What We Learned from the Year Generative AI Went Mainstream

The Jefferies 2025 Private Growth Conference brought together hundreds of top bankers, investors, founders, and tech executives to discuss the sector’s key trends and developments. The insights below are drawn from interviews and panels with conference attendees.

In 2023, generative AI was already reshaping the business landscape, but some important questions remained. Chief among them: how would these technologies meaningfully impact businesses, given their unclear enterprise applications?

Today, that question is largely answered. If 2023 was the year of AI hype, 2024 was the year AI went mainstream.

Three-quarters of businesses now use AI in at least one function, and generative AI is projected to drive $1.1 trillion in revenue by 2028. Big Tech is expected to invest a record $300 billion in AI this year.

At Jefferies’ Private Growth Conference, sector leaders discussed the trajectory of AI adoption and how it’s shaping dealmaking in 2025.

Embedding AI Into Everyday Decision-Making

“The AI ecosystem is maturing exponentially,” said Raphael Bejarano, Co-Head of Global Investment Banking at Jefferies. “Every year is a period of exponential change. I think we’ve seen that with the companies at the Private Growth Conference — their monetization, their actual utility. We’re beginning to see the green shoots where adoption is really going to happen”.

One of the companies making AI easier to adopt is Sigma Computing, a cloud-native analytics platform that helps non-technical users work with complex data. By layering AI on top of traditional business intelligence workflows, Sigma is making data more accessible to everyday decision-makers.

“If you reduce it a little bit, what AI means for us is an access method,” said Mike Palmer, CEO of Sigma. “We talk a lot about making access to data simple. There are a billion and a half people with spreadsheets in the world, and we thought that was the lingua franca of business. But actually, the lingua franca of business is just language. So for us, AI is just another way to allow an average person to easily get an answer to a question [from data].”

The latest McKinsey survey on generative AI adoption found that companies that successfully integrate AI into their workflows are already seeing meaningful EBIT gains. While adoption varies by industry, most companies are at least using AI in marketing and sales, with plans to expand into other business functions.

That perspective was echoed by Mark Crane, a Partner at General Catalyst who has led several investments in applied AI. He described how AI is reaching every part of the business landscape: “Generative AI is everywhere. Every vertical has been touched by this and will be touched by this,” he said. “Public safety, shipping, healthcare — pick your favorite vertical.”

AI Is Already Moving the Top Line

One major topic at this year’s conference was how AI could reshape performance and growth expectations in the years ahead. With adoption now mainstream, when should investors expect to see impacts on company financials?

Gaurav Kittur, Global Co-Head of Internet Investment Banking at Jefferies, suggested that impact may come sooner than expected.

“I was just talking to a CFO . . . his business grew more in the last five days than it had in the past year, driven by an AI algorithm that just started to work,” Kittur said. “AI is transformative. We’re starting to see the impact on top lines, on revenue, on profitability.”

Ravi Mhatre, Founding Partner at Lightspeed Venture Partners, has observed similar trends. “We’re seeing it happen,” he said. “It’s more than just pockets. The thing that’s most attention-getting for us is the speed with which revenues in these enterprise sectors is starting to happen… Usually in enterprise it takes longer, but these technologies are solving real business problems, so adoption is happening very rapidly.”

The Private Growth Conference also featured several entrepreneurs who spoke directly to how AI is driving financial impact for their business.

Dakota Smith, President and Co-Founder of Hopper, noted the effect on operating costs: “[AI] lowered our cost of customer service by 70 percent,” he said. “And it actually increased customer satisfaction… because they get instant assistance.”

For Sellers, an AI Narrative Is No Longer Optional

AI is also having a growing impact on transaction activity. Much of this is being driven by strategic buyers, as two-thirds of business leaders plan to use M&A to strengthen their AI capabilities over the next year. Private equity is also active in AI-driven deals, as sponsors look for ways to apply AI to drive efficiency across their portfolio companies.

“Every seller right now — frankly, whether or not you’re a tech company — has to have an AI story,” said Jon Gegenheimer, Managing Director in Technology Investment Banking at Jefferies. Many buyers, he explained, are already evaluating targets based on their AI exposure: “What they want to understand is, net-net, is the target I’m looking at a beneficiary of AI, or is AI an antagonist?”

That perspective was echoed by Stefani Silverstein, Co-Head of Global TMT Investment Banking at Jefferies. “It is very much not just a buzzword anymore; it is the reality,” she said. “Whether [a company] has a solution for AI, is the solution for AI, or is at risk of disintermediation from AI — they need to have an answer”

She emphasized that buyers are pressing for clarity. “It’s relevant for almost every single deal,” she said. “Having a solution, a story around [AI] that can be articulated to investors, to the board, to the investment committee is critical. It’s really driving a lot of the activity, at the very least, the dialog”

Continuing Up the AI Adoption Curve

AI is already reshaping operations, performance, and deal activity, but many still believe we’re in the early innings.

“Most of us are not really using the full capacity [of AI],” said Cameron Lester, Co-Head of Global TMT Investment Banking at Jefferies. “We all can see there’s a Ferrari engine out there, but most of us are still driving much more modest cars.”

For companies and investors, the real work now lies in building the systems, talent, and discipline needed to put that power to use in a measurable way. And as this year’s conference showed, that effort is already in motion.

How AI is Transforming Cybersecurity

The cybersecurity sector is rapidly transforming, spurred by the transition from cloud-based to AI-native technologies and the urgency for governments to shore up national security vulnerabilities.

Jefferies Managing Director Tim Roepke believes some cybersecurity companies are so valuable – and critical to the technology ecosystem – that they are fundamentally shifting the deal landscape and “challenging traditional ideas of when to buy versus when to build.”

On the heels of Jefferies’ April Private Growth Conference – which featured several leading cybersecurity companies and hundreds of other investors and company leaders – we spoke with Tim Roepke to get his take on the current state of the cybersecurity sector.

Q: What will AI’s impact be on the cybersecurity sector?

Tim: AI could be the most significant technological paradigm shift we’ve seen, including the iPhone, Google search, social media, and the public cloud. It could outdo them all because it touches every person and every business.

Q: How do you secure these AI applications? Is it very different from software security in the past?

Tim: AI apps were not a part of IT stacks in the past, so new muscle memory is being created. Company leaders are asking themselves, “How will we use AI individually? How will we use it as a business? And ultimately, how do we secure it, so it doesn’t do bad things?”

