How Japan’s GX Plan Aims to Decarbonize the Country’s Toughest Sectors

Jefferies recently wrote about Japan’s Green Transformation Policy (GX), a $1 trillion plan to dramatically reduce emissions over the next decade. This initiative represents nearly three times the annual GDP investment percentage of the U.S. Inflation Reduction Act — yet it has largely flown under investors’ radar.

Decarbonizing Japan’s economy comes with unique challenges and opportunities. Japan relies more on coal (the most carbon-intensive fossil fuel) than its high-income peers, and a large share of its energy is imported. At the same time, Japan can draw lessons from other countries’ transition policies and emissions trading schemes, giving it a significant second-mover advantage.

Historically, Japan has lagged in energy transition investment. Last year, it made up just 2 percent of global energy transition spending, despite being the world’s fourth-largest economy. Smaller economies, including India, the U.K., and Brazil, matched or outspent Japan in 2023.

The GX plan is specifically designed to address these challenges. It targets high-emission companies with an aggressive decarbonization strategy — aimed at maintaining their economic performance and the country’s energy supply.

Here’s how it works in five key steps.

- Target Setting: Japan’s slow start in the energy transition isn’t stopping it from setting ambitious, fast-moving goals. The GX Plan aims to reshape the country’s power mix by 2040, with 40-50 percent from renewables and 20 percent from nuclear. These targets set the stage for bold policymaking and investment — detailed in the steps that follow.

- Transition Sovereign Bonds: Between 2023 and mid-2029, Japan will issue ¥20 trillion in transition sovereign bonds. Unlike the “green bonds” of the IRA, which fund climate projects across the economy, transition bonds specifically help high-emitting companies lower emissions — moving from “brown” to “less brown” or “greener.” Proceeds will fund R&D through the Green Innovation Fund and support decarbonization efforts via the Subsidy Program, with a focus on Japan’s hardest-to-decarbonize sectors.

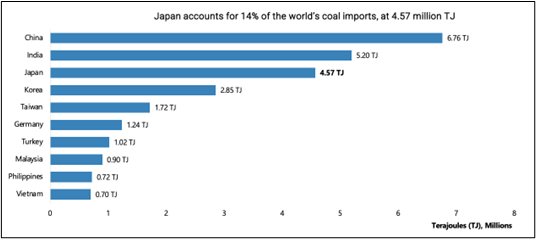

- Carbon Levy on Fossil Fuel Imports: Japan accounts for 14 percent of the world’s coal imports, trailing only China and India. Starting in 2028, it will introduce a carbon levy on fossil fuel importers, with rates increasing over time. Revenue from the levy will be used to repay the principal and interest on GX Transition Bonds. By linking fossil fuel imports to decarbonization funding, Japan is creating a built-in financial mechanism to curb coal dependence while sustaining long-term support for its transition strategy.

- A National Emissions Trading System (ETS): Japan launched its national ETS in FY2023, beginning with voluntary participation through the “GX League” — a group of 747 companies responsible for over 50 percent of the country’s GHG emissions. Notably, 18 of the 20 highest-emitting Japanese stocks (Scope 1 + 2) have joined. This voluntary phase runs through FY2025 before transitioning to a mandatory ETS in 2026. Japan has the opportunity to learn from the successes of ETS efforts in Europe, China, and beyond. More details on its plan will be released this year.

- An Innovation-First Approach to Climate Policy: Japan’s GX Plan prioritizes research and development in addition to subsidies — a strategy aimed at positioning the country as a global hub for climate tech and clean energy innovation. More than half of the transition bond proceeds will fund R&D through the Green Innovation Fund. The plan also dedicates JPY 200 billion over five years to deep tech startups and JPY 700 billion to support small and medium-sized enterprises driving the energy transition.

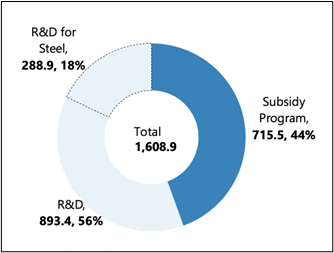

This chart illustrates the use of proceeds for the February Bond Auction (representing 1.6T JPY of the total 20T JPY to be issued).

Japan’s decarbonization path comes with unique challenges—but it’s being tackled with an equally unique strategy.

The scale and structure of the GX Plan—its incentives, R&D focus, and diverse climate finance tools—set Japan up for one of the most ambitious energy transitions in the developed world. Jefferies, and investors everywhere, should keep a close watch.

Follow along for more insights from Jefferies’ Sustainability and Transition Team on the Japan GX Plan and other important climate investing themes in the weeks ahead.

Grid Upgrades Are Lagging—Can Drones Change That?

Last February, Jefferies wrote that upgrading and expanding grid infrastructure was widely viewed as the biggest obstacle to a net-zero future.

Clean energy investment was surging, but grid development lagged badly. Existing infrastructure was severely unprepared for the projected load growth of the next decade.

A year later, new innovations aimed at modernizing the grid are gaining traction—and one, in particular, is turning heads. Infravision’s drone-enabled power line stringing uses unmanned aerial vehicles to install power lines faster and more cost-effectively than traditional methods.

Could this be the breakthrough that speeds up grid deployment while cutting costs and improving safety? Jefferies’ Sustainability & Transition Team sat down with Infravision’s founders to explore where drone-enabled power line stringing stands today—and what it could mean for the global transition.

This article recaps Jefferies’ interview with Cameron Van Der Berg, Co-founder and CEO of Infravision, and Brian Leveille, the company’s CFO. For a deeper dive into their insights, read the full report from Jefferies’ Sustainability & Transition Team.

A New Approach to Transmission Replacement

The United States needs to more than double existing regional transmission capacity by 2035, according to the Department of Energy’s 2023 Needs Study. A key piece of this effort is replacing aging power lines with new and advanced materials—an effort that’s expensive and, in some cases, risky.

