed strongly to the consumer for several years, and now those dollars have been shut off. But where a company has a unique proposition to the consumer—Dutch Bros, Wingstop or Texas Roadhouse, for example—you see a great following across many demographics. For companies with positive traffic within retail and consumer, the valuations are going up dramatically because they’re outpacing the marketplace. So, I would say you have to show consumers something they want to have at a manageable price point. Then they will come in.

Q: If I am a consumer business wanting to fuel my next stage of growth, where should I be looking?

JW: If you are a differentiated consumer business, the public markets are wide open to you now. If you can demonstrate something like 10% unit growth and positive same-store sales primarily driven through traffic, you can definitely get a premium in public markets. Cava’s 2023 IPO, which was one of the most successful of the year, was a great example. These kinds of companies are getting a better premium in public markets because investors can look to the future and have a discounted cash flow analysis that says, “Hey, we could pay for this today, but given these trends, we can look out three or four or five years and see great results.”

If you are a smaller-cap company that is just starting to show significant growth, you might find more willing buyers on the private side, where there is also a fair amount of capital to invest.

Q: If I am the leader of a company that does not meet those desirable growth metrics, what options are available to me to help fund the next stage of my growth?

If you can’t go to public markets and there is a gap in what you can do on the private side, you might want to think about preferred capital. Basically, every private equity program is looking for preferred capital opportunities, even if they don’t focus specifically on the consumer sector. That’s where there is a lot of liquidity.

And then you have a lot of companies that are not firing on all cylinders. Those are the ones that strategics are looking at where they see the ability to cut costs and get scale from synergies and technology. We’re seeing a fair amount of activity in cases like that.

Q: You have been in the consumer banking field for several decades. Aside from technology and the way it is incorporated into everything, what is it that has changed most about the way businesses grow and get capital?

JW: It’s just a far more crowded environment to bring something new and attractive to the consumer. Thirty years ago, there wasn’t as much differentiation available to the consumer, which created a wider opening for an innovator to develop a unique product or business model. That’s harder to do today, and that’s why we haven’t had many companies go public in the last few years. They are just not differentiated enough in the marketplace, and consumers have plenty of options that allow them to be selective in what they shop for or where they go to eat.

Now, there are examples where talented entrepreneurs introduce something totally new, like what Marc Lore has done with the food delivery service Wonder. But, on balance, there is just a higher bar for companies to clear to show that they have an offering that is truly differentiated.

Prime Services C-Suite Newsletter – May 2024

Jack-of-all-Reads: A newsletter for multi-hat-wearing C-suite leaders and their key constituents.

Jumping into Summer Themes – Non Competes, Shadow Trading, T+1, and Operational Due Diligence

Industry Insights:

Our newsletter, Jack-of-all-Reads, shares the latest and greatest insights in a brief read on a monthly basis. Please let us know of any comments or questions – we welcome and appreciate your continued partnership.

Industry Insights:

- FTC’s Non-Compete Ruling. On April 23rd, the Federal Trade Commission (FTC) announced a rule banning non-competes nationwide with an effective date of August 22, 2024. The rule retroactively voids virtually all existing non-compete clauses in employment agreements, with few exceptions. Additionally, it will ban any new non-competes, regardless of the employee’s salary or status, moving forward. While legal challenges regarding this ruling occur between the FTC and various business groups, managers can still take steps to prepare:

- What should fund managers do? The ruling requires employers to provide “clear and conspicuous notice” to their employees impacted. This notice must be received by the effective date.

- Work with counsel to figure out which employees are affected, which are exempt, and how they are going to provide the proper notices required by the ruling.

- Implement alternative protection methods in their employee contracts that do not violate the FTC’s ban.

- What should fund managers do? The ruling requires employers to provide “clear and conspicuous notice” to their employees impacted. This notice must be received by the effective date.

- T+1: Understanding the Expected. The SECs acceleration of the settlement cycle from T+2 to T+1 had an effective date of May 28th in the US and May 27th in Canada, Mexico, and Peru. This rule will enforce completion of allocations, affirmations, and confirmations of trades sent or received within one day of the trade. Service providers have been adjusting their processes to be compliant with the new timeline.

- What is Changing? Most prime brokers are set to begin sending notifications to clients to inform them that the trade will need to be allocated and confirmed within the allotted time frame. The cut off for afterhours trading will be at 8pm EST on the day of the trade. Managers are ensuring there are systems in place to manage this and decrease the likelihood of mishaps.

- Being Prepared. Managers should be checking in with their OMS providers and fund admins to ensure all systems are in place and sent to their counterparties on time. Some groups are utilizing vendors such as NYFIX or CTM to assist in these processes. If unaware, reach out to your counterparties for list of action items including steps such as:

- Make arrangements with your counterparties, prime brokers, and custodians to affirm transactions on trade date.

- Explore electronic industry trade processing solutions.

- Update FX liquidity, trading, and settlement arrangements.

- ODD: Ins and Outs of Current Practices. As we enter new stages of technology and investing, ODD teams are navigating new processes. Through our conversations with ODD professionals as well as the SBAI’s 2024 Operational Due Diligence Survey there are various ways in which the function has evolved.