They are also looking for tool consolidation. If a CTO has five cybersecurity problems, they don’t want five cybersecurity vendors. They want one that can handle most problems.

Businesses also want to prevent catastrophic scenarios that can snowball. Imagine a company creating an AI agent that knows customers’ bank accounts, blood types, and financial histories and can distribute that information to millions. They must ensure it is checked appropriately, secured inside a firewall, and monitored and managed.

Q: How are the upstart cybersecurity companies trying to define themselves, and how are incumbent cybersecurity companies trying to stay ahead?

Tim: Twenty years ago, there was a shift to cloud-native technology. That was moving our data from servers in our closets and basements to AWS or Microsoft Azure. Now, the data revolution associated with AI use-cases has created a shift in infrastructure requirements. There is a small group of businesses in terms of dollars of revenue, but they have immense value and go-to-market ability.

It will take a long time for a business of any scale to move from a cloud-native to an AI-native infrastructure. However, breakthrough startup cyber companies can now approach potential customers with a holistic offering. They can say, “We have a solution that prevents your AI from getting out of control, can protect you from traditional hackers, and can prevent North Korea from getting into your cloud.”

Q: How is cybersecurity technology with AI different from what has existed in the past?

Tim: AI-native cybersecurity companies tend to be very prescriptive and on offense. They find and neutralize the attackers or discover things that could happen to organizations months in advance, and act. They are out to find problems before they ever start.

Q: When transformational technology changes the landscape, what does that mean for deal-making?

Tim: It will lead to a lot of deal-making.These companiesare so critical and valuable that they challenge traditional ideas of when to buy versus when to build. Google purchased Wiz for $32 billion. Google could have tried to build something like it, but buying Wiz made sense even at that price.

The Future of Carbon Removal, According to the People Building It

In January, Jefferies’ Sustainability and Transition Team posedten key questions for the energy transition in 2025 — a year many investors expect to be more uncertain than any since the pandemic. Among those questions: How will the carbon removal industry evolve?

Jefferies has long been confident in carbon removal, given its fundamental role in reducing atmospheric CO₂ and strong backing from major governments and tech companies. But the industry is entering a period of transition, driven by concentrated demand, high costs, and wavering government support in a shifting political climate.

To better understand today’s challenges and opportunities, Jefferies hosted CEOs from fourteen leading carbon removal companies. Their perspectives offer a candid look at the sector’s key risks — and how winners could emerge from this moment of uncertainty.

This article previews CEOs in Carbon Removal: A Playbook Amidst Grave Uncertainty, a new report from Jefferies. For full insights from the Carbon Removal Event, consult the complete report.

How Do Executives Address the Key Uncertainties in Carbon Removal?

Jefferies sees three main sources of uncertainty in the carbon removal industry: (1) Concentrated Demand, (2) High Costs, and (3) Volatile Government Support.

The team raised these topics with carbon removal executives. Here’s how they responded:

- Concentration of Demand: Microsoft Now Accounts for 77 Percent of Total Carbon Removal Tons Purchased

The companies argue that demand remains strong, not just from tech, but also from sectors like financials, consumer goods, industrials, and airlines. They note that Chinese tech companies are beginning to show interest in carbon dioxide removal as well. Executives expect demand to grow further as both voluntary carbon and compliance markets open up. They also point out that companies purchasing carbon removal credits early will be “first in line” when costs drop and supply tightens. Finally, they report that since Trump’s victory, they have not seen any slowdown in demand for carbon removal credits.

Still, sector leaders are mindful that Microsoft now accounts for 77 percent of total durable carbon removal purchased to date, with 93 percent of their portfolio focused on BECCS (bioenergy with carbon capture and storage). This concentration raises concerns about the industry’s early dependence on a single corporate buyer.

- High Costs: Carbon Removal Credits Are Exorbitantly Expensive

Most carbon removal companies face specific cost bottlenecks. For direct air capture (DAC), energy costs are a major hurdle. For soil carbon, enhanced rock weathering (ERW), and other approaches, the bigger challenge often lies in MRV — measurement, reporting, and verification. MRV accounts for more than half the costs for ERW companies. At Charm Industrial, which uses bio-oil injection, lab testing for MRV costs about $200 per ton, but because their data is stable, the CEO expects they can cut 90% of those costs by moving to less frequent testing.

Alternative revenue streams can also help offset costs. Equatic’s green hydrogen sales, priced around $3 per kilogram, help bring their net carbon removal cost to well below $100 per ton. Capture6 creates multiple revenue streams by managing brine, producing fresh water, and capturing carbon through their DAC solution — all of which use the same units of energy.

- Volatile Government Support: Will the Trump Administration Kill the Industry?

Government support has been critical for carbon removal companies, with U.S. leadership playing an especially important role. Mote Hydrogen, for example, received a substantial grant from a U.S. Hydrogen Hub, and Climeworks was selected for up to $625 million in funding from the Department of Energy. Climeworks cited the U.S. as a leader in carbon removal but also pointed to Canada’s investment tax credit, a memorandum of understanding with Saudi Arabia, and early moves by several Asian governments. Equatic has received ARPA-E funding and a Department of Energy award, along with a partnership from the Singapore government.

Recently, the Trump Administration has paused federal funding and laid off federal employees who worked on carbon removal. The CEO of Charm Industrial noted that permitting remains a bigger obstacle than economics for carbon removal companies, and suggested that if permitting reform advances under Trump, a pullback in incentives may not be as significant a headwind as some expect. CEOs also noted that venture capital investors are taking a “wait and see” approach, a trend that has continued since the event.

Jefferies continues to view carbon removal as a bipartisan priority, with ongoing support through programs like the 45Q tax credit and DAC hubs.

A Shakeout That Could Strengthen the Industry

Jefferies’ Sustainability & Transition Team wrapped up the event with a definitive message: don’t give up on carbon dioxide removal.

The team projects that a slower energy transition could drive even greater demand for carbon dioxide removal — and that Trump’s presidency may not be as negative for the industry as many expect.

There are also now more than ten proven carbon removal technologies, each with different characteristics, costs, and co-benefits; it’s not just about direct air capture. And there are practical ways to reduce costs, including through economies of scale, alternative revenue streams, and streamlining MRV processes.