Infravision’s drone-enabled approach is tackling the challenges of transmission replacement head-on. Its proprietary TX System pairs a heavy-lift drone with an electric smart puller tensioner, enabling automated, high-precision power line stringing across long distances.

According to Van Der Berg and Leveille, this system offers three key advantages:

- Safety: The drones take on high-risk tasks—like working at elevated heights or in difficult terrain—reducing the need for direct human intervention. This lowers the risk of accidents while allowing crews to stay focused on other critical tasks.

- Efficiency: Drones can reach remote areas that ground crews and helicopters can’t, helping to speed up project timelines.

- Savings: The system offers lower cost per phase mile than traditional methods while also reducing overhead expenses.

The founders believe these benefits position Infravision to significantly disrupt traditional power line installation.

Infravision’s Market Opportunity & Growth Strategy

Infravision’s drones aren’t just an R&D experiment—they’re already in operation, with real projects and growing scale. Their primary customers are utility companies and engineering, procurement, and construction (EPC) contractors, including a 50-kilometer, 250-megawatt high-voltage line with Powerlink Queensland.

Infravision has also partnered with PG&E to deploy its drones on power lines and is now working with Sterlite Power in India. As global power demand and electrification efforts accelerate, the company expects to expand its presence across international markets.

The company’s total addressable market is significant, backed by $200 billion in planned transmission capital expenditure and $870 billion in distribution capex and opex globally in the coming years. Following a $23 million Series A funding round led by Energy Impact Partners, Equinor Ventures, and Edison International, Infravision plans to double its workforce over the next year.

New Opportunities in the Energy Transition

Drone-enabled solutions create a wide range of opportunities for the energy transition.

They don’t just improve cost and safety efficiencies in transmission installation—they also shorten project timelines, freeing up skilled workers for other transition projects. Additionally, companies like Infravision make large-scale T&D construction more feasible in non-Western countries, where high costs have historically been a barrier.

For more on Infravision’s solutions, check out Jefferies’ full recap of the team’s recent conversation. For deeper insight into the energy transition, climate tech, and related opportunities, explore the Jefferies Sustainability & Transition Team’s work on Jefferies Insights.

Prime Services C-Suite Newsletter – December 2024

Jack-of-all-Reads: A newsletter for multi-hat-wearing C-suite leaders and their key constituents.

Regulatory Initiatives, Liquidity Trends, and AI in Relationships

Wishing you all a wonderful Holiday Season and success in the New Year! We welcome and appreciate your continued partnership.

Industry Insights:

2024 was a year marked by macro and geopolitical uncertainty, but despite this unpredictability, the U.S. equity markets massively outperformed. The S&P 500 and Nasdaq have risen 26% and 28% respectively as of end of November1. What do we think this current backdrop means and what are a few keys to success in 2025?

- Lower Quantity but Higher Quality in the New Launch Landscape: While the number of managers launching new funds is lower than in years past, the quality is higher. Hedge fund consultant & technology provider, PivotalPath, has tracked 145 “quality new launches,” defined as managers spinning out of shops with >$1bn in assets. A major backer of these high-quality launches are large Multi-Manager platforms. This is giving much needed “oxygen” to the new launch space, allowing pedigreed groups to get off the ground and cover their startup costs much quicker.

- Top Performance: Despite the notable decline in both headline launches and liquidations, reversing 2023’s trend when net new launches turned positive, hedge fund industry assets continue to surge, topping the $4 trillion mark, which is likely due to performance-based growth.

- After experiencing outflows in 2022 and 2023, hedge funds reversed this trend, attracting nearly $23.04 billion of net inflows through Q3 2024, but a majority of the growth in assets, approximately $324.8 billion, has come from hedge fund performance.2

- Top Performance: Despite the notable decline in both headline launches and liquidations, reversing 2023’s trend when net new launches turned positive, hedge fund industry assets continue to surge, topping the $4 trillion mark, which is likely due to performance-based growth.

- Hedge Fund Concentration: The number of hedge funds in the industry is sitting at 8,213, up slightly from the 8,145 that existed in 2023, but below 2015 peaks. As the number of hedge funds remains steady and assets continue to swell higher, the trend of further industry concentration prevails, which is evidenced by the fact that firms with greater than $1bn in AUM account for 85.50% of assets in the industry.2

- Increased Consolidation: Flows have been bifurcated to the largest ($5bn+) and smallest (<$100mm) managers,2 this year pointing, perhaps paradoxically, to this trend of industry consolidation amidst a healthy new launch backdrop.

- A Spotlight on Performance YTD: On a year-to-date basis, 89% of all hedge funds are reporting positive performance, according to PivotalPath, producing an average return of ~15%. When evaluating fund performance based on AUM, smaller managers in the $100mm to $250mm range have been the best performing cohort year to date, while managers in the $2.5bn to $5bn range are lagging behind by more than 600bps.

- Alpha Production: Most hedge funds are posting positive returns this year, however, the major hedge fund indices, as tracked by HFR, are lagging behind equity market indices. Through November, the S&P 500 is up about 26%, while the MSCI World has surged about 20%.1 Contrarily, the HFRI FWC is only up about 10%, and the HFRI Equity Hedge is up approximately 13%.4 Despite this, hedge funds are still conserving capital and producing alpha – PivotalPath’s composite hedge fund index demonstrates that through November hedge funds are producing an average 5.8% of alpha over the S&P.

- Sector Focus: When focusing specifically on healthcare performance, the HFRI Healthcare index is performing above both the XBI and IBB. Growth in both healthcare and technology sector assets have been on a steady incline over the past three years. The growth seen from the healthcare and TMT groups is slightly ahead of that in all equity hedge assets. Interestingly, there are still net outflows which is a contrast from net inflows of the overall hedge fund industry.

- Fundraising as a Top Challenge in 2024….But Optimism for 2025: Capital raising for hedge fund managers proved challenging in 2024, especially as equity markets surged, interest rates remained high, and economic uncertainty prevailed.