- New Assets. As investment teams look to diversify, ODD professionals are working on understanding new asset classes. They’re assessing different types of managers and funds for the first time and having to learn unfamiliar parts of the industry.

- More Technology. Firms without robust dedicated teams in house are more likely to rely on data tools as well as be early adopters of software and technology. As the majority of ODD professionals feel that they do not have enough time to perform tasks, the movement towards AI is expected to have great implications towards these groups.

- Counterparties. As managers continue to outsource back office functions, it can provide additional hurdles for those performing ODD to get quality information and full transparency.

- Onsite. According to the SABI survey, the majority of ODD reviews are still done onsite. Most allocators are performing a full ODD review with new manager relationships, however, a small group are taking a risk based approach.

- Insider Trading: Shadow Trading Ruling. The SEC won their first shadow trading case on April 5th after an 8 day long trial. Shadow trading is defined as occurring when an investor invests in one company after hearing material nonpublic information about another company which can affect the performance of the related companies stock.

- Implications for Managers. The ruling confirmed that this type of trading is a considered an insider trading activity encompassed under an expansion of the existing insider trading rules. Given concerns, there is additional focus on having proper compliance controls and technologies in place.

- How to Stay Protected. Many groups are specifically looking into technology to monitor expert network calls and some are even revamping their compliance policies.

Please reach out to your Jefferies contact for more information on any of the topics above.

Client Corner:

Increased Software Interest: Analytics and Data. We’ve recently observed an uptick in clients asking about various software and technological solutions to supplement key aspects of the reporting and data aggregation process. As the technological revolution continues, many are looking for ways to stay ahead, and do more with less resources. There has been an increase in emerging managers leveraging these tools as well. Our team has been doing research around the key players in the space, feel free to reach out to Ariel Deljanin to discuss further.

Spotlight on Content and Events:

Pitching 101: Reviewing Industry Best Practices.

As managers focus their attention on the capital raising process, they must begin to evaluate how they want to present and pitch themselves as well as their business. This piece describes the common outlines, frequently asked questions from inventors, and the do’s and don’ts of presenting.

Contact your Jefferies representative to learn more.

From the Desk of BCS: 2024 H1 Insights. Although many themes from the 2023 Trends Pack are continuing to impact decision makers today, the Jefferies Capital Intelligence team is compiling insights around current key trends impacting the hedge fund industry. Through engaging with clients, the ODD community, and attending conferences, this piece has a focus on combining long-term industry data with current insights to identify emerging trends. Some top of mind topics include managing counterparty and LP relationships, the war on talent, regulatory environment, and capital raising. Stay tuned for the H1 2024 iteration of From the Desk of BCS.

Interesting Service Provider Reads: Highlighting Topical Content from Industry Leaders

Akin Gump – SEC Announces First Off-Channel Communications Enforcement Action Against a Standalone Private Fund Manager and “Round 2” of Marketing Rule Enforcement Actions — Focus on Hypothetical Performance

Lowenstein – ‘Shadow Trading’ is Insider Trading: Jury Establishes Liability in Historic Shadow Trading Case

RQC Group – SEC Issues Risk Alert Providing Initial Observations Regarding Marketing Rule Compliance

Seward & Kissel –2023 New Manager Hedge Fund Study

Jefferies Prime Services Contacts:

Mark Aldoroty

Head of Jefferies Prime Services

[email protected]

Barsam Lakani

Head of Sales for Prime Services

[email protected]

Ariel Deljanin

Business Consulting Services

[email protected]

Leor Shapiro

Head of Capital Intelligence

[email protected]

Paul Covello

Global Head of Outsourced Trading

[email protected]

Eileen Cooney

Capital Introductions

[email protected]

DISCLAIMER

THIS MESSAGE CONTAINS INSUFFICIENT INFORMATION TO MAKE AN INVESTMENT DECISION.

This is not a product of Jefferies’ Research Department, and it should not be regarded as research or a research report. This material is a product of Jefferies Equity Sales and Trading department. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the individual author and may differ from the views and opinions expressed by the Firm’s Research Department or other departments or divisions of the Firm and its affiliates. Jefferies may trade or make markets for its own account on a principal basis in the securities referenced in this communication. Jefferies may engage in securities transactions that are inconsistent with this communication and may have long or short positions in such securities.

The information and any opinions contained herein are as of the date of this material and the Firm does not undertake any obligation to update them. All market prices, data and other information are not warranted as to the completeness or accuracy and are subject to change without notice. In preparing this material, the Firm has relied on information provided by third parties and has not independently verified such information. Past performance is not indicative of future results, and no representation or warranty, express or implied, is made regarding future performance. The Firm is not a registered investment adviser and is not providing investment advice through this material. This material does not take into account individual client circumstances, objectives, or needs and is not intended as a recommendation to particular clients. Securities, financial instruments, products or strategies mentioned in this material may not be suitable for all investors. Jefferies is not acting as a representative, agent, promoter, marketer, endorser, underwriter or placement agent for any investment adviser or offering discussed in this material. Jefferies does not in any way endorse, approve, support or recommend any investment discussed or presented in this material and through these materials is not acting as an agent, promoter, marketer, solicitor or underwriter for any such product or investment. Jefferies does not provide tax advice. As such, any information contained in Equity Sales and Trading department communications relating to tax matters were neither written nor intended by Jefferies to be used for tax reporting purposes. Recipients should seek tax advice based on their particular circumstances from an independent tax advisor. In reaching a determination as to the appropriateness of any proposed transaction or strategy, clients should undertake a thorough independent review of the legal, regulatory, credit, accounting and economic consequences of such transaction in relation to their particular circumstances and make their own independent decisions.