Many industry executives believe a shakeout among carbon removal companies will ultimately sharpen the industry’s focus on quality, credibility, and scalability at a reasonable cost. Buyers are taking a portfolio approach and avoiding heavy bets on any single technology. Investors in carbon removal are doing the same — diversifying across technologies, scale, geography, and registries to manage risk.

For deeper insights, consult the full Carbon Removal Event report and Jefferies’ 10-part expert series on the science behind leading carbon removal technologies, published in 2022.

How Can Tech Growth Companies Avoid Missing Their Moment?

Three years after the technology IPO market began declining, the IPO window appeared to be opening in the first few months of 2025. Despite market volatility and policy uncertainty, quality companies were poised to go public amid strong investor demand. However, the White House’s seismic April 2nd “Liberation Day” tariff announcement has, at minimum, delayed the IPO plans of several companies.

As investors sort through the impact of this radically altered trade environment, some of the world’s top technology investors and company leaders gathered for the Jefferies Private Growth Conference on April 22-23 in Santa Monica, CA. Ahead of the conference, we spoke with Evan Osheroff, Jefferies’ Managing Director of Software Investment Banking, to get his take on what’s shaping the technology market and where it’s headed.

Q: The White House tariff announcements caused immense short-term disruption. But do you expect it to fundamentally impact the trajectory of technology industry deal-making this year?

Evan: In addition to causing short-term disruption, it further cemented an environment of volatility, which is even more critical to overlay on the deal environment. As advisors and investors, we can’t control policy. All we can do is react to it. In the first few months of 2025, we already saw a dozen deals featuring venture-backed companies being acquired or going public at billion-dollar-plus valuations. So, the investor interest we expected to have coming into the year was undoubtedly there. I think it will still be there when the smoke clears a bit from the recent market volatility. We have companies in the IPO pipeline that are ready to go imminently and are just taking a week-by-week approach as to when to launch their offering.

In the meantime, investors need to stay focused on company fundamentals and recognize that when it comes to Washington, the only certainty for the next few years is likely to be uncertainty.

Companies, both public and private, venture-backed or in private equity portfolios, will have to accept volatility as the new norm. If people wait for things to calm down and become comfortable, there will be no M&A activity, IPOs, and limited capital returned to LPs. I don’t believe that is how this will play out, and the first few months of 2025 certainly suggest companies and investors are willing to transact despite the volatility.

Q: What is the current state of the IPO market, and what can we expect in the near future?

Evan: We are seeing some positive signs and increased activity, which we expect to continue. Companies are starting to select their underwriters and getting prepared, and interest in IPOs is definitely high. Business health is good, and valuations are more realistic than a few years ago. The problem recently has been a lack of supply. There have been too few IPOs, and people hesitate to be the first mover.

Many good companies are waiting in the background if they have a strong balance sheet. Clearly, some will choose to wait a bit longer as they assess the impact of tariffs and any knock-on effects they have across the market. Nonetheless, you have several notable fintech names ready to go. There are also several large software companies valued in the tens of billions that could go public any time they want, and we expect at least some to start sooner rather than later. Although there has been less activity in enterprise, a broad array of companies across various tech sectors are getting prepared for a potential IPO.

If these companies have a large cash pile and don’t have to do anything, they will not rush out. In the meantime, many companies are doing secondaries to provide liquidity to their employees and investors.

Our advice to companies considering an IPO is to worry less about a macro market window and more about your own window when you are growing fast, making the transition to profitability, and leaving plenty of runway for public investors to accrete value in their portfolios.

Q: Can delaying their IPOs create problems for these growth companies?

Evan: I don’t think enough people are talking about this. There are plenty of good reasons for private companies to do secondaries, but at a certain point, you are kicking the can down the road. Over time, these companies will have increasingly impatient employees eager to monetize their equity. They also run the risk that there won’t be enough value for public investors to capture by the time they do an IPO. If you do secondaries for too long, you may miss your IPO window and the great valuations – and payouts – that were once possible.

Q: What are your thoughts on AI as a near-term source of revenue and profitability?

Evan: AI presents a huge opportunity for growing revenue and scale. However, profitability may be years away.

I believe companies that deploy AI will create the greatest value. We are already seeing companies crossing $100 million in revenue in a matter of months, not years. Is that sustainable? We’ll see. Eventually, though, AI will generate substantial revenue and enormous value, uplifting pricing, capabilities, and competitiveness. Next up is the 10-person, $1 billion revenue company. That is not very far away from where we are today.

Q: Do you think people overestimate the magnitude or near-term payoff of the AI revolution?

Evan: AI, however you define it, will be infused into everything, including AI agents, foundational models, better analytics, and enhanced search capabilities. I have a firm conviction that it will change and transform everything.

One of these AI companies hoping to do an IPO will be the next Netscape, and another will be the next Google. But no one knows which one it will be.

Q: The arrival of DeepSeek in the public mind was a big moment. It wiped out a significant portion of the market capitalization of major companies that day. Is it having a lasting impact on software companies?

Evan: It’s less about DeepSeek specifically having an impact on software companies and more about showing what is possible in a world of open source and how critical that is to innovation. DeepSeek effectively showed that models can be copied, and innovation can be applied to achieve spectacular results. That is why companies are moving so fast and raising so much money. We are still at the beginning of the innovation curve, and that is exciting.

Jefferies Business Consulting and Strategic Content Newsletter – Q1 Recap

Jack-of-all-Reads: Jefferies Business Consulting and Strategic Content Newsletter

Q1 Recap

Spotlight on Jefferies Content and Events:

Welcome to Jefferies. Margaret Davidge-Pitts, Brad Lutzer, and Fabio Mariani Join to Enhance Our Prime Brokerage Offering for Clients: Please welcome Margaret Davidge-Pitts, who joins as our Head of Asia Capital Introduction, based in Hong Kong, Brad Lutzer, who joins our Prime Services Sales and Origination Team, based in New York, and Fabio Mariani who joins our Securities Finance team as Head of Americas Prime Distribution, based in New York. The addition of Brad, Fabio, and Margaret will broaden our reach with key equity financing clients and bolster our overall client strategy across the globe.

- Margaret joins us from Goldman Sachs, bringing nearly 20 years of experience and expertise in helping hedge funds launch, scale and raise capital in Asia, including in markets such as South Korea, Taiwan, Thailand, Australia and New Zealand.