- Creating Liquidity: Moreover, many institutional allocators still reported being hamstrung by their privates allocations, looking to their hedge fund books as a form of liquidity. In Dynamo Software’s 2024 Hedge Fund Report, hedge fund managers ranked fundraising as their top business challenge, followed by delivering alpha, managing key client relationships, and recruiting talented employees.

- “Hit the Ground Running”: The majority of hedge funds are determined to increase marketing efforts in 2025, with more than 55% of the groups surveyed in the study anticipating ramping up their capital raising efforts in the New Year.

- The War for Talent Wages On: As many job seekers are now placing an increased emphasis on firm culture, they may also have expectations of career development opportunities across levels, creating alignment of autonomy, flexibility, and purpose.

- Trends in Hiring: Unsurprisingly, multi-manager & multi-strategy funds, as well as equity long short managers, have been some of the most active groups hiring new talent, according to data compiled by With Intelligence. Multi-Manager platforms specifically were responsible for nearly 40% of hiring in the industry in Q2 2024. Across all firms, 63% of new hires were on the investment side, while the other 37% were on the noninvestment side, across various legal, operations, and technology focused roles.

- Role Type: Overall, industry headcount in non-investment roles has increased from 40% to 54% since 2015,5 pointing to the increased focus on non-investment functions such as technology and infrastructure, treasury, and portfolio financing.

Regulatory Corner:

SEC’s Regulatory Enforcement Priorities – What’s in focus for 2025?: Coming off a very active year on the regulatory front in 2024, the SEC has released their enforcement priorities for 2025. Some exams have led to full sweeps of all aspects of a firm’s procedures. As a result, compliance teams are focused on making sure their policies and procedures are reflective of the firm’s practices and that their team is well versed on what should be included. Although many of these rules have been discussed at length, below are some current industry insights and areas of focus for our clients:

- Regulation SHO: This rule has a compliance date of January 2nd, 2025 with the first report due in mid-February (2 weeks post month-end). Managers should begin to track which securities meet the threshold.

- Regulation S-P: The SEC adopted amendments to Regulation SP in May of 2024, and firms with over $1bn AUM have until November 2025 to comply with the ruling.

- AI Enforcement: The term of “AI Washing” has been gaining popularity, especially as regulators want to ensure that managers are not overselling their use of the technology. Because part of the SEC’s focus is on emerging financial technologies, they are expected to release a Predictive Data Analytics rule in 2025, which should encompass managers’ use of AI.

- Marketing Rule: The first sweep of sanctions when the New Marketing Rule was released in 2022 were mostly focused on hypothetical performance and returns. However, now the most common deficiencies are related to testimonials or endorsements from 3rd party ratings, as well as fees and expense calculations.

- Cyber Security: The SEC is aiming to evaluate if a fund has a comprehensive business continuity plan in place and that this plan has been tested. Any plans should outline appropriate vendor due diligence processes, as well procedures to ensure investor information is protected. Third party controls and governance practices will also be reviewed

Spotlight on Content and Events:

Terms Analysis: The Jefferies Capital Intelligence team has compiled the most recent trends and fee studies with focuses on Long Only, Healthcare, Emerging Managers, and TMT hedge fund managers. As discussed in the most recent edition of the newsletter, throughout 2024, the team has observed firms being more creative with their terms and fees, oftentimes even creating unique share classes to cater individual investors’ needs. Some key findings from each vertical include:

- Long Only: Since 2022, equity long only mandates have accounted for about 33% of all equity mandates, up from the 30% they accounted for in the 2021-2023 timeframe.

- Healthcare: Historically, healthcare funds have charged higher fees than traditional long short fund; however, after reviewing the fund terms of healthcare funds that launched between 2022-2024, the team found that healthcare terms have become more aligned with traditional long short funds.

- Emerging Managers: Since 2022, the team has consistently observed over 80% of emerging managers choosing to outsource their trading functions, and while less common than choosing to outsource trading, the team has seen more than 30% of emerging managers choosing to outsource their CFO/CCO/COO function.

- TMT: In terms of redemptions, most directional managers required 60 days’ notice, while the most popular notice for low net funds was 45 days. This difference in liquidity may partially be attributed to the variations in directional and low net funds’ holding periods for long positions.

Please reach out to your Jefferies contact for more information on any of the topics above.

Interesting Service Provider Reads: Highlighting Topical Content from Industry Leaders

ACA/NSCP – 2024 AI Benchmarking Survey Results

Akin Gump – Nasdaq Diversity Rule Deemed Unenforceable By 5th Circuit

Dynamo – Dynamo Software’s 2024 Hedge Fund Report

SRZ –REMINDER: SEC Short Position (Form SHO) Filing Deadline Fast Approaching

Jefferies Prime Services Contacts:

Mark Aldoroty

Head of Jefferies Prime Services

[email protected]

Barsam Lakani

Head of Sales for Prime Services

[email protected]

Ariel Deljanin

Business Consulting Services

[email protected]

Leor Shapiro

Head of Capital Intelligence

[email protected]

Eileen Cooney

Capital Introductions

[email protected]

1FactSet, performance data is through November 2024.

2HFR Q3 2024 Hedge Fund Report

3SOFR refers to the Secured Overnight Financing Rate, which is a broad measure of the cost of borrowing cash overnight collateralized by Treasury Securities.

4HFRI, performance data is through November 2024.

5Arcadian

DISCLAIMER

THIS MESSAGE CONTAINS INSUFFICIENT INFORMATION TO MAKE AN INVESTMENT DECISION.

This is not a product of Jefferies’ Research Department, and it should not be regarded as research or a research report. This material is a product of Jefferies Equity Sales and Trading department. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the individual author and may differ from the views and opinions expressed by the Firm’s Research Department or other departments or divisions of the Firm and its affiliates. Jefferies may trade or make markets for its own account on a principal basis in the securities referenced in this communication. Jefferies may engage in securities transactions that are inconsistent with this communication and may have long or short positions in such securities.