© 2024 Jefferies LLC

Clients First-Always SM Jefferies.com

The Return of the Strategic Buyer in Tech M&A

Technology capital markets have been in a transaction winter since the end of 2021, with many buyers and sellers frozen in place and substantially reduced transaction volume. That deep freeze appears to be ending and the field of prospective buyers is expanding.

For the first time in several years, private equity firms and other financial players may not be the lead protagonists in technology M&A. Strategic buyers have reawakened, which creates expanded opportunities for sellers to achieve optimized value, particularly if they prepare thoroughly and target the market correctly.

The relative quiet of strategic acquirors has been much discussed, particularly since their cash balances have grown steadily since the end of the Global Financial Crisis. Higher interest rates also gave strategic acquirors a pronounced cost of capital advantage relative to other types of buyers. At the same time, valuation multiples declined for many otherwise healthy and attractive technology companies.

This should have led to an uptick in strategic acquiror activity as they looked to deepen and extend capabilities and capitalize on high-value strategic themes. At a minimum, one would have expected more large consolidations as incumbent strategics joined forces, usually by exchanging their stock.

Despite these catalysts, strategic acquirors remained generally dormant for almost two years, due at least in part to enduring wide “bid / ask spreads” born of the extraordinary valuations seen in the runup to and immediate aftermath of the COVID outbreak. Boards of directors – cautious by nature – still regarded most potential acquisitions as too expensive. With respect to issuing stock consideration, they were unwilling to commit to the dilution that would have resulted from issuing shares at challenged valuation levels, even though the valuations of target companies were often even more depressed.

Then, in late 2023, the ice broke. Deals involving strategic buyers started to flow, driven by growing equity values, restored investor enthusiasm for growth and extension, the onslaught of AI adoption, and companies’ willingness to test an evolving regulatory environment.

Last September, Cisco announced its intent to acquire the cybersecurity and analytics company Splunk in a $28 billion cash deal. Among other ambitions detailed in its announcement, Cisco argued that the combination would empower it to use generative AI to simplify complex tools so that more non-technical people can use them.

In January, Hewlett Packard Enterprise (HPE) announced its all-cash $14 billion acquisition of the networking gear maker Juniper. It was a classic tech infrastructure consolidation that HPE said would accelerate AI-driven innovation. A few days later, the chip design software maker Synopsys said it would buy Ansys in a $35 billion cash-and-stock deal, snapping up the maker of software used in creating products from airplanes to tennis rackets.

On February 15th, the Japanese chipmaker Renesas Electronics said it would buy the California electronics design firm Altium for $5.9 billion in cash, as Renesas is looking to offer digital device design to customers.

These headline-grabbing transaction announcements should signal to prospective acquirors of all stripes that strategic-led Tech M&A is back.

According to Standard & Poor’s, the total value of all M&A deals in the first quarter of 2024 was the highest since the second quarter of 2022, when interest rates were still low and digitization was driving dealmaking. In the first three months of this year, strategic buyers spent more than $107 billion on acquisitions. By contrast, the ratio of financial firm deals to all deals has declined from 38% in the first quarter of 2021 to 26% in the first three months of 2024.

The expanding field of buyers has immediate implications for how a potential seller should position itself to find a partner, including:

- Temper your growth goals and emphasize your current – or very near-term path – to profitability. For over a decade, there has been a strong—some would say excessive – emphasis on growth at all costs. While forward growth expectations remain the most correlated performance metric to valuation outcomes, margins and profits matter again.

- Emphasize the underlying economics of the sales motion and the embedded efficiency opportunity that accompanies scale.

- Understand how investors value your potential strategic acquirers and fit your narrative accordingly to develop internal business unit champions who are willing and prepared to spell out the value proposition to their decision-makers.

- Know who you are and what kind of company you will be once you mature. Buyers don’t want to have to figure out your story. Do it for them.

Jefferies expects continued growth in strategic buyer M&A as the first companies entering the capital markets report successful outcomes. However, the increase may be gradual as strategic buyers seek clarity on the evolving valuation, regulatory, and interest rate environments.

Another factor looming large for the back half of 2024 is the U.S. presidential election, which historically does not meaningfully influence dealmaking outside of the largest transactions. However, President Biden and former President Trump present starkly different perspectives on regulation and the Federal Reserve, and some dealmakers may put the brakes on transactions until after the votes are counted.

Despite these uncertainties, the strategic buyer appears to be out of hibernation, which bodes well for sellers better positioned to optimize exit valuations against a more comprehensive set of strategic and financial acquirors.

What’s Driving the Canadian Economy?

The International Monetary Fund expects Canada to be the world’s third fastest growing economy in 2024, and that growth is coming from a more diverse mix of industries than ever before.

