The European private markets landscape — and GP-led secondaries market in particular — is increasingly central to the global conversation around capital allocation. Its combination of institutional scale, growing liquidity, and depth of high-quality assets is shaping how capital is deployed worldwide like never before.

Consider that Europe is now home to approximately 8,000 of the estimated 32,000 privately owned buyout and growth-owned assets and about €950 billion of the €3.8 trillion in global private equity assets under management. In addition, the hold period for these assets has grown to more than seven years, resulting in a huge backlog of assets needing exits.

Beyond its growing size, this market also offers investors a distinctive asset profile that provides global investors with exposure they often will not find anywhere else. With Europe set to account for up to 30% of all GP-led secondary activity in 2026, now is the time for investors to explore a truly unique opportunity set.

A Step Change in Scale and Cadence

Europe helped shape the modern GP-led market. Some of the earliest continuation vehicles — and some of its most formative transactions — were executed there.

Early landmarks that set the template for today’s high-quality sponsor-led deals include Nordic Capital’s 2018 €2.5 billion continuation vehicle, PAI’s 2019 €2 billion CV that rolled over its stake in Froneri, one of the world’s largest ice cream makers, and CapVest’s €1.8 billion single-asset CV for Curium in 2020.

What feels different today is not the quality of European deals — that has always been high — but their scale and cadence. The region is now producing a steady stream of large, industry-defining deals.

In 2025, Jefferies advised on a £2.3 billion CV for Inflexion — the largest multi-asset CV raised in Europe to date — and on TDR Capital’s single-asset CV for David Lloyd, which reportedly valued the company at ~£2 billion.

We estimate that approximately 50 GP-led transactions closed across the region in 2025, representing about $33 billion in volume. Looking ahead, Jefferies expects the global secondaries market to eventually reach $400 billion, with GP-led accounting for approximately $200 billion. We also estimate that 33% of global CVs will come from Europe in the future. The size of this market could reach €60 billion by 2030, with over 110 deals involving the highest quality assets.

A Distinctive Asset Profile

Europe’s growth reflects a distinctive asset profile well-suited to the CV structure. The market is more middle-market-oriented than the US market, and many of the businesses best suited to CVs have already established themselves as domestic leaders, looking to scale across Europe or internationally. These assets are large enough to be proven but still early enough in their growth journey to offer a broad range of exit routes, with a wider pool of strategic and PE buyers than their more mature US counterparts.

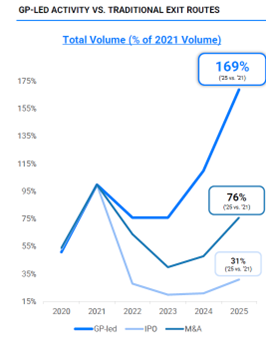

The pressure on GPs to pursue alternative liquidity routes is acute. There is more than $3 trillion in unrealized value across global buyout portfolios and traditional M&A and IPO markets, well below 2021 peaks. European GPs, which sit atop a quarter of the world’s PE assets, are not immune to this pressure, and continuation vehicles offer a compelling answer.

Not Simply a Smaller US Market

In January 2025, Paris-based Ardian closed on an approximately €29 billion fundraise for its ASF IX secondary fund – making it the largest such fund in the world. In fact, this was the largest private equity fund of any kind to close in 2025.

It was yet another sign that Europe is now a defining force in the global GP-led secondary market.

Europe certainly is not just a scaled-down version of the US market. Its markets have developed under a more challenging geopolitical backdrop — including risks from the war in Ukraine, energy price volatility stemming from the Iran conflict, and trade friction that lands squarely in regional deal underwriting — and transactions can still face a tougher path through US-centric investment committees. European companies may face more challenges, but those that overcome them tend to emerge as more resilient businesses led by people with top-tier operational and strategic leadership skills. This is just one reason that the longstanding assumption that Europe should automatically carry a risk discount is looking less convincing than it once did.

Alignment That Looks Different

There is also a meaningful structural difference in how GP alignment works in Europe. In the US, most PE funds use a deal-by-deal waterfall: the GP earns carry on each successful investment once that deal has returned capital and cleared its preferred return. In Europe, the dominant structure is a fund-level waterfall: the GP earns carry only after the fund as a whole has returned all LP capital and met its preferred return on a fund-wide basis.

Many European GP‑led transactions do not crystallise carried interest in the selling fund at the point of execution. As a result, Jefferies estimates headline. GP commitment in the US averaged at ~9.8% of total commitments vs. Europe at ~4.6%.

In practice, strong alignment with CV investors is preserved through different mechanisms. European sponsors more frequently commit capital on an out‑of‑pocket basis — often supported by financing — and participation from the flagship fund is also more prevalent. This can place a sponsor’s core track record at risk, creating a strong signal of alignment.

The distinction is therefore one of structure rather than substance: alignment in European transactions is expressed differently but is typically comparable with US transactions.

Global Capital Is Taking Notice

The fundraising backdrop reinforces the growing appeal of the secondaries market in Europe: A 2026 survey of PE managers found that 43% of EMEA respondents plan to increase their use of GP-led secondaries over the next 24 months, up from 14% last year — a clear signal that adoption still has room to grow.

The case for Europe’s centrality to the GP-led market is no longer a forward-looking argument — it is now a reality. With a quarter of the world’s PE assets, a middle-market profile ideally suited to the continuation vehicle structure, and a growing roster of landmark transactions executed under challenging conditions, the region has demonstrated it can compete at the highest level. Europe is not catching up to the next phase of the GP-led market. It is leading it and is increasingly central to the decision-making of global capital allocators.