The information and any opinions contained herein are as of the date of this material and the Firm does not undertake any obligation to update them. All market prices, data and other information are not warranted as to the completeness or accuracy and are subject to change without notice. In preparing this material, the Firm has relied on information provided by third parties and has not independently verified such information. Past performance is not indicative of future results, and no representation or warranty, express or implied, is made regarding future performance. The Firm is not a registered investment adviser and is not providing investment advice through this material. This material does not take into account individual client circumstances, objectives, or needs and is not intended as a recommendation to particular clients. Securities, financial instruments, products or strategies mentioned in this material may not be suitable for all investors. Jefferies is not acting as a representative, agent, promoter, marketer, endorser, underwriter or placement agent for any investment adviser or offering discussed in this material. Jefferies does not in any way endorse, approve, support or recommend any investment discussed or presented in this material and through these materials is not acting as an agent, promoter, marketer, solicitor or underwriter for any such product or investment. Jefferies does not provide tax advice. As such, any information contained in Equity Sales and Trading department communications relating to tax matters were neither written nor intended by Jefferies to be used for tax reporting purposes. Recipients should seek tax advice based on their particular circumstances from an independent tax advisor. In reaching a determination as to the appropriateness of any proposed transaction or strategy, clients should undertake a thorough independent review of the legal, regulatory, credit, accounting and economic consequences of such transaction in relation to their particular circumstances and make their own independent decisions.

© 2024 Jefferies LLC

Clients First-Always SM Jefferies.com

Japan’s GX Plan: Is the World’s Most Ambitious Energy Transition Being Overlooked?

Nearly two years ago, Japan unveiled its Green Transformation Policy (GX), a $1 trillion plan to dramatically reduce emissions over the next decade. This initiative represents nearly three times the annual GDP investment percentage of the U.S. Inflation Reduction Act — and it aims to catalyze climate tech innovation in the world’s fourth-largest economy.

Surprisingly, GX has largely flown under the radar of institutional investors. Of the 400+ investors Jefferies recently engaged across the U.S. and Europe, only three were familiar with the plan.

Japan’s GX spans all areas of climate finance: carbon levies, emissions trading, transition bonds, and more. Given its scale — and the Japanese stock market’s outperformance over the past three years — Jefferies views it as a defining transition investment theme for the next decade.

In the coming weeks, Jefferies will outline GX’s core policies, investment tailwinds, and strategies for addressing Japan’s highest-emitting sectors. First, here are the eight things every climate investor needs to know about Japan and its approach to decarbonization.

- Japan is the world’s fourth-largest economy — at least. According to the International Monetary Fund, Japan’s $4.07 trillion GDP ranks 4th globally, behind the US, China, and Germany. Some calculations place it in 3rd.

- Japan is one of the world’s leading emitters. The International Energy Agency reports that Japan accounts for 2.9% of global emissions, the 5th highest globally. Since 2000, Japan’s emissions have dropped 15%, and its emissions per capita rank 23rd worldwide — compared to China, which ranks 25th.

Despite being one of the world’s leading emitters, Japan was just 2% of the total $1.8trn spent on energy transition in 2023.

- Japan’s GX Policy represents a larger percentage of its GDP than the Inflation Reduction Act does for the US. In a recent note, Jefferies encouraged investors to look beyond the US, especially as the IRA may not survive in its current form. It is also arguably more impactful on Japan’s economy than the IRA is on the US. Annual public investment under GX is 0.33% of GDP, compared to the IRA’s 0.13%. Factoring in both public and private investments, GX accounts for 2.47% of GDP, while the IRA is 1.04%.

- Japan has set several new climate targets, including a goal for nuclear power to make up 20% of the country’s energy mix by 2040. To achieve these ambitious goals, Japan is tapping into all areas of climate finance, including bond issuance, R&D investments, subsidies, carbon levies, and an emissions trading scheme.

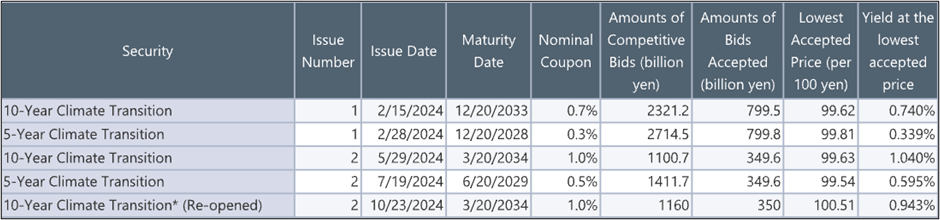

- Japan is issuing transition bonds as part of its GX vision. Japan will issue 20 trillion JPY (~$144B USD) of sovereign climate transition bonds over the next several years. In February 2024, the 10-Year Climate Transition Bond was priced at a 0.74% yield, slightly below regular Japanese 10-year government bonds at 0.755%.

In 2024, Japan issued ¥2.65 trillion (~$17B) across 5 bond auctions. The first bond auction of 2025 is scheduled for January 29.

- Japan plans to impose a carbon levy targeting fossil fuel importers. This levy will gradually increase over time, with the proceeds allocated to repaying the principal and interest of the GX Transition Bonds. Notably, Japan currently accounts for 14% of global coal imports.

- Japan’s GX League is trialing the emissions trading scheme (ETS) for high-emission sectors. Introduced in 2023, it started with voluntary participation from the GX League — a group of 747 companies accounting for >50% of Japan’s emissions. From 2026 onward, the ETS will be mandatory.

- Japan is betting on R&D to drive a carbon-neutral future. Unlike the subsidy-heavy U.S. IRA, Japan’s GX policy focuses on directly supporting R&D through the Green Innovation Fund, which is supporting innovation at the country’s leading companies. In February 2024, 55% of bond auction proceeds were allocated to R&D initiatives.

Many of the key elements of Japan’s GX Policy are still taking shape, but there’s no question this plan merits investors’ attention. Jefferies’ team will continue to monitor the decarbonization of one of the world’s leading economies — and the economic growth and innovation this strategy aims to ignite.