- Brad also brings nearly 20 years of industry experience and relationships across a broad range of hedge funds and asset managers; he joins from UBS.

- Fabio brings nearly 30 years of experience and expertise in the Prime Brokerage Industry specializing in Hedge Fund Distribution for Securities Finance. He joins from TD Securities and has spent over 25 years at Goldman Sachs.

- Recent Movers: Recently, our Prime Services Sales team has relocated two of our key members to expand our global presence: Ed Barnes has moved from NYC to London and Grace Qiu has transitioned from NYC to Hong Kong. These strategic moves aim to enhance our business and strengthen our offerings.

Digital Footprint of Multi Manager Funds: This piece dives into the online presence of multi-manager funds, examining how they strategically brand themselves in the digital landscape. It explores how multi-manager funds leverage digital tools to enhance their brand and communication with investors. Please reach out to your coverage for a copy.

Initiation Report: Israel Economic and Strategic Outlook 2025: Israel has been embroiled in prolonged warfare on multiple fronts since the October 7th 2023 tragedy. There are optimistic signs that Israel’s geopolitical reality could greatly improve. Click here for full PDF.

AI Agents—The Key Human Capital Question in 2025: Insights from our 3.5 years of studying human capital investing have led us to focus on the central investment human capital theme of 2025: AI agents. This note outlines what AI agents are, recent updates from MSFT and CRM, and practical steps for investors to analyze how companies integrate AI into the workforce. Click here for full report.

Industry Insights

Access Funds & Why They Have Proliferated: Access firms might have had a stigma to them, like SMA’s once did, however, the success of private wealth channels highlighted their potential for fundraising and many groups are now working with or in dialogue with these firms. These platforms leveraged fintech to streamline operational processes, reducing headaches associated with feeder funds, such as redemption docs and annual audits. This model now provides financial advisors and their HNW and RIA clients access to high-quality alternative managers across hedge funds, private equity, REITs, and evergreen vehicles, albeit at a higher cost due to streamlined operations.Main concerns for managers include:

- Failure to Raise Capital: Success often depends on brand recognition. Less-known managers may struggle to raise capital as access funds are not placement agents. If unsuccessful, managers face penalties, typically paying one year of management fees.

- New Players: Managers must ensure access fund providers can handle client reporting for QPs and AIs. Engaging a knowledgeable lawyer is crucial to protect the manager and ensure compliance.

- Liquidity Mismatch: Hedge funds may have annual liquidity, lockups, and gates, while access funds might be more liquid. This mismatch can create challenges, especially with illiquid investments. A good lawyer can negotiate liquidity arrangements and create processes for mass redemptions.

SMAs and Due Diligence: With the rise of separately managed accounts (SMAs), understanding investor perspectives on transparency and due diligence is crucial. A study by Investment Advisor Association reveals that SMAs collectively manage over $1.5 trillion in assets, with an annual growth rate of 8% over the past five years.5 Key points to consider include:

- Multi-ODD: Multi-Manager funds are increasingly investing via SMAs. Investors may focus diligence on multi-strategy managers if SMA managers rely on their services. However, some conduct ODD on both the SMA and commingled fund, reviewing track records, performance, AUM, staffing, and fund specifics.

- Transparency: SMAs offer increased transparency, but managers should address potential risks in SMA agreements. A study by Squarepoint encourages managers to ask about internal trading strategies, shadow alpha declarations, reasons for Pre-EOD transparency, willingness to adopt confidential information language, and gather references from other PMs to mitigate risks arising from this transparency. 6

- Ring-Fenced SMAs: Ring-fencing is typically non-negotiable and built into the platform by asset owners. While it provides a form of separation, sleeves can still be affected by other managers’ portfolios. Some SMA platforms incorporate ring-fencing, often structured as segregated portfolio companies or series LP/LLCs, preferred for asset separation. Combining sleeves can offer better margining, and managers are compensated for their performance regardless of others’ outcomes.

Midtown Office Reports: Multiple brokers reported that 2024 saw the highest yearly leasing volume in NYC since pre-pandemic levels, marking a significant increase from 2023. Despite this, rents have not seen much increase as vacancy rates remain higher than pre-pandemic levels. This trend signals a substantial return to office spaces, with new businesses also seeking short-term options during their launch phase.

- Coworking Space and Short Term Rentals: Sublease terms range from 1 to 2 years, with even 1-year leases being rare. Landlords typically avoid leases shorter than a year due to transaction costs, and the length of the signing process. For coworking spaces in Midtown, many managers will consider options like Studio or Industrious, or go directly through major landlords like Tishman or SL Green.

Service Provider Trends: Emerging trends in the service provider community are shaping various verticals.

- AI and Compliance: There are growing offerings around AI and expert network calls, along with the implementation of AI policies. Cyber compliance is also seeing more attention, with many CCOs updating policies to include AI and data usage clauses.

- Middle Office Services: Outsourcing services for data, operations, treasury, settlements, and collateral has been gaining popularity, especially among new launches with an in-house CFO. This trend helps address the ongoing struggle to find junior talent to support senior staff.

- Trends around Technology: There’s a rise in “lite” offerings as many more managers are increasingly focusing on technological developments showing interest in software earlier in their life cycles with limited access to capital.

Regulatory Corner

Korea Update: As you may be aware, The Korean market will lift its short sale ban on March 31, 2025. In advance of this, the Financial Services Commission in South Korea and related organizations have announced guidelines and control measures designed to eradicate naked short selling of stocks traded on the Korean Stock Exchange. Jefferies’ offering of Equity Swaps product in Korea will continue uninterrupted, and our upgraded position management system will fully abide by the new rules.

- Global Offering: As part of Jefferies’s expanded global offering, we are pleased to share that we will be able to offer our equity swaps product in South Korea to facilitate short sales. Jefferies SWAP clients can synthetically short Korea equities again from this date.

- Pre-Borrow: Korea is a pre-borrow market, meaning borrow needs to be secured with Jefferies Financing desk before any short is executed. While the previous short sale universe was restricted to the KOSPI 150 and KOSDAQ 200 names, this is not the case now. All Korea equites are in scope (subject to certain exclusion names designated by the exchange (Offshore ETF / Synthetic ETF / ‘Overheated’ short sell names).