Canada is on the rise, which is why Jefferies recently announced the establishment of a full-service investment banking and capital markets presence in the country. It’s a place where we see immense opportunity to help our clients grow, scale and acquire world-class assets.

To better understand Canada’s growth story, we asked John Manley – the new Chairman of Jefferies Canada and a former Deputy Prime Minister with a decorated career in law, business and public service – to share his thoughts.

What’s the state of the Canadian economy today?

It’s been four years since the start of the COVID pandemic and I think we’re still in the post-pandemic phase. We have a lot of parallels with the U.S. where both fiscal and monetary policy were more expansive and accommodative for longer than needed.

I previously chaired a large Canadian bank and saw our deposits going through the roof early in the pandemic because there was simply more income being replaced in the economy by the government than there was lost to the pandemic at a time when supply was disrupted. Inflation was inevitable.

Like the U.S., the Canadian central bank raised rates to tamp down inflation and now they are also on the cusp of cutting rates later this year. Even though the Bank of Canada said the economy has stalled since mid-2023, fiscal policy is still very supportive, and there are plenty of forces aligning to spur growth in the years ahead.

What do you see as the primary drivers of Canadian growth in the months and years ahead?

Historically, the Canadian economy has been more akin to Australia than the U.S. because we have such a strong base in natural resources. Energy and financial services alone account for almost half the value of the Toronto Stock Exchange (TSX). But on a relative basis, the share of energy and financial services is shrinking. Materials and industrials are expanding. Technology has almost doubled its presence in the TSX, and the third most valuable company in all of Canada is Shopify, an ecommerce retailer.

So the economy is becoming more diversified and many of our leading companies are in a position to both sell more into the U.S. and to attract more capital from all over the world. That said, I still believe that Canada’s “family business” is the extraction and processing of our immense natural resources. Demand for energy and minerals, as well as the output from our agricultural, forestry and fishery industries are strong and growing.

What are the most important strengths of the Canadian economy?

It starts with the most important asset of any country or company: The people. Canada has a highly educated populace and in fact we have the second highest share of people in the world with a post-secondary education behind only South Korea. We have one of the fastest growing populations in the world and much of that growth is fueled by immigrants, who now make up almost a quarter of the country. Canada brings in almost as many immigrants as the U.S. annually even though our population is only about one tenth the size. So we have a dynamic population that is also very entrepreneurial, and the low barriers to starting a business means that we have a very high rate of new business formation.

And then there is the family business of providing the food, fuels and minerals the world needs: We’re the 5th largest exporter of agri-food and seafood, 4th largest of metallurgical coal and of crude oil, and the 6th largest exporter of gas.

Where are the untapped opportunities in Canada?

For all of Canada’s strengths, we only have 40 million people so companies can only get so big selling to our domestic market. I think one of Jefferies’ biggest value adds for our clients will be helping them make more inroads into the U.S. and global markets.

Our openness to immigrants has been a significant strength but we’ve also been overly reliant on workforce growth as a driver of our economy because Canada has lagged U.S. productivity growth for an extended period of time. But I do think there are several developments on the horizon that could enhance our productivity. One example is the completion of the Trans Mountain Extension Pipeline which will expand our ability to transport oil from Alberta from the Port of Vancouver. Economically speaking, that’s been all money going in with no GDP growth to show for it. But once the extension comes online, that could increase GDP by as much as 0.5% and simultaneously improve the productivity measure. In addition, as Canada’s technology sector continues to expand and artificial intelligence enables more efficiencies for all of our companies, that should also spur productivity.

What has you most excited about Jefferies’ opportunity in Canada?

Canada has everything the world needs. We have energy, water, agricultural and mineral resources, and so much else. We have an educated population and high standard of living that supports a vibrant consumer market. So this is a growing and diverse economy and whatever the sector, Jefferies has someone with expertise who can help our clients find opportunities in them.

All we lack is scale, which access to US markets can help provide. Enabling our clients to benefit from their proximity to that massive neighboring market is at the top of my list of objectives for Jefferies Canada in the short term.

Taking on Google: Perplexity’s Quest to Redefine Search with AI

In February, The New York Times profiled Perplexity, a buzzy year-old startup whose AI-powered search engine is loosening Google’s grip on the market. “Can This AI-Powered Search Engine Replace Google?” the article asked.

Only three months later, Perplexity announced a $62.7 million funding round that valued the company at over $1 billion. It drew heavyweights from OpenAI, Amazon, Nvidia, and other tech giants, cementing Perplexity as a key player in AI.

The company offers an alternative to users frustrated by Google’s ad-heavy and SEO-driven search results. Instead of serving up links, Perplexity aggregates information from credible sources into a single, cohesive answer.

This method, according to CEO Aravind Srinivas, represents “a better way to experience the internet.”

At Jefferies’ 2024 Private Internet Conference in Los Angeles, Srinivas sat down with Gaurav Kiuttur, Global Co-Head of Internet Investment Banking, to discuss the shifting search landscape, Perplexity’s growth, and competition from Google and OpenAI.

Their conversation comes on the heels of Perplexity announcing Enterprise Pro, its first B2B offering that delivers the platform with security and control at enterprise scale.

The following Q&A was lightly edited for clarity and length.