Follow along for more insights from Jefferies’ Sustainability and Transition Team on the Japan GX Plan and other important climate investing themes in the weeks ahead.

Ten Questions for the Energy Transition in 2025

It’s too soon to predict what 2025 will mean for the energy transition. Much depends on the incoming administration’s policies, the resolution of global conflicts, and the direction of emerging technologies. As S&P Global Commodity Insights wrote in their 2025 outlook, “there is more uncertainty in energy markets heading into a new year than any year since the pandemic.”

Jefferies’ Sustainability & Transition Team is entering 2025 with ten key questions, covering the challenges and opportunities shaping the global transition. While the team brings perspectives on these issues today, developments in policy, technology, and markets could lead to a range of outcomes in the year ahead.

- Is the energy transition a viable investment theme for equity investors?

Yes, despite the underperformance of clean energy equities (ICLN) relative to oil and gas (IEO). The energy transition is much bigger than the performance of solar and wind producers compared to traditional energy companies.

Jefferies compiled a list of approximately 1,000 public equities across 27 subsectors related to the energy transition, representing a combined market cap of $18 trillion. A detailed analysis of the broader universe tells a different story about the transition’s investability and performance. Expect further insights on this subject in 2025.

- Will Climate Tech 2.0 repeat Climate Tech 1.0?

The team remains cautious about the scaling challenges facing climate tech companies, often referred to as the “missing middle.” These companies, struggling to transition from pilots to larger-scale projects, face significant hurdles, particularly in securing capital.

Jefferies has identified over 1,000 promising climate tech firms—across energy storage, sustainable aviation fuels, green hydrogen, nuclear, and more—that need significant scaling-up capital. In a high-interest-rate environment with uncertain government funding, this could be a challenge.

On January 13, 2025, Jefferies will host a seminar featuring leaders in climate tech, including Decarbonization Partners, Spring Lane Capital, Sila Nanotechnologies, and Commonwealth Fusion Systems, to explore these issues and investment opportunities further.

- Will investors look outside the U.S. for opportunities in the transition?

Jefferies anticipates a more global approach to energy transition investments in 2025. While U.S. investors have largely focused on the Inflation Reduction Act since its passage, significant decarbonization initiatives in countries like Japan, China, India, UAE, Saudi Arabia, and Brazil have been overlooked.

The firm expects global programs such as Japan’s GX Plan to gain investor attention as U.S. enthusiasm slows during a political transition. Jefferies sees these international markets as rich with opportunities in specific transition sectors.

- Is 2025 finally the year of climate adaptation?

Climate adaptation is a multi-trillion-dollar investment opportunity as economies worldwide contend with increasingly extreme weather. Data from the EU’s Copernicus Climate Change Service indicates that 2024 will be the hottest year on record, marking the first time global temperatures exceed 1.5°C above pre-industrial levels.

This year, Jefferies has highlighted investable themes like heat resilience, urban climate adaptation, and water management, offering stock ideas to address these challenges. The firm hopes to see more investment vehicles developed in public markets to support these critical areas.

- How will the carbon removal industry evolve?

Jefferies maintains long-term confidence in the carbon removal industry due to its necessity in reducing atmospheric CO₂ levels and its support from major governments and tech companies like Microsoft. However, the industry is going through transition, and Jefferies anticipates industry consolidation among the 800+ carbon removal companies currently operating.

Jefferies is producing a 15-part series, “How to Build a Carbon Removal Company,” featuring leaders from Direct Air Capture, Biochar, and Marine CDR, offering insights into where the sector is headed in 2025.

- How will companies commercialize sustainability?

Outside of the energy transition, companies across sectors are seeking to commercialize the sustainability megatrend.

Jefferies has developed a 10-part framework for how businesses can commercialize sustainability through capital raising, M&A, joint ventures, carbon markets, regulatory incentives, and more. Data from 1H24 showed sustainable debt surpassing $5 trillion since 2006, while green M&A activity continues to grow by both value and volume.

As companies move from “awareness-building” to executing sustainable strategies, Jefferies will use its framework to track developments and identify best practices across industries.

- Will AI agents change the labor market?

Jefferies has focused on human capital issues for nearly four years, and in 2025, artificial intelligence will be the firm’s singular focus.

Jefferies expects AI agents to be a transformative force in the labor market in 2025. These software programs, capable of independently performing tasks to achieve human-set goals, are being developed by companies like Salesforce, OpenAI, and Microsoft.

AI agents are already enhancing workflows, such as Salesforce’s Agentforce tools for sales and customer service. McKinsey estimates that generative AI could create over $2.6 trillion in annual value, with AI agents driving much of this impact.

- Which Republican Party becomes dominant: free market or populist?

Jefferies sees growing tension within the Republican Party between its traditional free-market faction and an increasingly influential populist wing. While the free-market camp champions deregulation and lower taxes, the populist side emphasizes trade protections, anti-Big Tech sentiment, and pro-worker policies.

How these factions influence the party’s economic agenda—particularly under the incoming administration—will shape policy debates around tariffs, unionization, and taxes in 2025.

- Will deregulation succeed and could it accelerate the energy transition in the US?

Jefferies is optimistic about the success of a deregulation agenda, including the Department of Government Efficiency (DOGE). In particular, the firm is monitoring deregulation’s potential to advance U.S. infrastructure projects critical to the energy transition. Proposed reforms to the National Environmental Protection Act (NEPA) could streamline permitting for grid infrastructure, nuclear projects, and utility-scale solar.

The firm will closely monitor developments under the incoming administration’s deregulation and government restructuring initiatives, which could provide bipartisan momentum.

- Will there be a global peace dividend in 2025?

2024 was a violent year. The ACLED’s Conflict Index shows global conflicts doubling over the past five years, spanning 50 countries.

Although most analysts expect extended global conflict, Jefferies believes the new administration could accelerate resolutions in Ukraine, the Middle East, and possibly China. A “peace dividend”—economic benefits from reduced defense spending—could follow, mirroring similar trends from the 1990s.