Proposed Increase in Endowment Tax: Policymakers close to President Trump are considering raising the tax rate on university endowments to combat the U.S.’s fiscal deficit. The 2017 TCJA introduced a 1.4% tax on endowments for universities with at least 500 students and assets exceeding $500,000 per student.1 Rep. Troy Nehls proposed the Endowment Tax Fairness Act to increase this tax to 21%, matching the federal corporate tax rate, while Rep. Mike V. Lawler suggested a 10% hike.2

- Impacts: Colleges argue higher taxes would reduce their ability to support financial aid, research, and faculty, impacting spend targets and asset allocation. Universities may be expected to adjust their portfolios, potentially increasing risk or exploring more tax-efficient strategies.

Enhanced Scrutiny on FCA’s ‘Name and Shame’ Proposal: The FCA’s “name and shame” plan requires early disclosure of investigations to increase transparency and deter misconduct.

- Outcomes: Hedge funds fear reputational damage and unnecessary investor withdrawals, noting that 2/3 of past FCA investigations ended without enforcement.3 Revised rules still concern hedge fund professionals, who worry it could deter business in the UK.4 AIMA recommends limiting disclosures to cases of immediate mass market harm or public knowledge. Investors should be aware of potential impacts on fund performance and market perception due to these disclosures.

Please reach out to your Jefferies contact for more information on any of the topics above.

Interesting Service Provider Reads: Highlighting Topical Content from Industry Leaders

ACA – SEC Marketing Rule FAQs for Gross and Net Performance of Extracted Performance

AIMA – Hedge Fund Confidence Index

Akin Gump – SEC Staff Says It’s OK to Just Be Gross

Carne – 2025 Change Research Report

Citco – Citco 2024 Middle Office Solutions Report – A Year in Review

FiSolve – Weekly News Digest: March 21, 2025

IQEQ – Roundup: SEC’s off-channel communication enforcement continues

SRZ – EDGAR Next: Preparing for the SEC’s Filing System Transition

Jefferies Prime Services Contacts:

Mark Aldoroty

Head of Jefferies Prime Services

[email protected]

Barsam Lakani

Head of Sales for Prime Services

[email protected]

Leor Shapiro

Head of Capital Intelligence

[email protected]

1Tax Foundation, New Efforts on Taxing Endowments Raise Questions on Neutrality and Revenue Collection

2Congressman Lawler Reintroduces the Endowment Accountability Act to Ensure Wealthy Universities Invest in Students

3Financial Times, FCA backtracks on plan to ‘name and shame’ probed companies

4Alternative Fund Insight

5Investment Advisor, Industry Snapshot 2024

6Squarepoint, Position Paper: Handling SMA Transparency with Responsibility

DISCLAIMER

THIS MESSAGE CONTAINS INSUFFICIENT INFORMATION TO MAKE AN INVESTMENT DECISION.

This is not a product of Jefferies’ Research Department, and it should not be regarded as research or a research report. This material is a product of Jefferies Equity Sales and Trading department. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the individual author and may differ from the views and opinions expressed by the Firm’s Research Department or other departments or divisions of the Firm and its affiliates. Jefferies may trade or make markets for its own account on a principal basis in the securities referenced in this communication. Jefferies may engage in securities transactions that are inconsistent with this communication and may have long or short positions in such securities.

The information and any opinions contained herein are as of the date of this material and the Firm does not undertake any obligation to update them. All market prices, data and other information are not warranted as to the completeness or accuracy and are subject to change without notice. In preparing this material, the Firm has relied on information provided by third parties and has not independently verified such information. Past performance is not indicative of future results, and no representation or warranty, express or implied, is made regarding future performance. The Firm is not a registered investment adviser and is not providing investment advice through this material. This material does not take into account individual client circumstances, objectives, or needs and is not intended as a recommendation to particular clients. Securities, financial instruments, products or strategies mentioned in this material may not be suitable for all investors. Jefferies is not acting as a representative, agent, promoter, marketer, endorser, underwriter or placement agent for any investment adviser or offering discussed in this material. Jefferies does not in any way endorse, approve, support or recommend any investment discussed or presented in this material and through these materials is not acting as an agent, promoter, marketer, solicitor or underwriter for any such product or investment. Jefferies does not provide tax advice. As such, any information contained in Equity Sales and Trading department communications relating to tax matters were neither written nor intended by Jefferies to be used for tax reporting purposes. Recipients should seek tax advice based on their particular circumstances from an independent tax advisor. In reaching a determination as to the appropriateness of any proposed transaction or strategy, clients should undertake a thorough independent review of the legal, regulatory, credit, accounting and economic consequences of such transaction in relation to their particular circumstances and make their own independent decisions.

© 2025 Jefferies LLC

Clients First-Always SM Jefferies.com

After a Record Run, Can India’s IPO Market Regain Momentum?

In 2024, 338 companies went public on the National Stock Exchange of India (NSE) and BSE, raising a record $21 billion. By year’s end, India was one of the world’s hottest IPO markets, with its volume matching the combined total of China and Hong Kong.

More recently, though, Indian public markets have lost steam. The Nifty 50 index, which tracks the country’s top-50 public companies, initially dipped on concerns over the Trump administration’s anticipated tariffs and continued to slide as more details emerged.

What does this mean for public offerings? It may be too soon to tell, but some investors view current IPO aftermarket performance as a warning sign. More new listings have struggled than succeeded in recent months.

Jibi Jacob, Head of Equity Capital Markets at Jefferies India, believes that broader market conditions—not IPO pricing or quality—are to blame.

“India’s market cap. has decreased from $5.5T to $3.7T, and IPOs feed on what is happening in secondary markets,” he said at a recent conference. “But if you look at the top 20 IPOs, mean returns are 25-28%. If pricing were wrong, returns would be more negative.”

Jefferies Insights caught up with Aashish Agarwal, the firm’s India Country Head, to discuss the country’s IPO pipeline. This follows his Q&A last fall, where he spoke about India’s growth story and the backlog of large companies eyeing public offerings.

Jefferies was recently recognized as India’s ‘Best Investment Bank’ by Global Finance.

India’s IPO Pipeline: Crowded but Stalled

Before analyzing the current market, it’s helpful to look back at recent trends in Indian public issuances, which, until November 2024, had ranked among the world’s most active.

In 2023 and 2024, Indian IPOs grew in number but even more in scale. Public issuances rose 22.6% from 2023, while fundraising volumes jumped 139%.