There’s been a ton of buzz around Perplexity over the last year. Can you tell us about your platform and business model?

Perplexity is a conversational answer engine. Instead of serving you ten links, it cuts the signal out of noise and gives you the answer you’re looking for.

Our current business model is subscriptions. A lot of people made fun of us for using subscriptions, asking “why would someone pay for search when Google is free?”

Well, Google is filled with spam, ads, and SEO. For people who value their time, $20/month is a worthwhile investment. We’ve successfully challenged conventional thinking around search, bringing a viable new business model to the space.

For people who haven’t used Perplexity, can you describe the user experience and how it differs from Google?

With Google, you get links. With Perplexity, you get answers.

Perplexity aggregates and resolves several links at once, giving you a summarized answer with citations. And you can ask follow-ups. You can converse with it.

Using Perplexity is like being in dialogue with the world’s smartest person who has all the internet’s knowledge at their fingertips. It’s like Wikipedia and ChatGPT had a kid.

How replicable is the technology? What’s Perplexity’s secret sauce?

Building the prototype itself isn’t that difficult. What’s hard is delivering it at scale.

All the minor details we manage – UX, speed, latency, accuracy, mobile responsiveness, iterative improvements. That, and the scale of users we have.

The way that we tackle hundreds of small details at scale is very hard to recreate. And by the time someone recreates it, we’ll only be further ahead.

Talk about OpenAI. What are the big differences with ChatGPT, their consumer product?

There is a simple way to understand this. For a product like ChatGPT, hallucination is a feature. For a product like Perplexity, where the goal is accurate answers, hallucination is a bug.

If I prompt ChatGPT with a creative task, like writing a poem or a joke, it has to hallucinate. The more it hallucinates, the more entertaining its response.

With Perplexity, we offer something similar in our “writing mode,” but the default functionality is to answer questions with rigor and citations. In that sense, we approach our product differently than ChatGPT.

Note: “Hallucinations” are misleading results generated by AI models, due to flaws in their training data, incorrect assumptions, or biases.

Where does Perplexity get its data? How do you ensure sources yield accurate answers?

From the beginning, we’ve been very mindful about which data sources we allow to contribute to answers. We want high-authority sources of information.

One useful proxy for this is peer review. You can’t publish something to The New York Times or The Wall Street Journal without it being approved by your editor and colleagues. That peer review gives content a high trust score.

Content on Twitter or Medium, on the other hand, is not really reviewed for accuracy. We take these factors into account and create a core of trusted domains on the web.

Then, as the product is used by more users and you get a sense of the best domains, you continue updating those trust scores to build a more and more refined product.

So far, how are you finding the market for users willing to pay for search? Is it big?

It’s a huge market, and we’re just getting started. There are millions of people using our product for free today, which gives us a massive funnel to convert from.

And beyond that, platforms like Google have billions of users, so there are so many more people to acquire at the top of the funnel. There are billions of dollars in revenue to make here.

And are there plans for an ad-supported version?

Definitely.

I’m a big fan of how Google built a very high-margin business through advertising. Unfortunately, it’s come at the cost of their core mission of “organizing the world’s information and making it accessible and useful.” Now, the product is designed more for the advertiser than the user.

We have ideas for integrating ads without compromising our core mission. That might mean building a lower-margin business than Google, but that’s okay with us as long as we are profitable and successful.

Finally, what does Perplexity look like in the next couple of years? How do you think about scaling?

We want to have an order of magnitude more users. Our queries should be more accurate. We should offer more diverse formats of answers – not just paragraphs but knowledge panels, scores, and more. This will be important for the Olympics and the election.

We also want to enable multimodal experiences: voice form factors, image form factors, distribution across several devices and powering every knowledge worker’s day-to-day workflow. People should be able to do more with Perplexity answers. They shouldn’t just read it and walk away.

The AI market needs to transition from chatbots to actually supporting workflows. If Perplexity can succeed at that, we have a really, really good shot at a big chunk of the AI profits.

Beyond Owning a Private Jet: Alternative Private Aviation Services

Thirty years ago, the private aviation market almost exclusively consisted of the people and corporations in many industries that owned private jets.

Not anymore. Today, 40% of the world’s 446,000 private jets are in the hands of private aviation companies – like NetJets, Vista and Flexjet – that offer customers more flexible choices of aircraft, greater security, and greater privacy. When even Taylor Swift is selling her private jets, you know something has changed.

These changes are creating new and substantial investment opportunities for a growing and diversified group of investors. They increasingly view the private aviation industry as a place for stable investments like those in commercial aviation services, airports, and airlines.

The influx of new investors, in turn, is creating new opportunities for owners of existing private aviation businesses by providing them with more access to capital and opportunities to realize advantageous exits.

The $37 billion private aviation industry has been steadily growing since the 1990s. The pandemic supercharged a long-term growth trend, with a 40% increase in flight hours between 2019 and 2023.

While private jet ownership has always offered more security, flexibility, comfort and amenities than commercial travel, alternative private aviation companies offer even more advantages. They provide the “right-sized” lift for each flight based on the distance traveled and number of passengers. The alternatives now include:

- Fractional ownership, where a buyer purchases anywhere from 1/16th to one half of an aircraft.