Jefferies plans to study the investment implications of such a shift, exploring opportunities that could emerge if global conflicts de-escalate in 2025.

What Energy Transition Investors See in Trump’s Policy Agenda

It’s been two weeks since the 2024 election, where the presidency and 468 congressional seats were contested. As of last Wednesday, the results are official: the GOP will hold a trifecta under President-elect Trump.

While the party’s agenda is still taking shape, one thing is clear—its policies will diverge from the Biden White House and its Democratic allies.

Jefferies’ Sustainability & Transition Team spent the past two weeks engaging over two thousand investors and companies on the implications of the election for global investment, the energy transition, and sustainability. Here are eight takeaways from those discussions.

- Which Republican Party Will Prevail?

Populism has taken root in the Republican Party. President Trump made grains across nearly every major demographic, and he performed exceptionally well in working-class communities.

Within the party, the team sees a growing divide between two camps:

- Traditional Republican Orthodoxy: Focused on deregulation and tax cuts.

- Populist Economics: Focused on protecting workers via tariffs; supportive of antitrust measures and skeptical of big tech; and supportive of government investment in key sectors.

The world is closely monitoring President Trump’s appointments to gauge the party’s trajectory, as the investment implications could vary significantly depending on which philosophy takes precedence.

- The Return of Industrial Policy & Tariffs

For years, industrial policy fell out of favor as a tool for promoting domestic industries and driving growth in developed markets. Recently, there’s been a shift. In 2023, more than 2,500 new industrial policy measures were implemented globally, ranging from tariffs to subsidies and state-directed financing.

The Trump administration is expected to lean heavily on industrial policy to boost U.S. competitiveness. Tariffs will likely take center stage, alongside continued support for key sectors like defense and energy. The campaign has also floated ideas such as creating a sovereign wealth fund to support U.S. industries.

Investors will need to integrate these policies into their strategies.

- Brace for Deregulation

Jefferies has tracked deregulation closely for months (see here, here, and here), anticipating a significant shift in the event of a Trump victory.

Now, there are plans for a new Department of Government Efficiency (DOGE), with Elon Musk and Vivek Ramaswamy at the help. Musk hopes to cut $2 trillion from the federal budget. Throughout the campaign, Trump regularly called for reducing the administrative state and pursuing widespread deregulation.

The specifics of this agenda—and its feasibility—remain uncertain. However, the potential impact on investors extends far beyond ESG and climate. Companies and investors should take a hard look at existing regulations, particularly those affecting competition, as many could be targeted for overhaul.

- Tax Cuts & Tariffs: Will Trump’s Policies Be Inflationary?

2025 will be a year of tax reform, with the Tax Cuts and Jobs Act (TCJA) expiring at the end of the year. Proposals for deficit-funded tax cuts and a high debt-to-GDP ratio have sparked bond market concerns over long-term (10-year) rates.

Since both the federal government and many companies often borrow at 10-year+ rates, changes in these rates over the next four years will heavily influence the federal deficit and corporate investment plans.

- The IRA Will Not Survive in Its Current Form

Heading into the election, conventional wisdom held that the Inflation Reduction Act (IRA) wouldn’t be repealed, given that 80% of its funds were directed to Republican districts. In September, Jefferies flagged potential downside risks to this assumption, and in October 2023, noted that the IRA could fall short of its goals unless key structural issues—like permitting—were addressed.

It’s now clear that significant efforts will be made to amend the IRA. Even without a full repeal, the incoming administration could pursue administrative actions that would effectively achieve the same outcomes as repealing the bill.

- The U.S. Energy Transition: Not All Is Lost

Several areas of the energy transition are poised for growth under a Trump presidency, whether due to federal indifference, alignment with favored industries, or state-level initiatives. Despite policy uncertainty and a potential shift in direction, the U.S. remains a highly attractive region for energy transition investments.

Investors see the most opportunity in the following sectors over the next four years:

- Natural Gas

- Carbon Capture & Sequestration

- Critical Minerals

- Transmission Reform (State & Federal)

- Grid-Enhancing Technologies (e.g., Dynamic Line Rating, Advanced Distribution Management Systems)

- Nuclear

- Geothermal

- Biofuels

Executives consistently highlight favorable capital and regulatory environments, a skilled labor force, and access to low-cost feedstocks (e.g., natural gas) as reasons the U.S. stands out, regardless of federal policy. Jefferies anticipates that specific areas of the transition will gain traction based on strong unit economics, rather than relying heavily on public subsidies.

- Look Beyond the U.S. on Energy Transition

Although the U.S. may pull back from global climate initiatives, the rest of the world will press ahead. China and the EU27 lead the world in real-economy capital formation for low-carbon technologies. 80% of the global population lives in net importers of fossil fuels, so the incentive to decarbonize will persist.

One unintended consequence of the Inflation Reduction Act (IRA) is that it has diverted investor attention away from decarbonization opportunities outside the U.S. For instance, Japan’s Green Transformation (GX) Plan—a ¥150 trillion initiative to decarbonize its economy—offers significant investment opportunities but has largely been overlooked.

Investors should broaden their focus to include other major policy programs that are shaping global decarbonization efforts.

- Will the U.S. Try to Compete with China on Decarbonization?

The U.S. must decide whether competing with China and other nations on climate and the energy transition fits into its broader Great Power Competition strategy.

The Inflation Reduction Act (IRA), CHIPS Act, and Bipartisan Infrastructure Law (BIL) were designed to position the U.S. as a leader in key areas like AI, semiconductors, biotech, and future energy systems. Significant changes or rollbacks to these initiatives could risk ceding ground in one or more of these strategic sectors.

++

Policy expectations for the next four years will evolve as President-elect Trump’s statements and appointments unfold in the coming months. For now, investors are preparing for a regulatory and investment landscape that contrasts sharply with the one shaped by the Biden administration.

For ongoing insights on the energy transition, climate investment, and related policy, stay connected with Jefferies’ Sustainability & Transition Team.