In 2023, small- and medium-sized enterprises led the IPO surge, nearly tripling new issuances from the year before. By 2024, larger companies entered the mix, and going into 2025, several of India’s unicorns were expected to go public.

Now, the outlook for large-cap IPOs is uncertain. No “mainboard IPOs”—listings from large, established companies—have launched for four consecutive weeks. New issuances have primarily come from the small and mid-cap segment.

“Though we have not seen sizable IPOs in the last few weeks, year to date nine companies got listed and cumulatively raised $1.8B. In the last two months or so, when the market has seen corrections, there are eight or nine issuers who have mandated banks for their potential listing with issue size greater than $1Bin the next 12 months,” Agarwal explained. “Since IPOs take 6-9 months for listing, being in the state of readiness is the key right now.”

A growing backlog of high-profile businesses has been cleared for public issuance but remains on the sidelines for now. So far, 34 companies have received approval to raise $4.8 billion this year, while another 55 are awaiting clearance for up to $11.4 billion, according to a leading Indian brokerage and asset management group cited by the Financial Times.

Has IPO Pricing Run Too Hot?

For two years, companies have capitalized on strong valuations in India’s public markets, which have become some of the most expensive globally by price-to-earnings multiples. The 2024 hot streak of IPOs added to the appeal. A study of 162 IPOs last year found that more than 82% traded higher after listing.

This stood in contrast to IPO markets in the U.S. and Europe, where new listings have struggled for years.

Some investors are asking if valuations have overheated. Reuters recently highlighted India’s largest IPO of 2024—a subsidiary of Korea’s Hyundai Motors. While the parent company trades at a 3.7x forward price-to-earnings multiple, its Indian subsidiary trades at 22x. Indian units of Japanese and European companies have seen similar valuation premiums.

Are 2025’s IPOs struggling in aftermarket trading due to inflated valuations, or is their performance simply mirroring broader market declines driven by tariff threats and other pressures?

“The two sizable IPOs of this year, Dr. Agarwal’s Health Care ($350 M) and Hexaware Technologies ($1B), have stood the test of recent market volatility. Both are above their issue prices currently,” Agarwal said. “We believe the aftermarket performance of 2024’s IPOs is currently driven by broad market performance and outlook.”

A Necessary Reset for Indian Markets

Some financial leaders see reason for optimism in India’s market performance, including Jefferies India’s Head of Research, Mahesh Nandurkar. In a recent appearance on CNBC India, he points to signs of stabilization in Indian benchmark indices and describes the recent downturn as a necessary reset.

“This much-needed market correction is now, I think, behind us,” he said. “Valuations are now down closer to long-term averages, and fundamentals are showing signs of improvement.”

His remarks come at a time of heightened volatility for U.S. public equities. Historically, turbulence in the U.S. has rippled into emerging markets—but this time could be different.

Nandurkar thinks the extended bull run in U.S. equities may have dampened investor appetite for emerging economies. Now, with uncertainty around tariffs and trade policy weighing on the U.S. economy, American investors may start looking elsewhere for returns. India could stand to benefit.

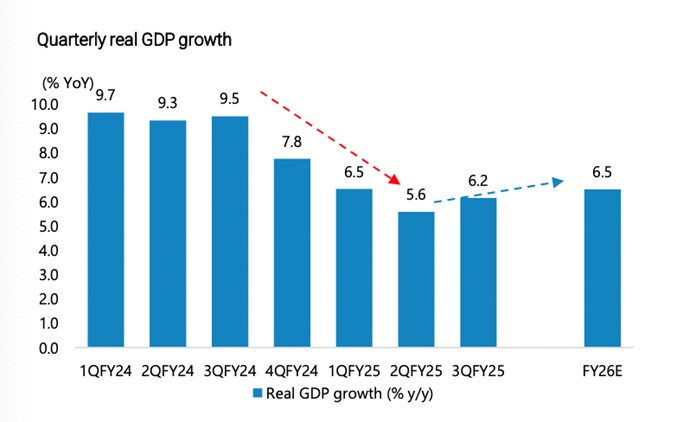

Source: MOSPI, CEA, Jefferies

Growth projections for the Indian economy reflect this. After the shallow slowdown of recent quarters, GDP growth is expected to rebound to 6.5% CAGR.

The panel cautioned that it’s too soon to call the trajectory of Indian public markets. But if the correction is truly in the rearview, it could set the stage for a stronger IPO pipeline.

Searching for Growth in Emerging Markets

As IPO activity lags in developed markets, investors are turning to emerging economies for opportunities. Indian public equities may be expensive, but they’ve delivered strong returns for years.

The question now is whether the recent IPO slowdown signals a deeper shift or just a temporary setback. With several high-profile companies still waiting to go public—and fresh positive signs for India’s economy—many eyes will be on India’s markets in the weeks ahead.

For more insights from Aashish Agarwal and Jefferies’ award-winning India team, read his Q&A on Jefferies Insights: What Will Drive India’s Growth for the Next 20 Years?

What the Global Political Shift Means for Energy

Just two months into the new U.S. presidential administration, the conversation—and regulatory framework—around energy is shifting dramatically. Yet global energy trends unfold along much different trajectories and timelines than those governing politics. According to Pete Bowden, Jefferies’ Global Head of Industrial, Energy & Infrastructure Investment Banking, this is why most energy investors and leaders with whom he speaks are moving with patience and deliberation.

This week, Pete and his team are host to several hundred senior leaders from the U.S. and globally at the Jefferies Energy and Power Summit in Houston. There, they are to discuss the most consequential trends shaping global energy markets. In advance of the gathering, we sat down with Pete to get his take on a few key questions likely to be on the minds of meeting attendees.

Q: What will the near-term impact of the energy regulatory changes from the Trump Administration be?

A: The changes may not be as seismic as some think.

The perception that everything would change the day Trump entered the Oval Office in January ignores the realities of this industry’s lead time and decision-making process. When you think about major oil companies, you think about aircraft carriers, not PT boats. Once they have their 2025 drilling plan set, which is halfway through 2024, they don’t change it based on the outcome of an election.

Let’s say the Keystone XL pipeline is approved tomorrow. It will still take years to build and will not be in service until after Donald Trump leaves the White House.