- Program membership, where the passenger purchases 50 or more hours per year of guaranteed access to a fleet of private aircraft anytime and anywhere.

- Jet cards, where the passenger purchases 25 or 50 flight hours on an operator’s fleet.

- On demand charters, where the passenger receives a bid for each separate trip.

- Aggregation services that allow passengers to buy tickets on shared charters or to access empty seats on private flights.

In addition to the convenience, flying with alternative services limits the ability of others to track your movements. This can be crucial to executives, bankers, and lawyers engaged in confidential deals who want to reduce public scrutiny, as well as notable figures looking to keep their private lives private.

Key Trends

Several tailwinds are propelling private aviation forward and attracting an influx of capital.

All of the alternative aviation models have the goal of increasing utilization per aircraft – picture Uber for private jets. The average personal private jet flies fewer than 200 hours per year, even though the aircraft is capable of flying over 1,200 hours. Increasing utilization by allowing more than one flyer to use the same aircraft simply makes flying private more economical.

Market growth and the transition towards fleet operators has also created an opportunity for operators to gain scale, greater margins, higher cash flows, and more mature capital structures.

Growth has also trickled down the private aviation supply chain. Providers of aviation services, such as maintenance organizations and fixed base operators (FBOs), have benefitted from more predictable demand. Larger operators can sign longer-term, higher dollar contracts. This benefits their suppliers and further strengthens the entire private aviation market.

All of these factors have increased interest from institutional capital. Fifteen years ago, the private aviation industry was dominated by entrepreneurs and family- or management-owned assets. Ten years ago, venture capital and growth equity investors began investing in the sector. Now the investor universe is expanding even further:

- Infrastructure funds are emerging as the core investor group in FBOs – changing the industry by creating higher return requirements and valuations.

- Experienced aerospace-focused private equity funds are leveraging their expertise in commercial aviation services via investments in private aviation-focused maintenance repair and overhaul (MRO) services.

- Travel, tourism, and hospitality investors are funding branded operators and FBOs with structured equity or debt investments.

- Family offices with long-term investment horizons are evaluating a wide range of opportunities including asset-light operators and tax-efficient investments in aircraft.

In total, over $20 billion of institutional-backed capital has been deployed into private aviation operators and supply chains since 2019 in the form of both equity and debt, and there is significant space for future investments across a range of business models and transaction structures.

Opportunities for Investors

Institutional investors have many entry points into the space depending on what they want from an investment. Asset light operators tend to have lower margins but are lower risk investments. Operators that own their fleets offer opportunities to deploy capital throughout the ownership period to fund growth. MRO operations display similar dynamics to the well-capitalized and familiar commercial aerospace sector, but often come with labor issues and dependence on OEMs. Integrated providers offer multiple avenues for growth but may be more difficult to value.

Private equity interest in this industry is being driven by a few common themes:

- The private aviation sector has displayed stable, long-term growth, paired with the emergence of professionalized and scaled businesses.

- Private aviation is tied to GDP and even more closely tied to wealth creation and high-net-worth individual population growth.

- Aviation is and will always be a highly regulated end market, which creates barriers to entry for new competitors and high switching costs for customers. This assures recurring revenues.

- Aviation, and private aviation in particular, is generally a capital intense sector and will require investment to fund growth like operators’ fleet expansion, MROs increasing capacity, FBOs improving networks, etc.

- The sector remains highly fragmented with considerable consolidation opportunities remaining.

- New business models create a dynamic marketplace with a wide range of alternatives for investment strategies in the sector.

Implications for Private Aviation Companies and Existing Shareholders

Interest from institutional investors will offer expanded opportunities for existing businesses in private aviation to gain access to capital and spur faster growth.

Founders can partner with experienced investors to professionalize their businesses and create war chests to realize aspirational growth strategies like geographical expansion or M&A. Partnering with institutional investors also allows companies to take risks for future growth and create succession or exit plans.

While demand from institutional investors has been growing and remains robust, we anticipate a handful of changing dynamics:

- Businesses will increasingly use public debt and equity to scale, likely utilizing instruments often seen in the capital structures of players in the commercial aviation space (e.g., EETC and ABS debt structures, tax-efficient municipal financing, high-yield notes, etc.).

- Infrastructure investors are likely to expand their scope beyond FBOs into other subsectors of aviation. These offer consistent and visible revenues and profitability, especially with the limited availability of traditional infrastructure assets.

- There will be more creative transaction structures including use of more diverse products such as preferred equity and convertible debt to protect investors’ downside and share upside when venturing into new sectors.

- Earlier stage investors may have to move their hunting ground further upstream to areas like electric vertical takeoff and landing (EVTOL) aircraft, aviation software, sustainable fuel, and other next-generation technologies.

As with any industry, there will be winners and losers – but the secular growth trends across private aviation and the excitement from the broader investment universe should create an environment of highly profitable exits for entrepreneurs and company founders. It is they, of course, who took risks years ago to create today’s private aviation landscape which is set for success for years to come.