How Quickly Is Climate Change Accelerating? It Depends How You Look At It

For years, the pace and scale of the global energy transition have been uncertain. Significant progress has been made in areas like solar capacity, electric vehicles, and battery storage, but new challenges continue to surface: aging grid infrastructure, high inflation, and surging power demand.

More recently, another layer of uncertainty has emerged—the pace of climate change itself. The acceleration of global warming is often used as a metric for assessing climate risks, but scientists are increasingly debating its implications. These debates raise questions about how quickly the climate is changing amid an uneven global transition.

Jefferies’ Sustainability & Transition Team recently sat down with Pierre Friedlingstein, Professor and Chair in Mathematical Modeling of the Climate System at the University of Exeter. Together, they explored what the latest data reveals about the trajectory of climate change—and whether net-zero efforts are up to the challenge.

Here are eight key takeaways from their discussion.

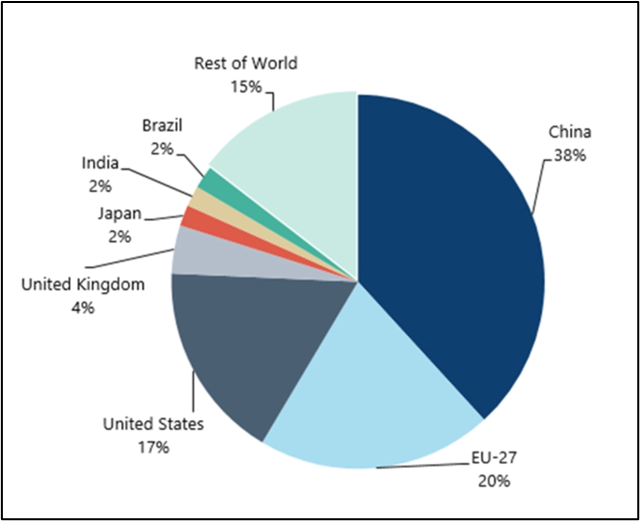

- Global fossil fuel emissions have quadrupled over the last 60 years, contributing to increased warming. Global emissions are around 37 billion tons of CO2 annually. Emissions have risen sharply since the 1970s, climbing from an average of 22 billion tons per year back then to nearly 40 billion tons per year in the last decade. China is the largest contributor, accounting for 31% of global emissions, followed by the U.S. at 14%, India at 8%, and the EU at 7%.

- Carbon sinks are still working to absorb CO2, but their efficiency is declining. Over the past 60 years, the ocean and land have more than doubled their capacity to absorb carbon, removing about 55% of global emissions. However, there are signs that these natural carbon absorbers may be becoming less efficient and slowing down.

- The amount of CO2 the world can emit while keeping global warming within specific limits—like 1.5°C or 2°C above pre-industrial levels—is finite. There’s a clear, direct link between total CO2 emissions and temperature rise, supported by all major climate models. At the current rate of emissions, we have roughly 7 years left to stay within 1.5°C, 15 years for 1.7°C, and 28 years for 2°C.

- Warming may be accelerating, but the rate of acceleration varies depending on the baseline and time period analyzed. Research shows a steady rise in warming from the 1970s to 2010, with a faster increase after 2010. However, the strength of this argument varies. The acceleration is more noticeable when comparing recent years to the late 19th and 20th centuries but less convincing over shorter time frames.

- The reduction in sulfate aerosol emissions may also be contributing to faster warming, as these particles have a cooling effect. Regulations to limit aerosol emissions, driven by their harmful health impacts, have led to fewer aerosols in the atmosphere. With less cooling from aerosols, warming could be accelerating.

- Climate scientists debate whether warming acceleration is a meaningful metric. The perceived rate and direction of acceleration depend on the timescales and natural variability considered. It’s important to focus on metrics like the remaining carbon budget, current emission rates, and the efficiency of natural carbon sinks in absorbing CO2.

- There is an increasing need for carbon removals given the limited carbon budget available. To limit future warming, CO2 must be removed faster than natural sinks can manage. Approaches like Direct Air Capture (DAC) and Bioenergy with Carbon Capture and Storage (BECCS) show potential for effectively removing carbon from the atmosphere.

- Whether the rate of warming continues to rise or not will depend on our ability to mitigate emissions. As long as emissions continue to rise, climate change will continue with increasing impacts and need for adaptation.

Jefferies’ conversation with Professor Friedlingstein underscores the central challenge of the global transition: despite advances in understanding and addressing climate change, the window for effective action is narrowing. Without faster, more ambitious efforts, critical warming thresholds could be exceeded within decades.

At the same time, the professor’s insights reveal the complexity of the climate conversation. Metrics like warming acceleration are context-dependent, and different indicators can yield varying conclusions. Understanding progress and setbacks in the global transition requires openness to evolving data and a broad range of climate metrics.

For more insights on climate and the energy transition, follow along with Jefferies’ Sustainability & Transition Team.

How Workforce Dynamics in Japan Will Shape the Country’s Economic Future

Japan is now positioned as one of the world’s most promising equity markets through 2030. While foreign investment has historically played a small role in the country’s economy, this opportunity has sparked a surge of Western capital. Berkshire Hathaway, for example, increased its stake in five Japanese trading houses by 70%.

Last fall, Jefferies’ Equity Research Team published From Lost Decade to Golden Age: A New Paradigm for Japan Inc., highlighting investment opportunities emerging from Japan’s ambitious economic reforms.

For new entrants, understanding Japan’s unique economic and professional landscape is essential. Jefferies’ latest Human Capital Survey, which compares attitudes in the Japanese labor force to those in the U.S. and U.K., provides valuable insights.

Here’s what the survey revealed about Japan’s labor force in 2024—and what it means for investors.

- Quitting: Just 22% of Japanese respondents are considering quitting in the next six months, compared to 42% in the UK and 45% in the U.S. This aligns with research showing that Japan’s HR policies—steep seniority-earning profiles, extensive fringe benefits, participatory management, and reluctance to hire experienced workers from other firms—result in low turnover rates..