Daniel Yergin likes to remind people that the president of the United States does not determine supply or demand or set the oil price. Donald Trump can, and likely will, ease up on permitting, allowing the industry to initiate activity on federal onshore lands or offshore blocks that it could not effectuate under President Biden. Even if that happens, though, oil companies will still move deliberately. For example, if President Trump were to open drilling in the Arctic, companies would still have to assess the liability and reputational risks of exploring there.

Ultimately, leaders in this sector want sensible public policy that recognizes fossil fuels as global commodities, and that the domestic availability of hydrocarbons solidifies American companies’ leadership role in the world.

Q: What will change at the Federal Trade Commission mean for the energy industry?

A: The Trump administration initially announced that it was retaining some core components of the Biden administration antitrust framework, suggesting there could be more continuity at the Federal Trade Commission than some expected. However, more recently, President Trump announced the firing of two Democratic members of the Commission. I do think the general attitude toward energy sector mergers will change. During the Biden administration, it seemed like almost every energy combination was reviewed, even if it had zero or negligible anti-competitive characteristics. Still, the FTC would ask select questions or issue a full second request, causing delay or risking a blocked deal.

Now, under President Trump, industry participants with wish lists that include deals they did not think could get through the FTC or DOJ will try to make those deals happen over the next few years.

Q: We’ve entered a higher-risk world with tariffs, potential trade wars, and shifting alliances. What will the impact of that be on the energy industry?

A: It has highlighted the importance of U.S.-produced hydrocarbons for the U.S. market. No matter the trade regime, we are the most significant end market.

Everyone is lining up trying to buy U.S. inventory because the production is proximate to the best end market. You know, at least directionally, what the regulatory regime will be.

Outside the U.S., one must worry about tariffs and shifting winds across different regimes worldwide. The U.S. has long been the most important end market and may now be the most important producer, so it is attractive in both ways.

Q: What is the state of the global energy transition?

A: In places like Europe, governments and voters are realizing that oil and gas will still be necessary for a long time to come because the energy transition has proven harder, more costly, and slower than some anticipated.

People are also learning that moving too quickly away from existing reliable energy sources can have serious, unexpected ecological consequences. For instance, Germany decommissioned nuclear power plants and assumed they could add enough offshore wind and solar energy to compensate. They could not. Consequently, Germany burns lignite coal in power plants to get through the winter. That is 1930s technology with a high carbon output per unit of electricity produced.

Q: How do you think the established players in the global energy industry can help fast-developing countries meet their demand?

A: The developing world needs the expertise and support of the developed world to meet its energy requirements correctly. If we do not provide them with that expertise and support and they do it the wrong way, it does not make a difference what we do in the lower forty-eight states on carbon capture or anything else. That is a drop in the ocean if we return to coal as the world’s flex fuel.

Focusing on the U.S. alone is like declaring a no-peeing section in the swimming pool. It just doesn’t work. Greenhouse gas emissions are a global challenge that requires solutions deployed globally.

Q: How do the significant investments the U.S. has made in renewable energy figure into the global picture?

Remember that the United States only accounts for about 14% of global carbon emissions, and our share is declining. Solar and wind deployment is growing rapidly here and worldwide and will likely continue. However, fossil fuels still account for over 80% of global energy demand.

To understand why, remember that over a billion people live in energy poverty worldwide, and fossil fuels are often the most available, affordable, and reliable option for countries to meet their energy needs.

Take India. India is electrifying and trying to do so with LNG, the right bridge fuel. However, President Biden’s previous export ban on LNG caused the country to pivot back to coal. This is a global problem that needs to be addressed globally.

Q: What should leaders in the energy industry think about that may not be at the top of their minds right now?

A: The industry should consider where it will be in 30 years. And that is hard for public companies to do. They need to make their numbers every quarter and have annual planning and deployment of capital cycles.

The industry needs to explain that even if fossil fuels are reduced in the power and transportation sectors, oil and natural gas liquids are still used in just about every household good. The idea that we will completely wean ourselves off oil is unrealistic.

If you believe that carbon capture and sequestration will be part of our carbon emissions control, oil and gas companies’ downhole expertise will be necessary. Carbon goes into depleted reservoirs, and the people who know how to put it there are the same people who took it out. These are big, multi-year projects with high capital intensity and a rigorous engineering overlay.

If you are a large oil company or energy producer, you should offer the public and policymakers a clear vision for how you can write the next chapter of this industry and ensure that energy is cleaner and more abundant.

European Mid-Cap Outlook: Q&A with Dominic Lester, Edward Keen, and Lorna Shearin

Now in its fifth year, the Jefferies Pan-European Mid-Cap Conference has quickly established itself as a marquee event for investors and corporates focused on Europe’s mid-cap universe. Launched during the pandemic as a virtual gathering, the conference has evolved into one of the largest and most impactful events of its kind. This year, it returns to London with 190 participating companies (up from 167 in 2024) and 525 investors confirmed, representing 286 institutions worldwide.

The 2025 conference reflects Jefferies’ strategic commitment to supporting mid-cap companies across Europe. Investor attendance is up 47% year-on-year, with 36% of participants now coming from outside the UK, reflecting the rising global appetite for European mid-cap opportunities.

Ahead of this year’s conference, we sat down with Dominic Lester, EMEA Head of Investment Banking; Edward Keen, Head of Equities EMEA; and Lorna Shearin, Deputy Head of EMEA Investment Banking, to discuss the themes shaping the European mid-cap landscape and what to expect from the event.

European Mid-Cap Outlook

What are you most excited about as we head into this year’s conference?

Dominic Lester: From a macro perspective, Europe’s momentum is building. Ironically, recent US political shifts have pushed Europe towards greater economic coordination. The UK is moving closer to Europe, Germany has reawakened following Merz’s electoral victory, and we’re seeing renewed energy in Southern Europe, particularly Greece and Italy. Funding is available, debt financing remains resilient, and equity markets are competitive. All of this creates a fertile backdrop for mid-cap companies. It feels like the start of a European economic renaissance.

Lorna Shearin: The Jefferies Mid-Cap Conference is a unique event, and we always look forward to connecting with so many of our UK and European investment banking clients. This year, we have 65 UK corporates participating, and the conference provides an excellent opportunity to showcase them—particularly our UK broking clients—to a broad pool of global institutional investors. It promises to be an interesting three days as we hear how these companies are navigating shifts in technology and macroeconomic conditions, and how these factors are shaping their M&A and growth strategies.

2025 marks the conference’s fifth year—what makes this year’s conference stand out?