Katya Brozyna is a leader of Jefferies’ Aviation & Aerospace Investment Banking practice. With over ten years of experience, Katya specializes in capital raising and advisory for clients across business aviation and commercial aerospace end markets. She has completed over 75 M&A, debt and equity transactions for operators, FBOs, MROs, manufacturers, leasing companies and other sectors in the aviation landscape. Katya received a B.S. in Finance and Accounting from the McIntire School of Commerce at the University of Virginia. She can be reached at [email protected]

On the Brink of a Super Cycle: What’s Next for Oil and Gas?

Rising interest rates and fears of recession dampened dealmaking across much of the global economy in 2023. One sector, however, not only showed resilience but set new records. Global energy companies reached their highest valuations since 2016, with 1,135 deals generating $281 billion in global M&A value, an 8.2 percent increase over the previous year.

This growth was largely driven by American oil and gas, where the world’s largest energy producers turned to address the global supply shortage. The year culminated in a series of mega deals, including Chevron’s agreement to acquire Hess and Exxon’s agreement to acquire Pioneer Natural Resources, the two largest transactions of 2023.

So far, 2024 has been another big year for the sector, but could growing uncertainty about Fed rate cuts threaten its momentum? Jefferies sat down with Pete Bowden, Global Head of Industrial, Energy, and Infrastructure Investment Banking, to discuss the energy sector’s consolidation, the potential for a “super cycle,” and more.

Consolidation and Expansion: Oil and Gas in 2023

In 2023, major geopolitical events, including the ongoing Russo-Ukrainian war and a new conflict between Israel and Hamas, continued to strain the global energy supply. With diminished access to oil from Russia and the Persian Gulf, Western countries looked to the United States for relief.

In response to rising global demand, integrated oil companies – which operate across the upstream, midstream and downstream sectors – looked to expand their inventories in the Permian Basin. This region, spanning western Texas and southeastern New Mexico, is the country’s highest-producing oil field.

“Global supply is falling short by five to eight percent of what’s needed,” Bowden shared. “Oil companies recognize that North American production is more important than ever, and inventory is limited. They’re focused on the Permian Basin, which is the epicenter of US drilling.”

In the final months of 2023, the industry saw significant consolidation: Chevron agreed to acquire Hess for $53 billion; ExxonMobil agreed to purchase Pioneer Natural Resources for $59.5 billion; and Occidental Petroleum committed to buy CrownRock for $12 billion. This trend continued into 2024, with Diamondback Energy announcing its agreement to acquire Endeavor Energy Partners for $26 billion. Jefferies served as lead financial advisor on the deal.

These transactions, all focused on the Permian, reflect efforts by integrated oil companies and large independents to bolster their reserves.

“As prime locations in the Permian are snapped up, what were once considered tier-two drilling locations will gain importance. Given the global shortage and America’s role as a supply hub, the economics should work in a half a dozen major US basins,” Bowden predicted.

Macro Headwinds and Sector Resilience: The Energy Outlook in 2024

Though M&A in the energy sector has been strong, rising skepticism about anticipated 2024 rate cuts could reduce companies’ appetite for new deals. Persistent inflation and a robust labor market have led some economists to doubt a rate cut this summer. However, commodities like oil and gas, traditionally a hedge against inflation, don’t always respond to rate changes like other asset classes.

“Right now, we’re in the perfect environment for oil and gas dealmaking. There’s a belief that interest rates are coming down and the assets are becoming more valuable,” Bowden said. “Even without a rate cut, the oil and gas bond market should continue to outperform. Prices will stay constructive, and there will still be deals.”

Bowden noted that mega deals from integrated oil companies are pressuring businesses of all sizes to transact. This push might signal the start of a “supercycle” in American oil and gas.

“With the industry consolidating, what were once large independents are now effectively mid-caps, and mid-caps have shifted to small-caps. Companies need to make deals to stay relevant,” he explained. “My perspective, as a generally skeptical guy with 25 years of industry experience, is that it is as good a market as we’ve seen and we’re likely heading into a super cycle.”

Though the energy transition is underway, it cannot progress quickly enough to offset current shortages in the global energy supply. As geopolitical conflicts, new and ongoing, create tailwinds for domestic oil production, American energy companies are expected to keep seeking opportunities to boost production and build their reserves in US basins.

For more insights from Pete Bowden and Jefferies, the leading advisor on M&A transactions in the energy sector for the last decade, read this recent interview with Bloomberg on the sector’s outlook in 2024.

Where is the Private Internet Market Headed in 2024?

In 2023, two-thirds of venture capital investment went into AI-related businesses.

Much like the widespread adoption of mobile technologies 15 years ago, AI is poised to radically reshape the private internet market. But how?

This is just one of the questions we put to Gaurav Kittur, Global Co-Head of Internet Investment Banking, and Cameron Lester, Global Co-Head of Technology, Media, and Telecom Investment Banking, as they prepare to host hundreds of investors and company leaders at the Jefferies Private Internet Conference in Santa Monica, CA. They share their thoughts on AI, on the changing exit paths for private companies, the impact of regulatory and geopolitical challenges and much more below.

Q: How do you see investment flows shifting as we progress through 2024?

