This article is adapted from Weekly Economic & Bond Market Insights by Thomas Simons, CFA, Chief U.S. Economist at Jefferies, and Michael Bacolas. Simons brings two decades of experience analyzing Federal Reserve policy and is a frequent commentator on CNBC and other major financial media outlets.

A stronger-than-expected labor market is forcing investors to reconsider one of the dominant assumptions entering 2026: that the Federal Reserve would have room to cut interest rates by at least 50 basis points, beginning as soon as this fall.

While a path to lower rates remains possible, materially improved labor-market conditions are likely to keep the Fed in a “wait-and-see” posture through the remainder of the year, according to Jefferies’ economists.

Labor Demand Has Recovered

Nonfarm payroll growth averaged just 10,000 jobs per month in 2025. Through the first five months of 2026, payroll gains have averaged roughly 114,000 per month. The conflict in Iran has had a far milder impact on hiring than the trade war that weighed on economic activity last year.

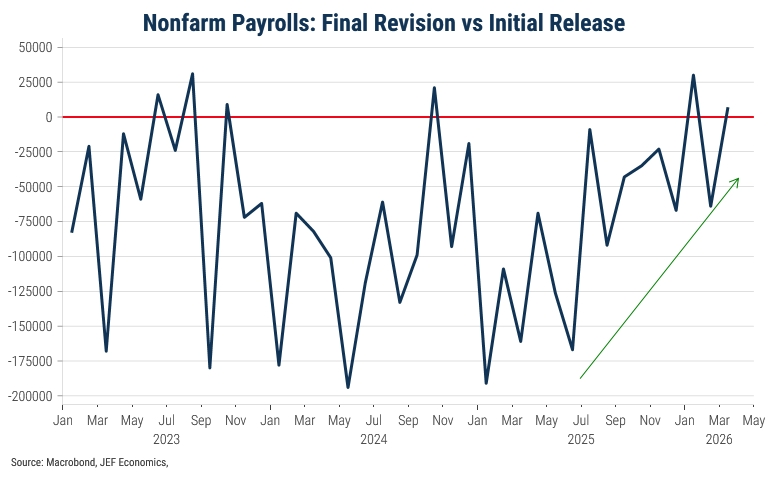

The improvement extends beyond headline payroll growth. Payroll revisions, which were consistently negative through 2025, have become progressively less negative and recently turned positive. The latest report included upward revisions totaling 93,000 jobs for March and April.

Job openings tell a similar story. For the first time since June 2025, the number of available positions now exceeds the number of unemployed workers. That ratio had fallen below one at the end of last year before steadily improving throughout 2026.

AI Hiring May Be Stronger Than Expected

The composition of recent job growth may be as important as the overall increase.

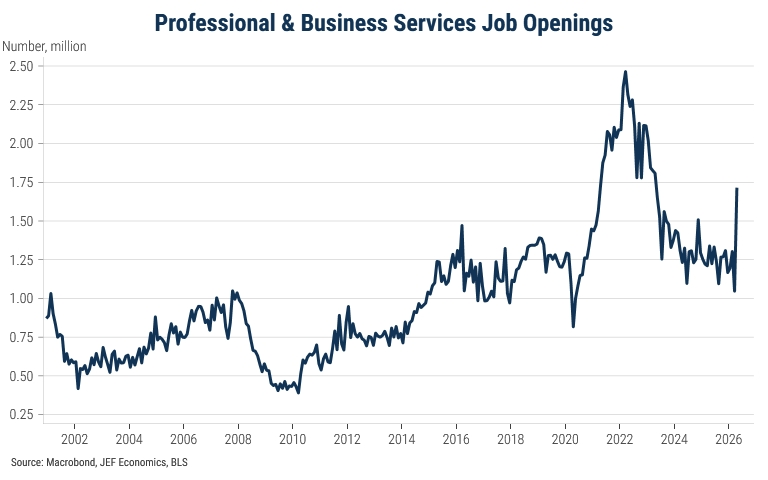

Much of the recent rise in job openings occurred in professional and business services, a category that includes computer systems design, technical consulting, and other specialized knowledge industries. These are among the sectors most frequently cited as being vulnerable to AI-driven job displacement.

A single report is not enough to establish a trend—but if the pattern persists, it may suggest that AI is creating new hiring demand rather than reducing it.

The strongest growth in openings occurred in the western United States and among businesses with fewer than ten employees. These trends may indicate that workers leaving large technology firms are forming new companies of their own. If so, the result could be faster AI development, greater competition across the technology sector, and eventually increased merger-and-acquisition activity.

Labor Tightness Could Increase

Several factors could reduce labor-market slack in the months ahead, including demographic trends, reduced immigration, and a decline in labor-force participation among workers between the ages of 20 and 24.

Some of that decline may reflect recent graduates returning to school after struggling to find employment. If labor demand remains strong and those workers are slow to reenter the workforce, labor-market conditions could tighten further and place upward pressure on wages.

Current monetary policy has not been restrictive enough to meaningfully suppress hiring. If wage growth accelerates alongside continued job creation, the case for rate cuts becomes increasingly difficult to make.

Why AI Could Complicate Fed Policy

Although Jefferies does not currently expect rate hikes, there is a growing debate within the Federal Reserve around productivity and the economy’s neutral rate of interest.

Conventional thinking holds that AI-driven productivity gains should eventually lower costs and help contain inflation. But the transition may not be so straightforward.

When productivity rises, businesses can generate more output from the same amount of labor and capital. That tends to increase the return on investment, encourage additional capital spending, and raise demand for financing. During that transition period, real interest rates can move higher rather than lower.

In other words, the same productivity gains that may eventually reduce inflation could initially support stronger growth, investment, and demand for capital. The question for policymakers is whether AI-driven productivity improvements arrive quickly enough to offset those forces.

The Range of Outcomes Remains Wide

While fewer economists are forecasting rate cuts in 2026, the Federal Reserve could once again have room to ease policy if AI-driven productivity gains help reduce costs and energy prices continue to decline.

At the same time, continued investment in AI infrastructure, resilient labor demand, rising real incomes, and accelerating productivity growth could justify keeping rates unchanged for an extended period—and may eventually revive discussions about additional policy tightening in 2027.

For now, Jefferies favors the view that AI will eventually prove disinflationary. But the pace of technological change has made economic forecasting unusually difficult.

A stronger labor market has already forced investors to rethink expectations for near-term rate cuts. What happens next may depend largely on whether AI’s impact shows up first in lower costs or stronger demand.