- Remote Work: 28% of Japanese respondents prefer to work five days in the office, compared to 22% in the U.S. and 14% in the UK. Additionally, 56% of full-time employees in Japan are required to work in the office five days a week, a higher percentage than in both the U.S. and UK.

- Four-Day Workweek: Only 69% of Japanese employees support a four-day workweek, compared to 87% in the U.S. and UK. Among the 63,000 Panasonic Holdings employees eligible for a four-day workweek pilot, only 150 opted in.

- Burnout: Just 31% of Japanese employees report experiencing burnout, compared to over 70% in the U.S. and UK.

- Employee Recommendation: When asked how likely they would recommend their company as a workplace (on a 1-10 scale), 70% of Japanese workers rated it 0-6, and only 10% gave it a 9-10. In comparison, 31% of U.S. workers and 38% of UK workers gave a 0-6 rating. Japan’s employee Net Promoter Score remains deeply negative.

- ChatGPT Use: Just 52% of office workers in Japan have used ChatGPT, compared to 79% in the U.S. and 80% in the UK. Concerns about automation are also lower in Japan than in the other countries.

- Upskill & Reskill: Only 67% of Japanese workers would explore skill development due to concerns about automation, compared to 84% in the U.S. and 86% in the UK. Notably, 35% of U.S. respondents would consider higher education for reskilling, versus just 14% in Japan.

For years, Jefferies has analyzed the human capital strategies of American and European companies, finding a significant link to corporate performance (see Human Capital Stocks and Europe’s Human Capital Stocks). As investment opportunities in Japan expand, insights from this latest survey may reveal where opportunities and risks lie.

Overall, the survey reveals that Japanese employees are less likely to quit than their American and British counterparts, for a range of reasons. As a result, employee engagement—and its impact on productivity—is the most material issue for Japanese companies today.

While the U.S. SEC has been slow to require human capital disclosures, Japan is moving forward with mandatory reporting on key areas, including: (1) succession plans for critical roles, (2) management remuneration ratios, (3) director skills matrices, and (4) initiatives to promote women, foreign nationals, and mid-career hires into middle-management positions.

These measures signal a shift in corporate transparency, offering both new and seasoned investors insights into the workforce dynamics that will shape Japan’s economic future.

For continued insights on human capital management and more, stay connected to Jefferies’ Sustainability & Transition Team.

The OCFO Is Having a Moment–Where Does It Go From Here?

The Chief Financial Officer’s role once focused on core accounting operations like AR/AP and FP&A. Today, the Office of the CFO (OCFO) is the strategic hub of modern enterprises. It influences everything from HR and risk management to the deal desk.

This expanded role has sparked a wave of products aimed at optimizing the often-painful workflows that fall to CFOs. The new category is catching investors’ attention, with some viewing it as the next big disruption in enterprise software.

“Today, OCFO is as core as it gets. All our investments touch OCFO in some way,” said Jonathan Wulkan of HG Capital.

At Jefferies’ fourth annual Office of the CFO Summit, leaders from 75 companies and nearly 175 investors gathered to discuss key trends, opportunities, and challenges in this growing space.

This recap covers a panel of four private equity investors in the OCFO space:

- Peter Christodoulo, Francisco Partners

- Jonathan Wulkan, HG Capital

- Matthew Dorr, General Atlantic

- Andrew Ren, Permira

How Did OCFO Become a Focus for Investors?

The OCFO category is still new—just a few years ago, it wasn’t on the radar of entrepreneurs or investors. Mr. Christodoulo explained the category’s emergence, charting CFOs’ evolution from accounting to a broader, product-centric role.

“I first heard the term ‘OCFO’ five years ago,” he shared. “The CFO’s role used to be mostly focused on things like accounting, AR/AP, FP&A, and Treasury. But gradually, a CFO’s role has grown as areas like payroll have led into HR and areas like billing have led into subscription and consumption billing. Now, CFO roles are heavily intermingled with products. It’s almost similar to fintech 15 years ago.”

For investors, this shift signals opportunity. Because CFOs’ focus was historically narrower, centered on core accounting operations, much of the innovation in other areas of the enterprise is only now starting to influence their job functions. Manual processes and legacy solutions still dominate CFO workflows.

“The biggest tailwind for OCFO is that this category has traditionally been seen as being in the background. Now, the OCFO is one of the loudest voices in the room, and that brings bigger budgets and a need for better technologies,” Mr. Ren shared. “The category is really exciting.”

Software Investing Is Down–Is OCFO The Exception?

Private equity and venture capital investment in software declined 51% year-over-year in 2023, as high interest rates and declining public-market valuations buffeted investors. With a new rate cutting underway, Jefferies asked the panel about their outlook for OCFO investing in the second half of 2024.

The response was clear: they’re open for business.

In discussing the future of OCFO investing, panelists highlighted a trend familiar to enterprise software investors: the shift from point solutions to platforms. As the OCFO role expands to cover more diverse functions, investors are seeking products that support the full stack, rather than individual functions.

“(OCFO products) should track the movement of data and money from the customer journey through internal systems. We think that there are great partnership opportunities between front and back-office software tools and payments platforms. From the OCFO perspective, it’s one continuous journey.”

Does the Sector Face Headwinds?

From an investor perspective, the panelists pointed out a few headwinds facing OCFO.

- Mr. Wulkan noted the influx of new entrants into the market. What was once a nascent category is becoming increasingly crowded, with more competitive bidding.

- Mr. Christodoulo mentioned that, like most sectors, OCFO hasn’t been immune to the high-rate environment of recent years. Businesses have had to adjust their cost structures, and in some cases, growth has slowed.

Despite these challenges, the overall sentiment was that OCFO remains a fast-growing and exciting sector—one that’s really just getting started. For more insights on OCFO and its trajectory, check out Jefferies’ interview with Evan Osheroff, Managing Director for Software Investment Banking.