GK: Consumer spending is still the vast majority of the GDP in the U.S. and many other countries, but the funding for consumer internet businesses – from seed all the way to the growth side – has slowed to a trickle. Now we see all this movement into AI-related businesses, particularly toward the infrastructure required to build the best models. So, I see similarities to 2008 when you had significant capital flowing into the infrastructure and operating systems for mobile, which then subsequently spurred the creation of companies like Uber, DoorDash, Airbnb and so many others. Soon, basically every consumer-facing application will have an AI-component to it, but it still isn’t clear exactly what that will look like yet.

That is why our Private Internet Conference will have a combination of AI-first companies along with more traditional consumer internet companies that are searching for ways for AI to enhance their business.

CL: For over a decade, there was an unprecedented wave of technology investment and innovation driven by four big themes. One was the broad adoption of mobile computing and development of Apple’s App Store and the Google Play Store. Two was the network effects of marketplace businesses – like Uber – and subscription businesses – like Netflix – that provide value to the consumer at a fraction of the cost. Three was the ability of brands to be completely created, discovered and grown digitally without ever having to first develop a brick-and-mortar presence. And four was the powerful unit economics of digital customer acquisition. This turbocharged the growth of so many businesses and yet each of these four themes is somewhat played out. Everyone’s on mobile, everyone has a digital presence and now Apple’s privacy changes have made customer acquisition harder.

It is causing a fundamental rethink of consumer internet business models and a big part of the solution will be finding ways to apply AI to consumer behaviors.

Q: What kinds of investments in AI are most compelling right now?

GK: We have seen these funding rounds for companies like OpenAI and Anthropic, which are really about making the AI-models more powerful. That requires a ton of capital because the only way that the models can get powerful is by training, right? The more data that you give it, the more reps effectively it gets, the stronger it becomes.

Then the question becomes what can this model do for you? Can you take it and plug it into a video editing app or a new game engine or a new music discovery platform? That’s where the next wave of discovery and business creation will come from. Some incumbent players will figure it out and they’ll get stronger, but some won’t, just like some couldn’t figure out mobile.

This will create the opening for some massive new companies in the next five to ten years. AI-investment might even enable meaningful competition for some very well established businesses, with just one example being Perplexity’s search engine offering. That’s starting to make a dent in a space where Google has had meaningful market share forever.

Q: Investment activity is slowly picking up, but investors are certainly being a bit more selective in what they fund. What are they looking for?

CL: The cost of customer acquisition through the traditional channels has become much more challenging. So, a strong organic word of mouth and natural organic growth model for customer acquisition is incredibly important.

A company really needs to show a path to profitability and expanding margin as well. Growth is always important, but you’re not going to get a hall pass for growth without a logical way to bring the cost of the revenue together and then scale the profitability.

In a more disciplined environment, investors will also tend to put a higher premium on funding already successful entrepreneurs. So, you look at the deal where Jefferies just served as the Placement Agent for the food and delivery app Wonder in its $700 million growth equity raise. This company was created by Marc Lore, who previously sold businesses to Amazon and Walmart. That’s the kind of founder experience that will always help prospective investors sleep better at night.

GK: I’d add that you really need to be able to show product-market fit and that the unit economics work as you scale up the business. There have also been several instances in tech – like with FTX and WeWork – where a founder wasn’t operating with proper controls. So, I am also seeing a renewed focus on governance, management and the proper board structure of companies.

Q: Antitrust activity is escalating in the U.S. and around the world. What do see as the most significant political or regulatory risks for private internet investors?

GK: For years, the major tech companies moved into strategic segments via acquisition, but that window is essentially shut for the time being because of the regulatory scrutiny. That’s one of the factors that should help the IPO market open up over time because there is a lot of pent up demand.

Obviously, the regulation of AI will continue to be a subject of conversation – and companies in this space need to be a significant part of it – but it’s just too early to forecast what any kind of durable regulatory AI regulatory framework would look like.

CL: Geopolitical risk is becoming a significant consideration. There is a war in Europe and in the Middle East. China-U.S. relations are eroding. Investment dollars flowing into China are dwindling and funds that would have gone to China five years ago are now going to India or elsewhere in Southeast Asia. So I think investment committees will be looking very closely at where businesses are located, how they’re interacting with other regions and what kind of risks that may create. With that said, it’s important not to overreact to short term geopolitical developments. For example, Israel is enduring one of the most challenging periods in its history. But Israel’s resilience and economic fundamentals – an educated populace, an ingrained culture of innovation and entrepreneurship and increasingly deep capital markets – are all still there. That’s why Jefferies is still so committed to growing our presence in Israel.

Q: Aside from AI, what do you think will be notably different about this coming cycle of investment in the private internet space.

CL: We’ve talked a lot about how AI will transform consumer businesses but it will also have such a seismic impact on small businesses. The small business customer does not have the time to do customization and these large language models and AI can improve and make small businesses much more effective in acquiring their own customers and servicing them than ever before.

GK: The growing role of private equity is very interesting to me as it has been a player on the software side but it is also starting to pay much more attention to private and consumer internet companies. Thus far, sponsors have had interest in what you might think of as Web 1.0 companies, like Yahoo or Trip Advisor. But you will ultimately see sponsors looking at other more mature, highly profitable businesses where leverage can be used to enhance returns.

This has been a bumpy few years for the private internet market and the progress from here won’t be linear. But there is so must justifiable enthusiasm about the new technologies and entirely new business models that are about to be created.