Dominic: It’s truly international, bringing together participants from across Europe and beyond. This reflects Jefferies’ long-term strategy to support the mid-cap universe. We’re seeing a diverse range of growth-oriented leaders—70% of companies are represented by C-suite management, with many new and returning names.

Edward Keen: I’m excited by the scale of participation—it’s becoming a bit of a marquee event! We now have 190 corporate attendees, with a third from the UK. The 125 European corporates represent a full range of sectors and include some of the most dynamic and exciting mid-cap companies in Continental Europe. On the investor side, we’re seeing large teams attending, some with up to 10 investment professionals. That shows deep institutional commitment and highlights Jefferies’ differentiation across trading, research, and banking.

How do you see the European mid-cap landscape evolving over the next 12–24 months?

Ed: We’ve expanded from a UK-centric model to pan-European coverage over the last few years. Mid-caps have always been a core focus for Jefferies, and there’s a strong case for European mid-caps right now. Valuations are compelling—most would argue they are cheaper than their US peers—and there’s real potential to find alpha. Our advisory expertise makes us a valuable partner to institutional investors.

Are there sectors or geographies where you expect significant deal activity or consolidation?

Dominic: Consolidation is accelerating in financial services, particularly in Italy, and we expect it to continue across Europe. Pharma remains active, and aerospace and defence are obvious areas given increased local defence spending. The IPO market is slowly reopening—we’ve seen corporate carveouts and private equity funds tap the public market to exit some assets that might be too large to sell, like Galderma. The constraint on European IPOs has been on the supply side, but I think we’ll see more high-quality companies coming to market, like Visma, Verisure, and other high-profile names such as Revolut. I don’t foresee a blockbuster IPO year, but it’s warming up and setting the stage for 2026. There’s also ongoing restructuring among over-leveraged companies, which will drive more M&A.

Lorna: Overall, deal activity remains healthy, particularly in technology, healthcare, energy and energy transition, and infrastructure, where we are seeing significant deal flow, including sponsor exits and public-to-private transactions. That said, the current geopolitical backdrop is making deal completion less certain and timelines to close are often longer. Geographically, Germany and the UK will likely remain focal points for many of our clients. It is the drive for innovation, sustainability, and digital transformation that continues to be the principal force behind M&A activity in the near and medium term.

Are institutional investors becoming more open to European mid-caps versus US opportunities?

Dominic: Yes. There’s a clear valuation arbitrage. Investors are still selective, but they’re looking for higher-growth opportunities—companies showing double-digit topline growth are in demand. In the UK, pension funds are under regulatory pressure to allocate more to public equities, which should help domestic demand as well.

Ed: Globally, we’re seeing US and AsiaPac long-only funds increasing their European exposure. We don’t really foresee people taking an overweight position—more of a rebalancing toward neutral. It’s important to remember that the liquidity profile of Europe is nowhere near as rich as the US. We have to tread carefully, but this could mark the beginning of a long-term shift. If there’s a resolution to the Russia-Ukraine crisis, there will be a resounding appetite for Europe, but things can change in an instant. Europe has its challenges—no one is totally immune to the effects of tariffs—but relative stability, predictability, and cheaper valuations are attracting capital.

Investor attendance is up 47%, with 36% ROW participation well above historical norms. What’s driving that international interest?

Ed: In my opinion, it reflects the diversification of global asset flows. Investors are moving away from being overweight in the US, and Europe is a key beneficiary. It also highlights the growing depth and breadth of Jefferies Corporate and Institutional investor clients. We are listening to what they want, and delivering!

Dominic: In addition, significant capital is flowing into Europe from the Middle East. Sovereign wealth funds and private equity investors there have both the capital and expertise, particularly in energy and industrial sectors. We’ve already seen large energy acquisitions in Germany and expect more to follow in industrials, petrochemicals, and beyond.

Any parting thoughts?

Dominic: This feels a bit like the 2020 reset. Historically, it’s been in the US’ interest to create military and economic dependence on the US. But as America turns inward, leaders in France, Germany, and the UK are taking the bull by the horns, and Europe is moving towards greater self-reliance in defence and energy security. I don’t think investors will sit on the sidelines in fear. People are shaken by geopolitical risks, but it’s prompting decisive action. This is a pivotal moment for Europe’s economy—and a huge opportunity for mid-cap investors.

Lorna: This is one of Jefferies’ flagship conferences, and it continues to grow year on year. In the same way that the Jefferies London Healthcare Conference has become a “must-attend” event in the annual calendar, we see our Mid-Cap Conference evolving in the same way. We’re delighted to host the event and to support both our corporate and institutional clients as they connect, grow, and flourish.

Ed: Make sure you sign up early if you want to come next year!

Data Moats, Infrastructure, and Agents: Where Investors See AI’s Next Big Opportunities

A Jefferies Insights Podcast

Evan Osheroff, Managing Director of Software Investment Banking at Jefferies, sat down with Don Stalter, North American Partner at Global Founders Capital, to discuss the trajectory of artificial intelligence (AI) and the opportunities growth investors are eyeing in the sector.

Their discussion covers the evolution of AI in business, the significance of data and operational expertise, the challenges and opportunities of investing in AI, the energy and infrastructure implications of AI’s growth, and emerging AI applications like autonomous logistics.

As a long-time investor and entrepreneur in technology, Don brings a unique perspective on what it takes for young companies to succeed in this fast-growing space — from building the right team to using open-source models to create application-layer businesses and AI agents. Mapping the AI market, where thousands of new companies launch each year, is no small task. Don and Evan’s conversation digs into the key questions investors should be asking and where the next big opportunities might lie.

Don Stalter is the North American Partner at Global Capital, where he has been an early backer of ten $1B+ unicorns. His most notable investment was in Deel, where he wrote the largest seed check and helped recruit key executives. Previously, Don co-founded CityDeal, a B2B marketing technology company acquired by Groupon in its early days. He also built out Groupon’s international offices and led global business development at Airbnb. Earlier in his career, Don worked in Credit Suisse’s tech M&A group and as a private equity investor at Savant Growth.

Evan Osheroff is a Managing Director of Software Investment Banking at Jefferies, with over 15 years of experience and more than $100B in completed transactions. He specializes in application and infrastructure software and has extensive expertise in M&A, IPOs, convertible offerings, debt financings, leveraged buyouts, and more.